Realty Executives Midwest

Here’s something you should know before you sell your house. The homeowners who win in today’s market aren’t the ones waiting it out or stepping back. They’re the ones who adapt from the start.

A number of homeowners this year didn’t get the outcome they wanted. But it’s not because something’s wrong with the market. It’s because something wasn’t right with their expectations.

Realtor.com reports 57% more homes have been taken off the market compared to last year. That means they listed… but didn’t sell. But here’s the honest truth. It was mostly because of two things: price and timing.

And if the seller had come in with the right mindset on each, their sale would’ve gone differently. Here are the top 2 things you can learn from those other sellers.

Let’s start with the most common sticking point: the asking price. Today, 8 in 10 sellers expect to get their asking price or more. But that confidence doesn’t always line up with reality.

According to Redfin, only 1 in 4 (25.3%) sellers are actually getting more than their list price.

And here’s where the mismatch is coming from.

And here’s where the mismatch is coming from.

A few years ago, you could set any price and buyers would come running, no matter what the price tag said. Odds are, you’d still sell for over asking. But things are different now.

Buyers have more options than they’ve had in years, so they can afford to be more selective. If your price feels even a little high to them, it’ll get overlooked in a heartbeat.

And for the homeowners who had that happen, some end up pulling their listings instead of making a simple adjustment that could have changed everything. Which is a shame, honestly. Because a small price tweak is usually all it takes to bring buyers in and get the deal done.

According to HousingWire, the average price cut right now is just 4%.

Think about that. Other sellers are listing too high and giving up rather than dropping their price 4%. If they’d just started 4% lower, they may have already sold. So, before you list, talk to your agent about what’s working nearby. They’ll help you find the sweet spot that’s competitive, realistic, and still protecting your bottom line.

And here’s the kicker. If you’ve been in your home for a while, your equity gives you room to set your list price more competitively and still come out way ahead. Unfortunately, those other sellers didn’t seem to realize that.

