Realty Executives Midwest

If you’re thinking about selling your house this year, you may be torn between two options:

In 2026, that decision matters more than it used to. Here’s what you need to know.

Over the past year, the number of homes for sale has been climbing. And this year, a Realtor.com forecast says it could go up another 8.9%. That matters. As buyers gain more options, they also re-gain the ability to be selective. So, the details are starting to count again.

That’s one reason most sellers choose to make some updates before listing.

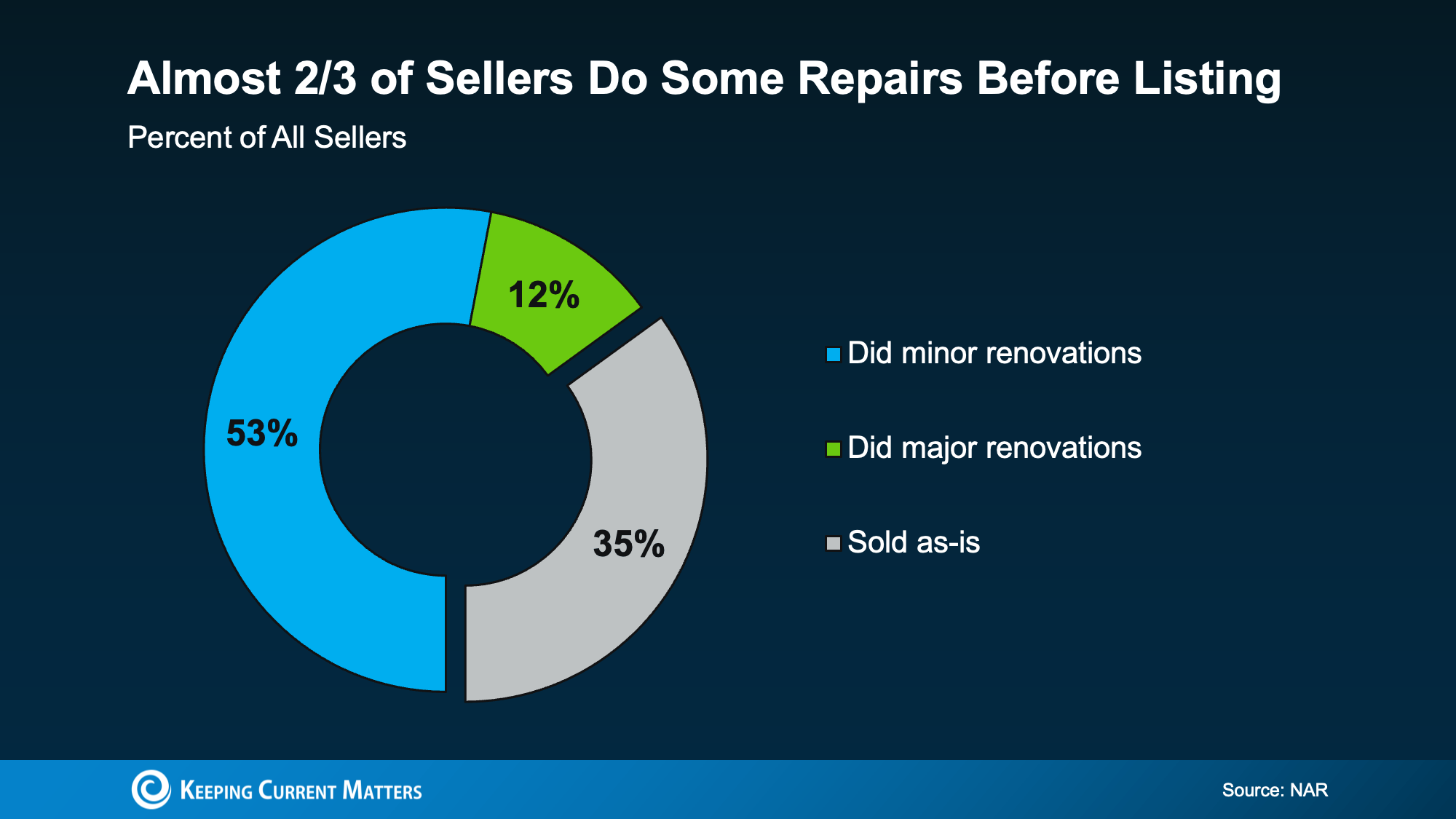

According to a recent study from the National Association of Realtors (NAR), two-thirds of sellers (65%) completed minor repairs or improvements before selling (the blue and the green in the chart below). And only one-third (35%) sold as-is:

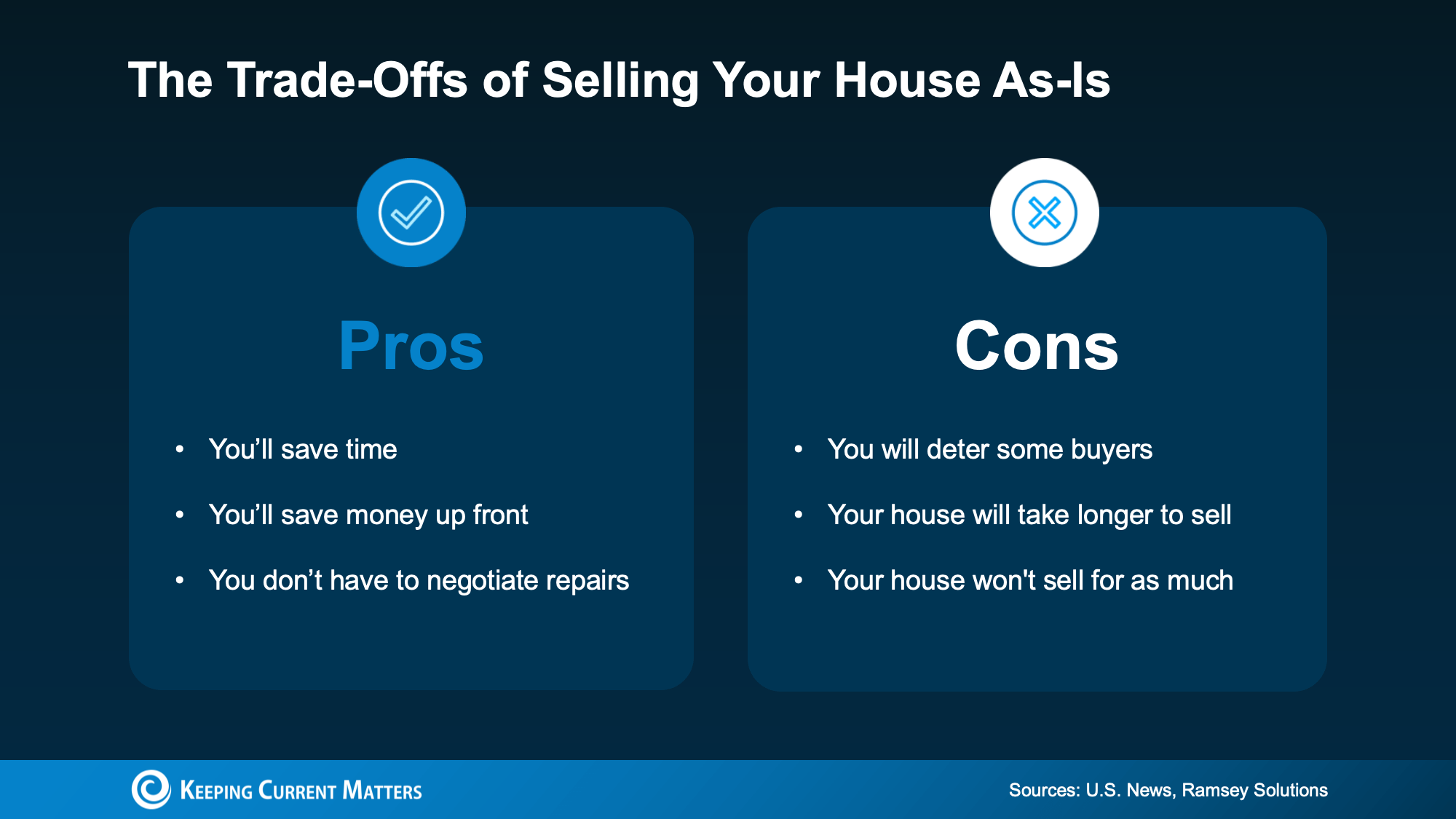

Selling as-is means you’re signaling upfront that you won’t handle repairs before listing or negotiate fixes after inspection. That can definitely simplify things on your end, but it also narrows your buyer pool.

Homes that are move-in ready typically attract more buyers and stronger offers. On the flip side, when a home needs work, fewer buyers are willing to take it on. That can mean fewer showings, fewer offers, more time on the market, and often a lower final price.

It doesn’t mean your house won’t sell – it just means it may not sell for as much as it could have.

How an Agent Can Help

How an Agent Can HelpSo, what should you do? The answer isn’t one-size-fits-all. It’s going to depend a lot on your house and your local market.

And that’s why working with an agent is a must. The right agent will help you weigh your options and anticipate what your house may sell for either way – and that can be a key factor in your final decision.

The good news is, there’s still time to get repairs done. Typically speaking, the spring is the peak homebuying season, so there are still several months left before buyer demand will be at its seasonal high. That means you have time to make some repairs, without rushing or stressing, and still hit the listing sweet spot.

The choice is yours. No matter what you end up picking, your agent will market your house to draw in as many buyers as possible. And in today’s market, that expertise is going to be worth it.

While selling as-is can still make sense in certain situations, in some markets today, it may cost you. So, no, you don’t have to make repairs before you list. But you may want to.

To make sure you’re considering all your options and making the best choice possible, connect with an agent to have a quick conversation about your house.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

After several years of high mortgage rates and hesitation from buyers, momentum is quietly building beneath the surface of the housing market. Sellers are reappearing. Buyers are re-engaging. And for the first time in what feels like forever, there’s movement happening again.

No, it’s not a surge. But it is a shift – and it’s one that could set the stage for a stronger year in 2026.

So, what’s driving the comeback? Here are three big trends that are slowly breathing life back into the housing market right now.