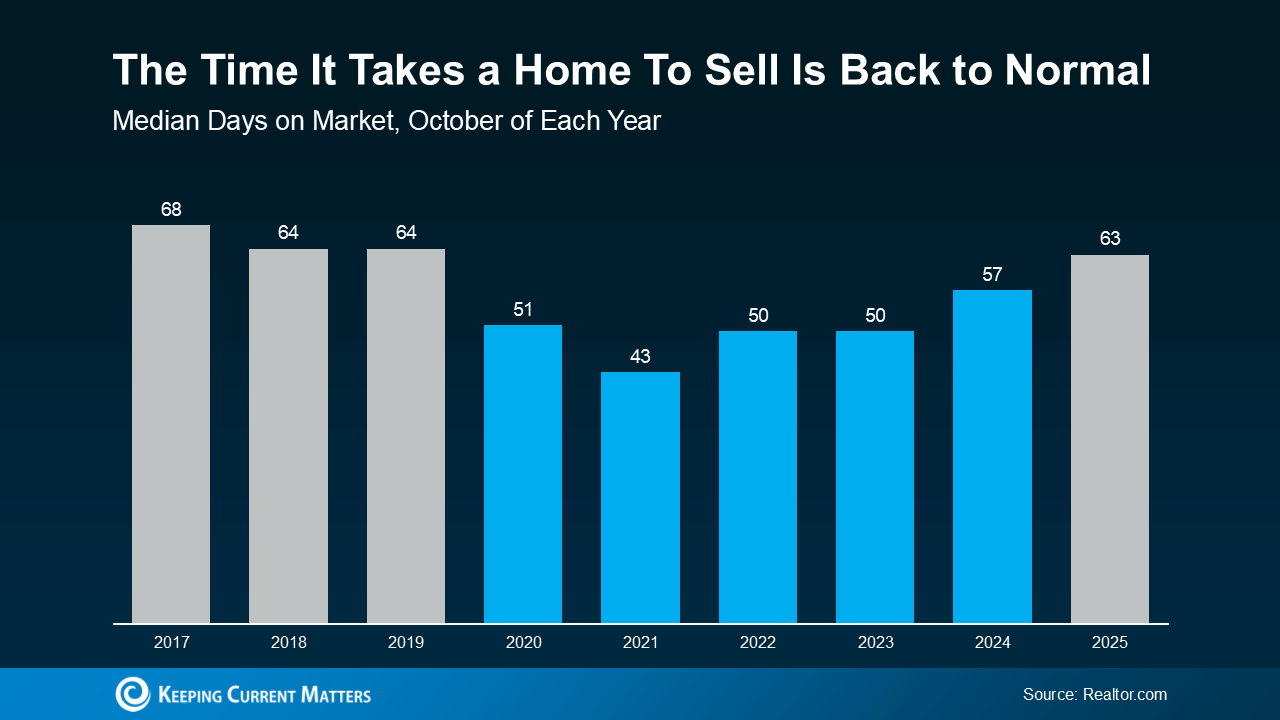

Another common misstep: expecting your house to sell in a weekend.

Many sellers right now remember when homes sold in as little as hours – and they expect that to happen today. But in most markets, that’s not the reality anymore.

It takes closer to 60 days to go from listed to sold, which is actually normal (see the gray in the graph below):

It just feels slower because they’re comparing it to the lightning-fast pace of 2020 and 2021.

It just feels slower because they’re comparing it to the lightning-fast pace of 2020 and 2021.

Think of it like driving 65 mph on the highway, then exiting and going 25. It feels like you’re crawling, but it’s actually the right speed for where you are. That’s what other sellers can’t seem to get over. But you can get ahead of that, by knowing what to expect.

Today’s buyers are more intentional. They’re taking their time, weighing their options, and making thoughtful decisions, which is creating a much healthier housing market.

So, if you’re planning to sell, don’t expect it to happen instantly. And don’t assume your house won’t sell if it doesn’t go under contract in the first weekend.

It’s normal for these things to take time.

If you want to make sure your house sells as quickly as possible, talk to your agent about ways to stand out, whether that’s through staging, photography, or strategic pricing. With the right advice, the right price, and the right prep work, it can still sell quickly.

If you’re thinking about selling, don’t let the market discourage you, let it guide you. The listings that didn’t sell this year weren’t doomed. They just started with the wrong strategy.

You can still win if you price right, are patient, and work with a local agent who knows how to position your home from the start.

Because in today’s market, success isn’t about waiting for conditions to change. It’s about getting your expectations right from day one.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

If there was one simple step that could help make your home sale a seamless process, wouldn’t you want to know about it?

There’s a lot that happens from the time your house goes under contract to closing day. And a few things still have to go right for the deal to go through. But here’s what a lot of sellers may not know.

There’s one part of the process where some homeowners are hitting a road bump that’s causing buyers to back out these days. But don’t worry. The majority of these snags are completely avoidable, especially when you understand what’s causing them and how to be proactive.

That’s where a great agent (and a little prep) can make all the difference.

The latest data from Redfin says 15% of pending home sales are falling through. And that’s not wildly higher than the 12% norm from 2017-2019. But it is an increase.

That means roughly 1 in 7 deals today don’t make it to the closing table. But, at the same time, 6 out of 7 do. So, the majority of sellers never face this problem – and odds are, you won’t either. But you can help make it even less likely if you know how to get ahead.