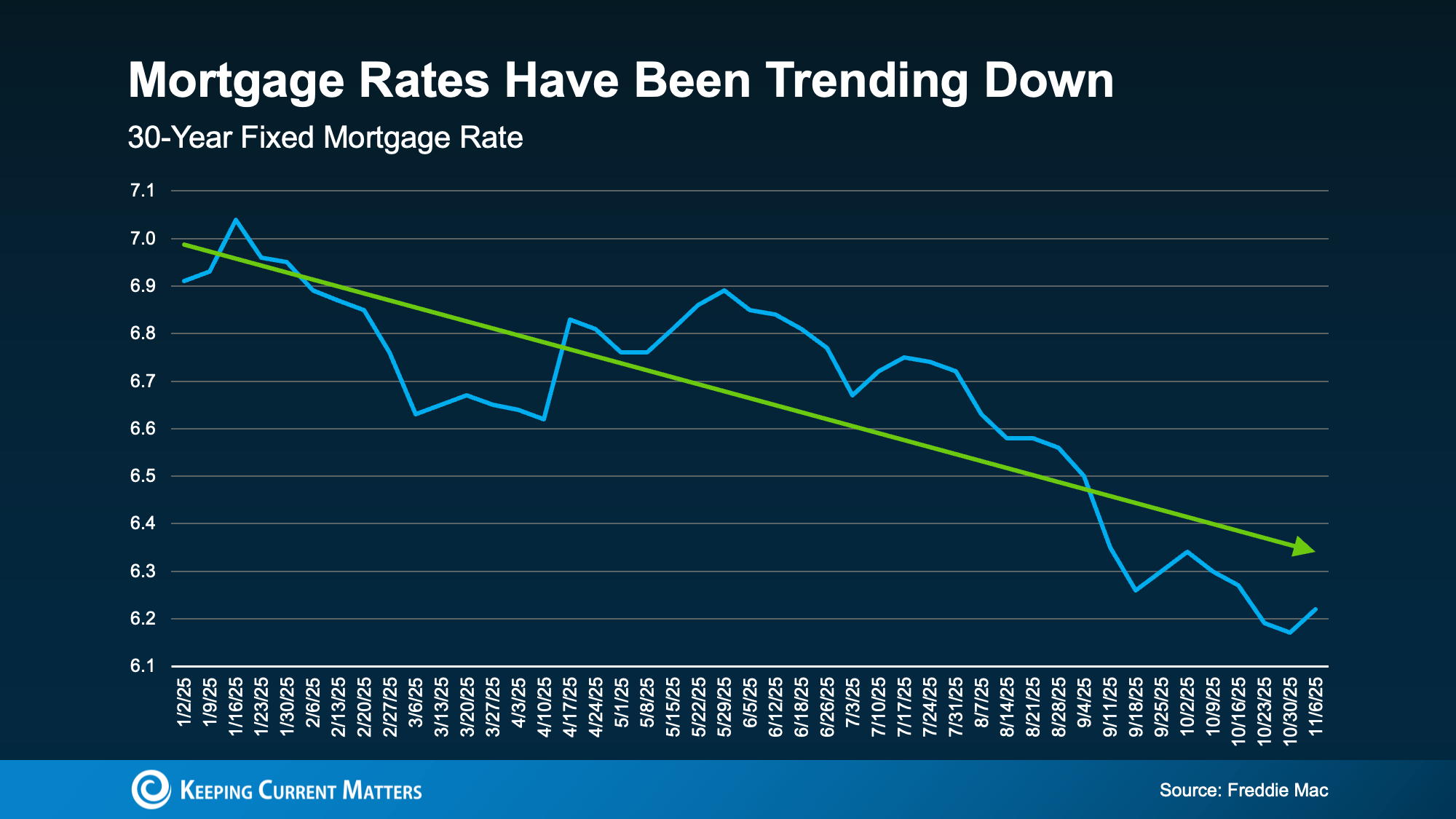

Mortgage rates are always going to have their ups and downs – that’s just how rates work. Especially with the general economic uncertainty right now, some volatility is to be expected. But, if you zoom out, it’s the larger trend that really matters most.

And overall, rates have been trending down for most of this year (see graph below):

And in just the last few months, we’ve seen the best rates of 2025. According to Sam Khater, Chief Economist at Freddie Mac:

And in just the last few months, we’ve seen the best rates of 2025. According to Sam Khater, Chief Economist at Freddie Mac:

“On a median-priced home, this could allow a homebuyer to save thousands annually compared to earlier this year, showing that affordability is slowly improving.”

Here’s why that matters for you. This shift changes what you can actually afford. It means lower borrowing costs and more buying power. Take this as an example.

Data from Redfin shows a buyer with a $3,000 monthly budget can now afford roughly $25,000 more home than they could one year ago. That’s a big deal. And it’s just one of the reasons why activity is picking up.

For a while, many homeowners stayed put because they didn’t want to give up their low mortgage rate. That “lock-in effect” kept inventory tight. And while plenty of homeowners are still staying where they are today, the number of rate-locked homeowners is starting to ease as rates come down. Life changes are becoming a bigger part of what’s driving more people to move, and that’s opening up more inventory.