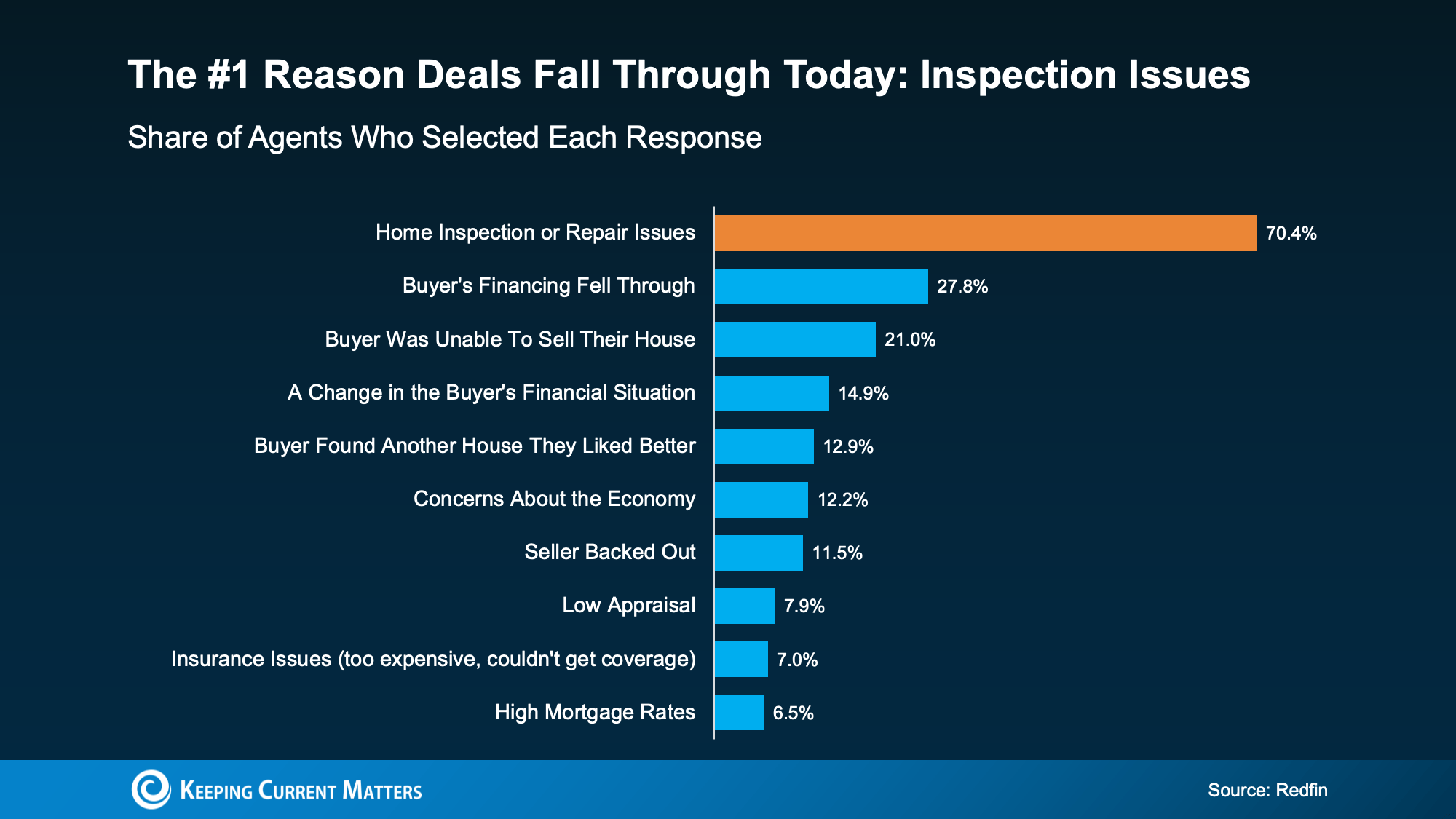

You might assume the main reason buyers are backing out today is financing. But that’s actually not the case. The most common deal breaker today, by far, is inspection and repair issues (see graph below):

Here’s why that’s a sticking point for buyers right now:

Here’s why that’s a sticking point for buyers right now:

The sellers with the best agents have heard about this shift and they’re doing what they can to go in prepared. Enter the pre-listing inspection.

It’s exactly what it sounds like. It’s a professional home inspection you schedule before your home hits the market. And while it’s not required, the National Association of Realtors (NAR) explains why it could be a valuable step for some sellers right now:

“To keep deals from unraveling . . . it allows a seller the opportunity to address any repairs before the For Sale sign even goes up. It also can help avoid surprises like a costly plumbing problem, a failing roof or an outdated electrical panel that could cause financially stretched buyers to bolt before closing.”