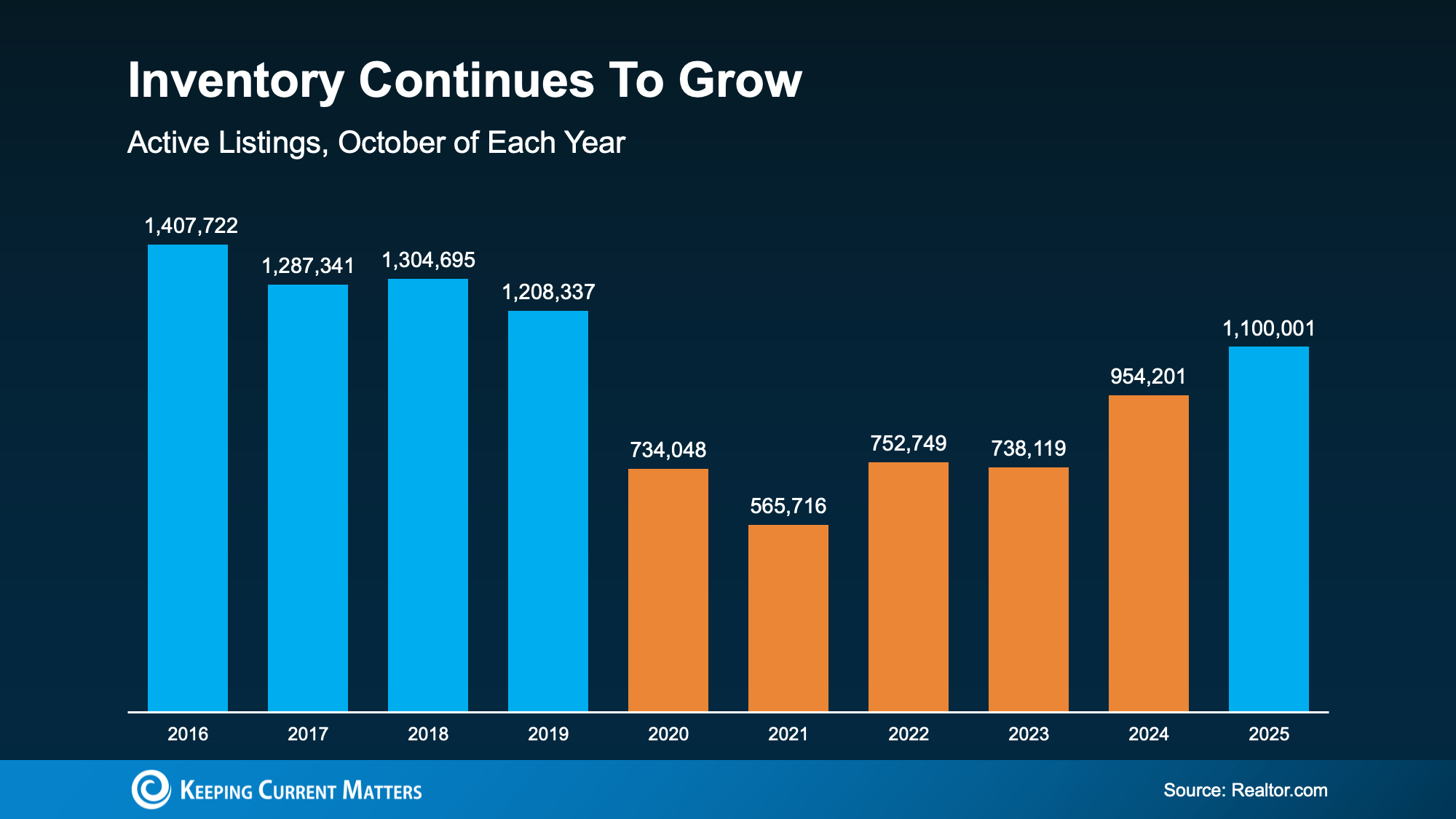

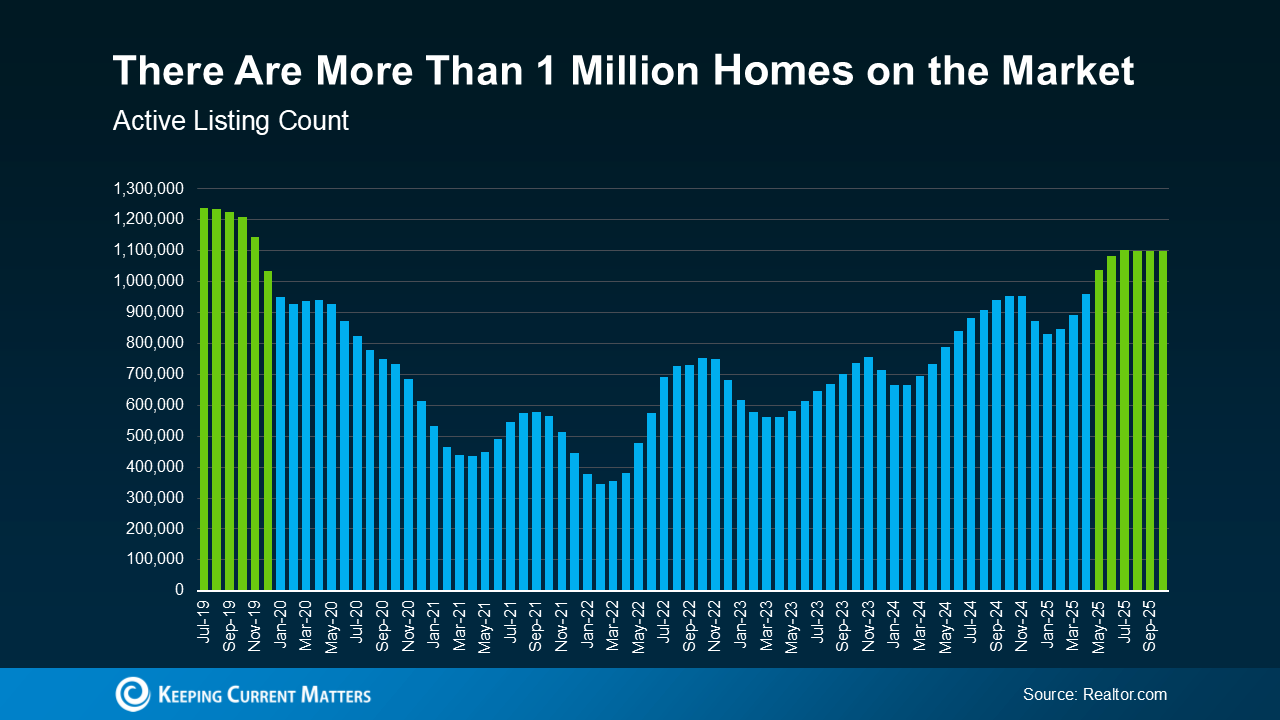

Data from Realtor.com shows just how much the number of homes for sale has grown. And the really interesting part is that the market is approaching levels that haven’t been seen for the past six years (see the blue on the graph below):

That return to more normal inventory levels is a really good thing. It gives buyers more options than they’ve had in years. And it’s helping to bring the market closer to balance.

That return to more normal inventory levels is a really good thing. It gives buyers more options than they’ve had in years. And it’s helping to bring the market closer to balance.

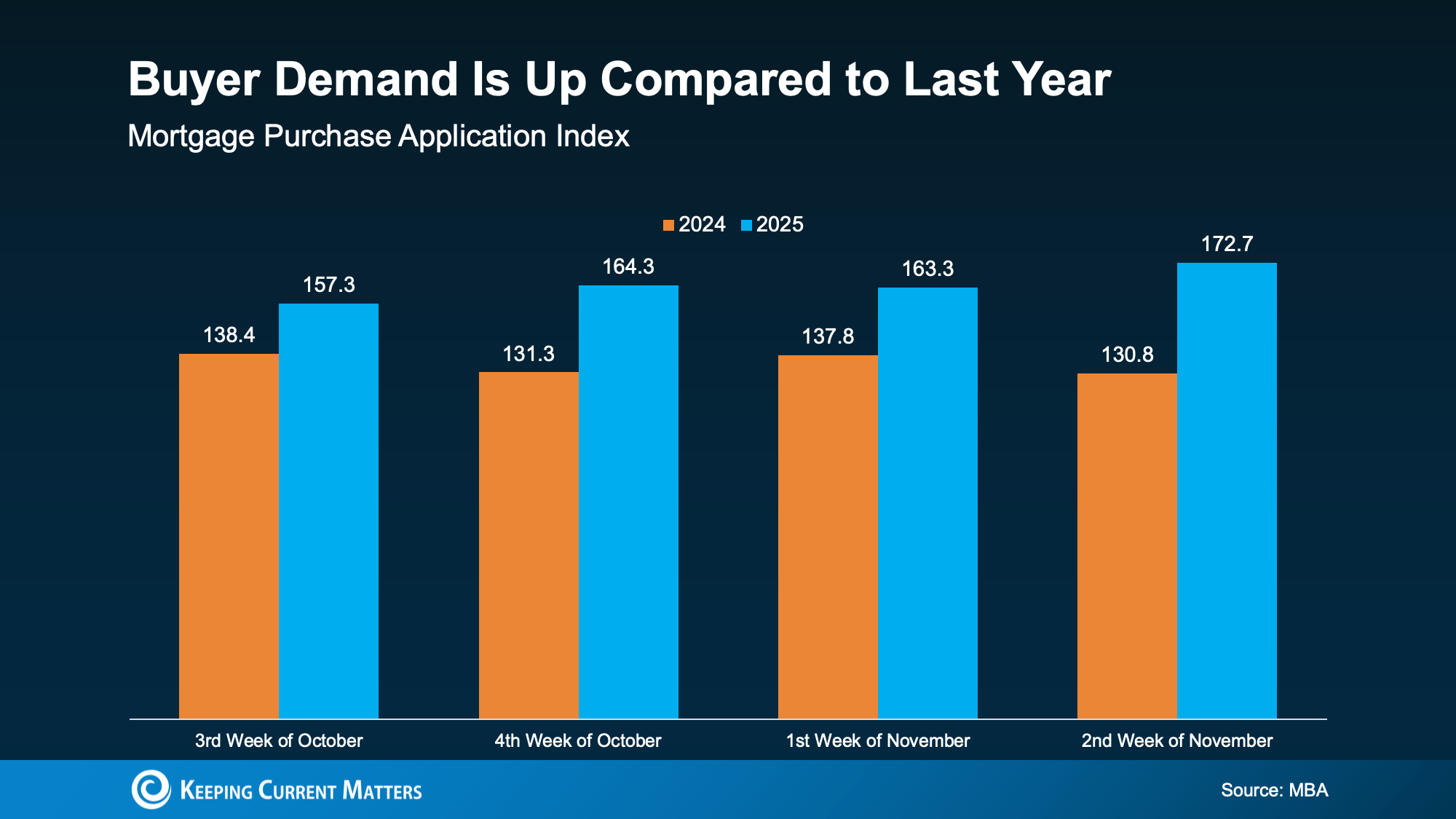

And it’s not just sellers making moves. With more options and slightly better affordability, buyers are getting back in the game, too. The Mortgage Bankers Association (MBA) reports purchase applications are up compared to last year, a clear signal that demand is building again (see graph below):

And experts think this momentum will continue. Economists from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) all forecast moderate sales growth going into 2026.

And experts think this momentum will continue. Economists from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) all forecast moderate sales growth going into 2026.

Now, this recovery won’t happen overnight. It’s not a flood of activity. But it is the start of steady improvement going into 2026. And that’s something a lot of people have been waiting for.

After several slower-than-normal years, the market is finally starting to turn a corner. Declining mortgage rates, more listings, and growing buyer activity all point to a market gaining real traction.

Connect with a local real estate agent about what’s changing and how you can make the most of it in 2026.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

If you’re trying to decide if you’re ready to become a homeowner in the next twelve months, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates, home prices, the current state of the economy, and more. And, you’re juggling how all of those things will impact the choice you’ll make. It’s a lot.

But here’s what you need to remember. While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

So, instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether or not you’re ready to make your move.

Buying a home is a big commitment. You’re going to take out a home loan stating you’ll pay that loan back. Knowing you have a reliable job and a steady stream of income is important and will give you peace of mind for a purchase so large.

If you have a reliable paycheck coming in, the next thing to figure out is what you can afford. This depends on your budget, spending habits, debts, and more.

At this point, it helps to talk with a trusted lender. They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs, and other expenses you’ll want to budget for. That way, you have a good idea of what to expect.

As you crunch your numbers, you’ll want to make sure you have enough cash left over in case of emergency. Think about it. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. It’s not a fun topic, but it’s an important one. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

It was mentioned above, but buying a home comes with some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes some time. If you plan to move again soon, you may not recoup your full investment.

So, how long should you stay put in an ideal world? Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you’re going to live there for a while, it may make sense to go for it. But, if you’re looking to sell and move within a year or two because you’re planning to transfer to a new city with that promotion you’ve been working so hard for, or you anticipate you’ll need to move to take care of family, those are things to factor in.