Think of it as a way to avoid future headaches. You’ll know what issues could pop up during the buyer’s inspection – and you’ll have time to fix them or decide what to disclose before you put your house on the market.

This way, when the buyer’s inspector walks in, you’re ready. No surprises. No last-minute panic. No deal on the line.

Generally speaking, a pre-listing inspection costs just a few hundred dollars. So, it’s not a big expense. And the information it gives you is invaluable. But before you make that investment, talk to your local agent.

In some markets, it may not be worth it. And in others, it may be the best move you can make. It all depends on what’s happening where you are and what’s working for other local sellers. If your agent recommends getting one, they’ll also:

That small step could save your deal (and your timeline).

So, if there was one simple step that could help make your home sale go according to plan, would you do it?

If you’d rather deal with surprises on your terms (not with the clock ticking under contract), talk to an agent about whether a pre-listing inspection makes sense for your house.

It may be worth it so you can hit the market confident, prepared, and in control.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

There’s been a lot of talk lately about how a government shutdown impacts the housing market. You might be wondering: Is it causing everything to grind to a halt?

The short answer? No.

The housing market doesn’t stop. It keeps moving. Homes are still being bought and sold, contracts are still being signed, and closings are still happening. The difference is that a few parts of the process may slow down a little, but overall, the market continues to function.

Whenever the government shuts down, some federal agencies temporarily close or scale back their operations. That can cause a few hiccups in real estate, especially when it comes to processing certain types of government loans and insurance requirements:

Even with those challenges and delays, most transactions still go through. Buyers keep buying, sellers keep selling, and agents keep helping people move forward.