If you do, great. But if you don’t, finding a trusted local agent and a lender is a good first step. Having the right team can make figuring out everything else easier. The pros can talk you through your options and help you decide if you’re ready to make your move, or if you have a few more things to get in order first.

If you want to have a conversation about all the things you need to consider to determine if you’re ready to buy, connect with a local real estate professional.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Whether it’s at a family gathering, your company party, or catching up with friends over the holidays, the housing market always finds its way into the conversation.

Here are the top three questions on a lot of people’s minds this season, and straightforward answers to help you feel more confident about the market.

Yes, more than you could a year or two ago.

The number of homes for sale has been rising over the past few years. According to data from Realtor.com, there have been more than one million homes on the market for six straight months, something that hasn’t happened since 2019 (see graph below):

That means two things:

That means two things:

Many homeowners who held off are realizing the shelves aren’t bare anymore. So, if you hit pause on your home search last year because nothing fit your needs, it may be worth another look. With more homes on the market now, you’re not competing for the same handful of listings like you were a couple of years ago.

And because there’s a bit more to choose from, homes aren’t disappearing the minute they hit the market. That gives buyers more space to breathe, more options to compare, and a little more time to make a confident decision.

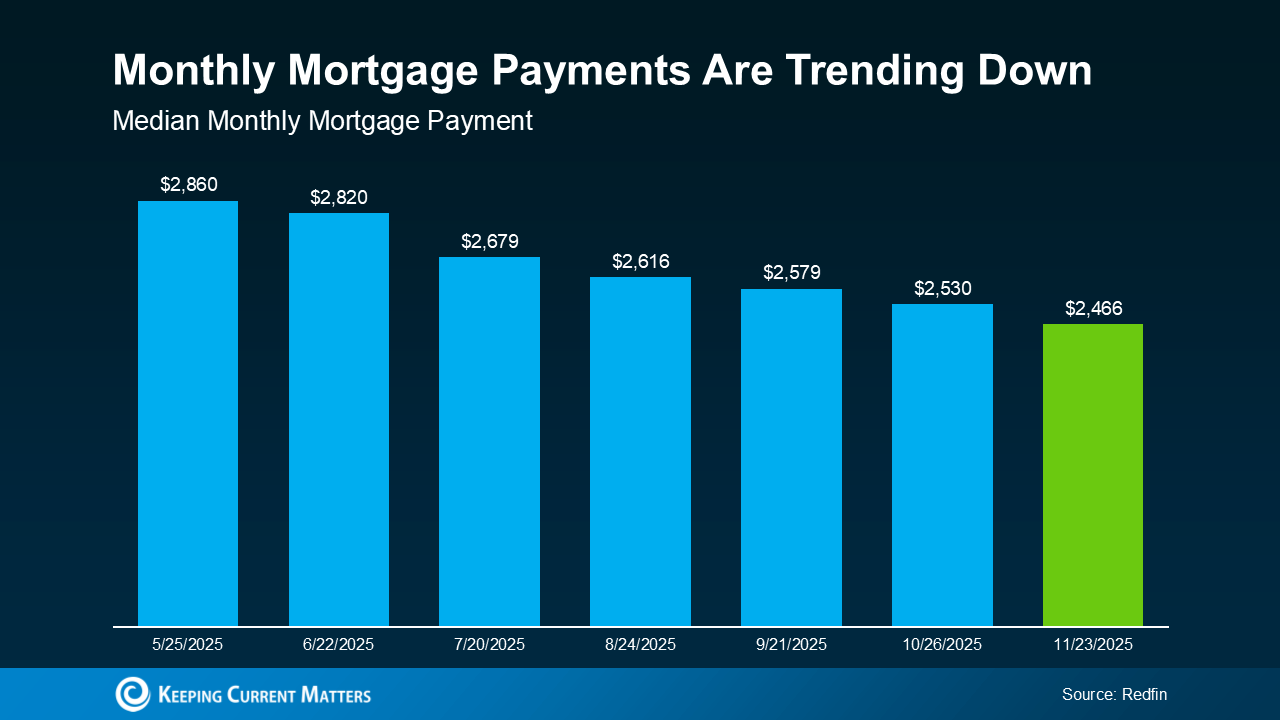

Affordability is starting to improve. Finally.

It’s been a tough few years for buyers. But this year brought some much-needed good news:

That adds up to a monthly mortgage payment that’s hundreds of dollars lower than it would have been just a few months ago (see graph below):

Buying still isn’t easy, but the numbers are starting to improve. For a lot of people, that means buying a home is becoming a more realistic goal again.

Buying still isn’t easy, but the numbers are starting to improve. For a lot of people, that means buying a home is becoming a more realistic goal again.

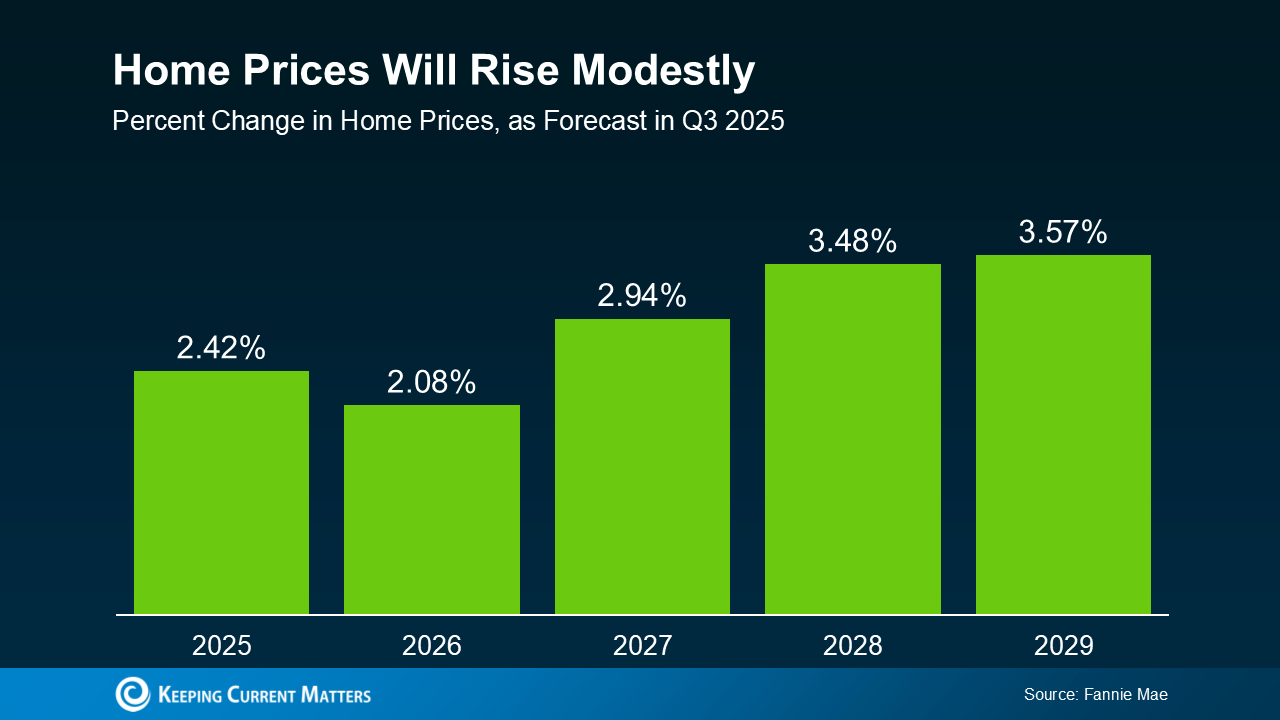

A lot of people worry that the housing market is about to crash, but the data doesn’t point in that direction. Yes, the number of homes for sale has been rising, but it’s still nowhere near the level needed for prices to fall significantly on a national scale. On top of that, homeowners today have a lot of equity and are in a much stronger financial position than they were back in 2008.

Of course, every local market is a little different. Some areas are still seeing prices climb, while others that saw huge spikes a few years ago are leveling off or seeing small corrections. But overall, the national picture is clear: experts surveyed by Fannie Mae project home prices will keep rising, just at a slower, more normal pace (see graph below):

That’s why waiting for a major price drop to get a deal isn’t a very strategic plan. History shows the same thing over and over: people who spend time in the market tend to build the most long-term wealth, not the people who try to time the market perfectly.

That’s why waiting for a major price drop to get a deal isn’t a very strategic plan. History shows the same thing over and over: people who spend time in the market tend to build the most long-term wealth, not the people who try to time the market perfectly.

Talk about the housing market can feel loud and confusing, especially when you’re hearing so many different takes. A trusted local agent can help you make sense of the data and understand your options. If you’re thinking about buying or selling, reach out to a local professional.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Want to know how to find the best deal possible in today’s housing market? Here’s the secret. Focus on homes that have been sitting on the market for a while.

Because when a listing lingers, sellers tend to get more realistic – and, more willing to negotiate. And that’s where the savviest buyers are finding homes other buyers overlook.

According to Realtor.com, about 1 in every 5 listings (20.2%) have dropped their asking price at least once. And while so many things in today’s housing market vary by region, that number is consistent throughout the country. That tells you one thing…

No matter where you live, there’s a chance to score a better deal. You just need to know where to look. And that’s where your agent comes in.

Your agent can help you identify which homes have been on the market the longest. Those are the ones where you’re more likely to get a discount. That’s because the seller may be getting frustrated their house hasn’t sold yet, so they’re more willing to play ball.

And since a lot of buyers steer clear of homes that aren’t selling, you may be the only offer they get. So, you can lean in and push for a better deal. As Realtor.com explains:

“Less competition means fewer bidding wars and more power to negotiate the extras that add up: closing cost credits, home warranties, even repair concessions . . . these concessions can end up knocking thousands of dollars off the price of a home.”

And they’re not the only ones calling out the opportunity you have right now. Bankrate also says:

“During the quieter fall and winter months, when fewer prospective buyers are shopping, home sellers may be more willing to lower their prices, or offer concessions, to attract those prospective buyers who are still looking.”

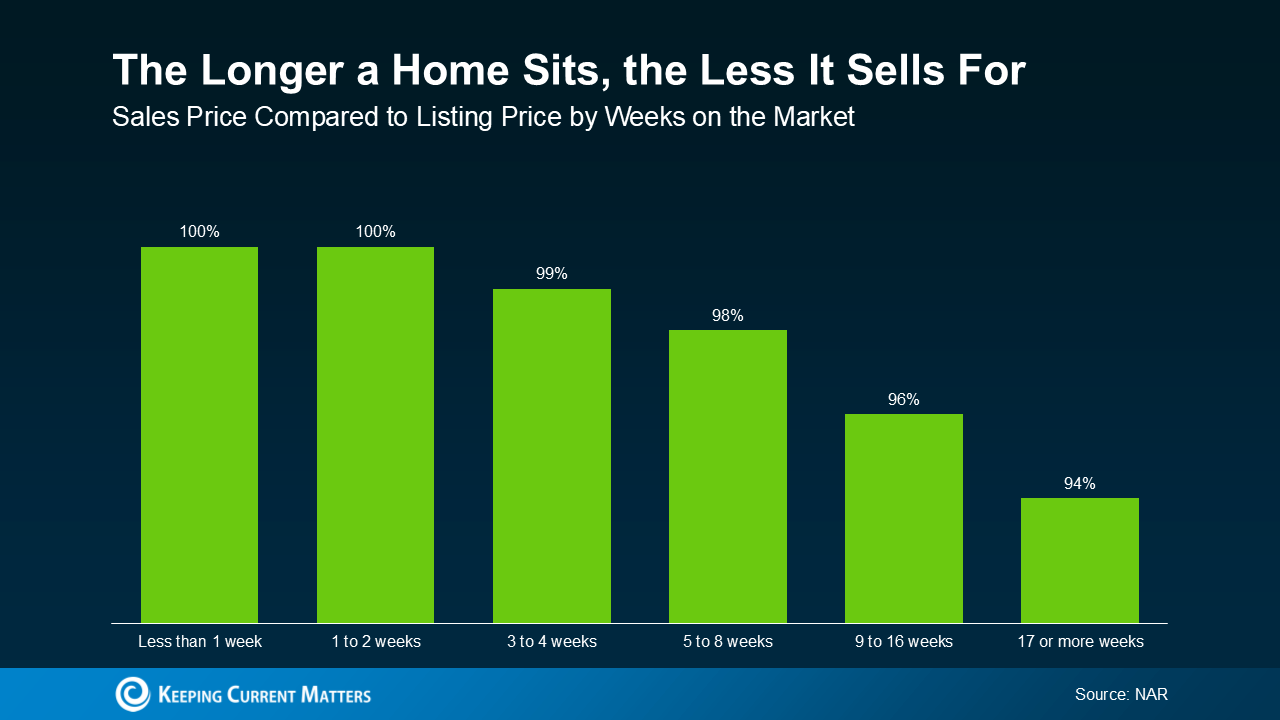

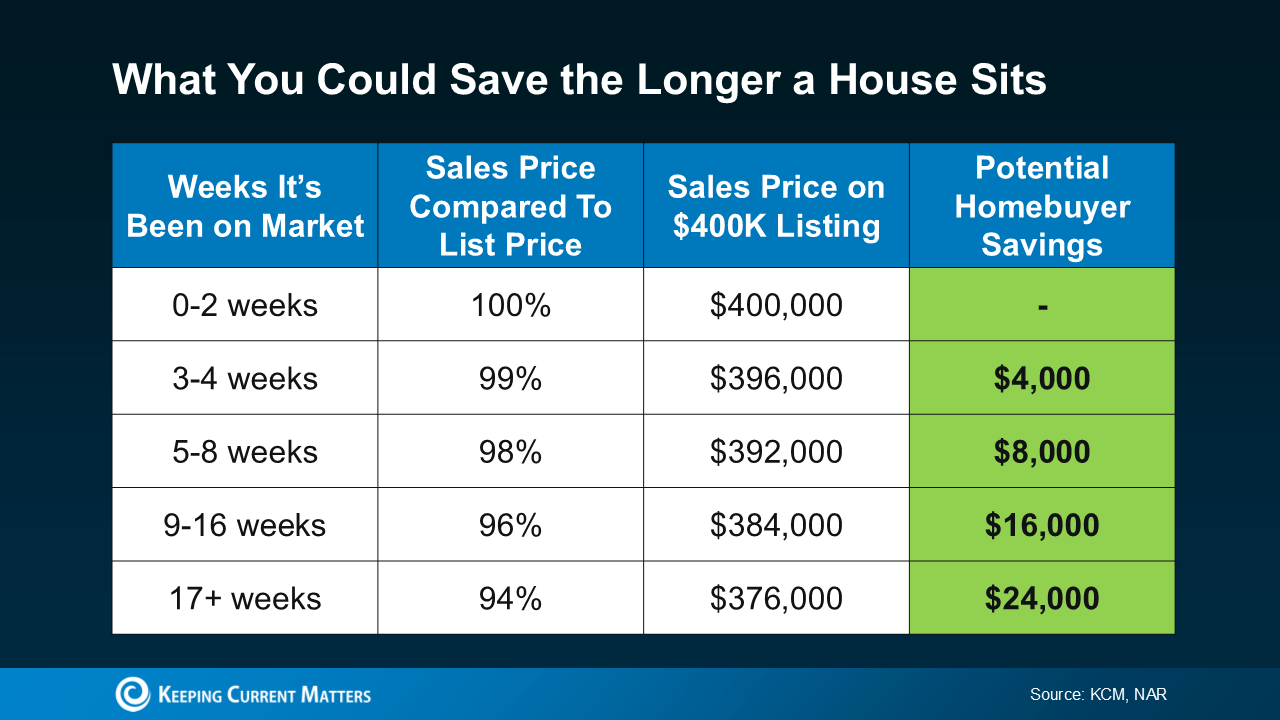

And the proof is in the data. The National Association of Realtors (NAR) shows a clear pattern: the longer a home stays on the market, the lower it tends to sell for compared to the original asking price.

So, if you’re serious about getting as much as you can for your money, focusing on these listings could be your best strategy yet.

So, if you’re serious about getting as much as you can for your money, focusing on these listings could be your best strategy yet.

And while paying 94% of the original asking price may not sound like much of a deal, the savings add up. That’s roughly $24,000 in savings on the median priced home (see chart below):

Zillow sums it up best:

Zillow sums it up best:

“If you’re a buyer who is hoping to strike a deal, look for homes that have been on the market for a while and that may already have lowered prices to entice buyers. You may find a motivated seller who is more willing to negotiate.”

If you want to find the best deal possible on a home right now, start by looking where others aren’t.

With 1 in 5 sellers cutting prices and many growing more flexible by the week, the homes that have been sitting a little longer could be your best opportunity to save.

Talk to a local agent about where to find them in your area.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.