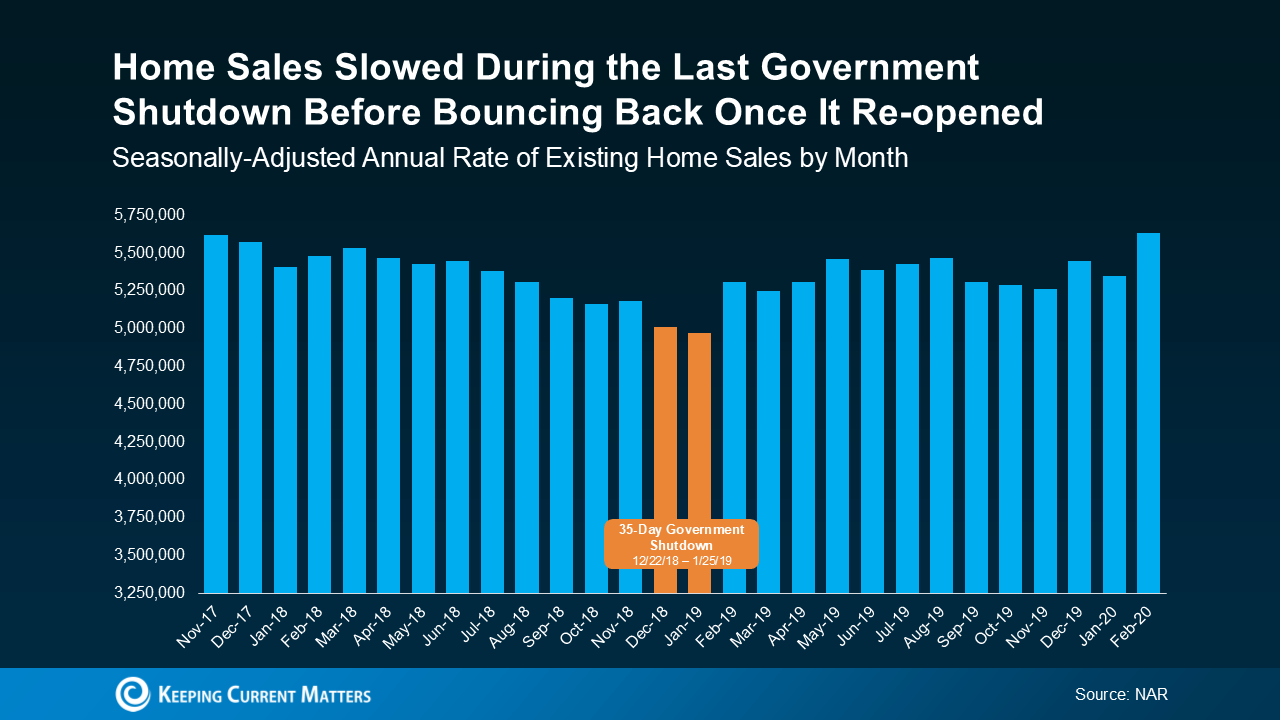

And you can see that play out in this data. If you look back at the most recent government shutdown that began at the end of 2018 and lasted for 35 days, sales activity dipped very slightly during the closure but picked right back up once the government reopened.

Data from the National Association of Realtors (NAR) shows existing home sales slowed for about two months, and then rebounded quickly as delayed closings worked their way through the system when the government reopened (see graph below):

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

If you’re in the middle of buying or selling a home, don’t panic. Most deals will still move forward, even if it takes a few extra days. Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“If you’re expecting to close in a week or a month, there could be some slight delay, but I think for most people, it’s probably going to be a blip more than a real deal killer.”

And if you’re just starting to think about buying or selling, this could actually work in your favor. Some buyers and sellers may become cautious and pause their plans during times of uncertainty, like this, and that can open a short window of opportunity.

When fewer people are active in the market, well-prepared buyers may find less competition for homes, and motivated sellers may be more willing to negotiate. These brief slowdowns often create a moment where you can make a move that would be harder once activity ramps back up.

A government shutdown can cause short-term delays for some buyers, but it doesn’t derail the housing market. The last time this happened, sales picked back up as soon as the government re-opened.

If you’re unsure how this might affect your plans, or just want to make sense of what’s happening, connect with a local real estate agent.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

A few years ago, inventory hit a record low. Just about anything sold – and fast. But now, there are far more homes on the market. Listings are up almost 20% from this time last year. And in some areas, supply is even back to levels we last saw in 2017–2019. For sellers, that means one thing:

Your house needs to stand out and grab attention from day one.

That’s especially true when you consider why the number of homes for sale is up. Here’s how it works. Available inventory is a mix of:

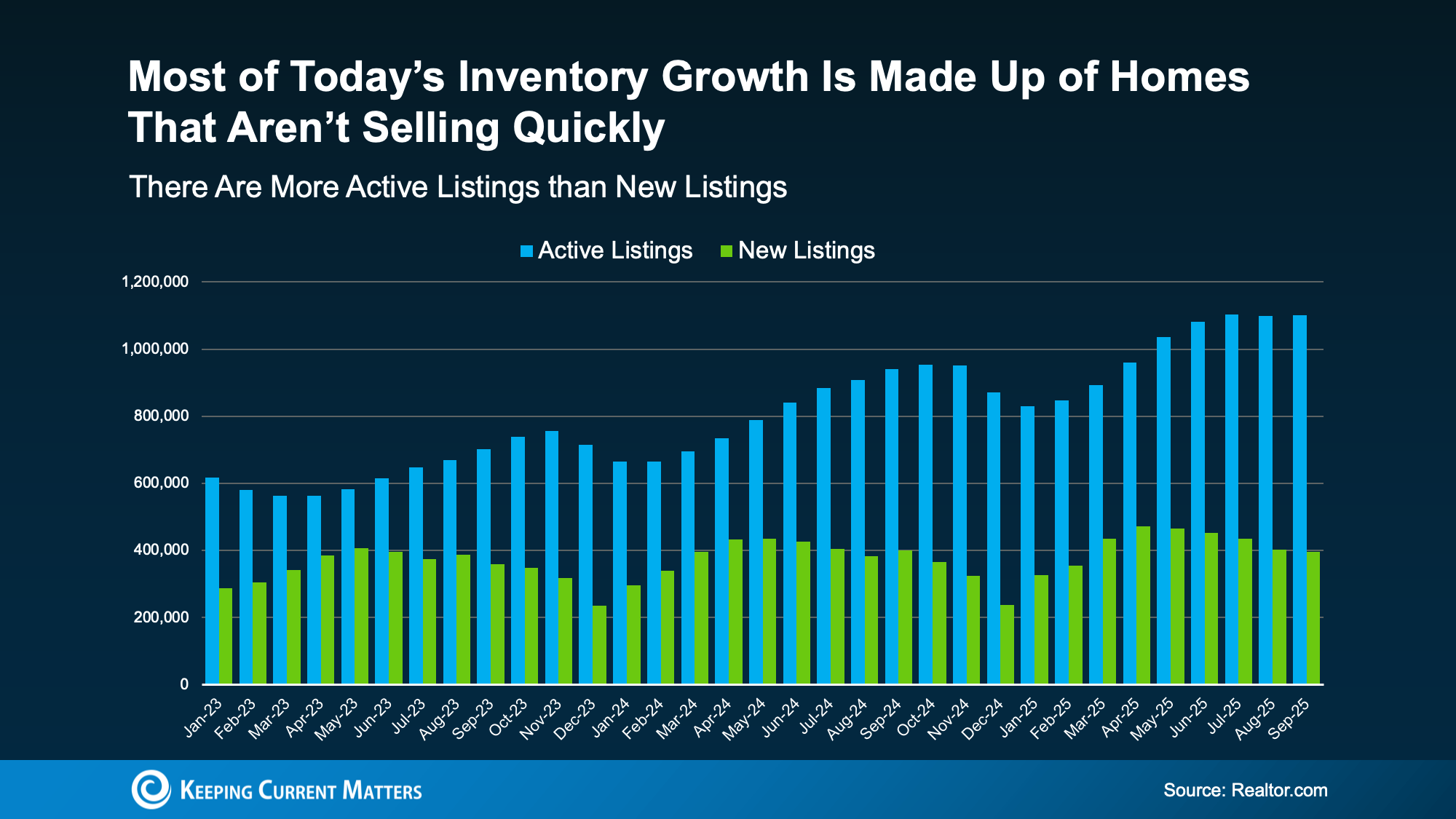

Data from Realtor.com shows most of the inventory growth lately is actually from active listings that are staying on the market and taking longer to sell (see the graph below).

The blue bars show active listings. These are the homes that are sitting month to month and not selling. The green bars are new listings, the homes that were just put on the market. And it’s clear there are fewer new listings compared to how many are staying on the market unsold.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

The secret to selling in today’s market is simple. Make sure your house is easy for buyers to say yes to as soon as it is listed.

Price it based on current conditions (not what your neighbor sold for 3 years ago). Make important repairs. And highlight the best things about your house. If you do that, it will sell in any market – sometimes even faster than you’d think. Because the truth is, homes that are priced right today are still selling.

It’s the homeowners who are clinging to outdated expectations that are seeing their house sit and their listing go stale. According to Redfin and HousingWire, here are some of the most common reasons sales stall out:

Most of those things didn’t matter as much just a few years ago. When inventory was at a record low, sellers could skip the prep, name their price, and still walk away with multiple offers over their asking price.

But today’s market is different now that inventory has grown. And that means your approach needs to be different too.

You don’t want to try out old strategies and aim too high just to see what sticks. Your first few weeks on the market are everything. That’s when your listing gets the most attention – and when pricing or presentation mistakes hurt the most. Get it wrong up front and your house will sit…and sit. Get it right, and it’ll be snatched up before you know it.

Selling quickly isn’t about luck. It’s about knowing how to play to the market you’re in. And that’s where your agent comes in.

A great agent will analyze your local market, suggest a price based on the latest comparables sold in your neighborhood, and create a marketing plan that makes buyers pay attention from day one. They’ll also walk you through any repairs you need to make or whether you need to bring in a staging company. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

That’s the power of getting it right (and getting expert help) from the start.

There are more homes for sale today, but that doesn’t have to work against you.

When your house is priced right, shows well, and is marketed effectively, it will sell. Connect with an agent if you want to know how to make that happen in your market this fall.

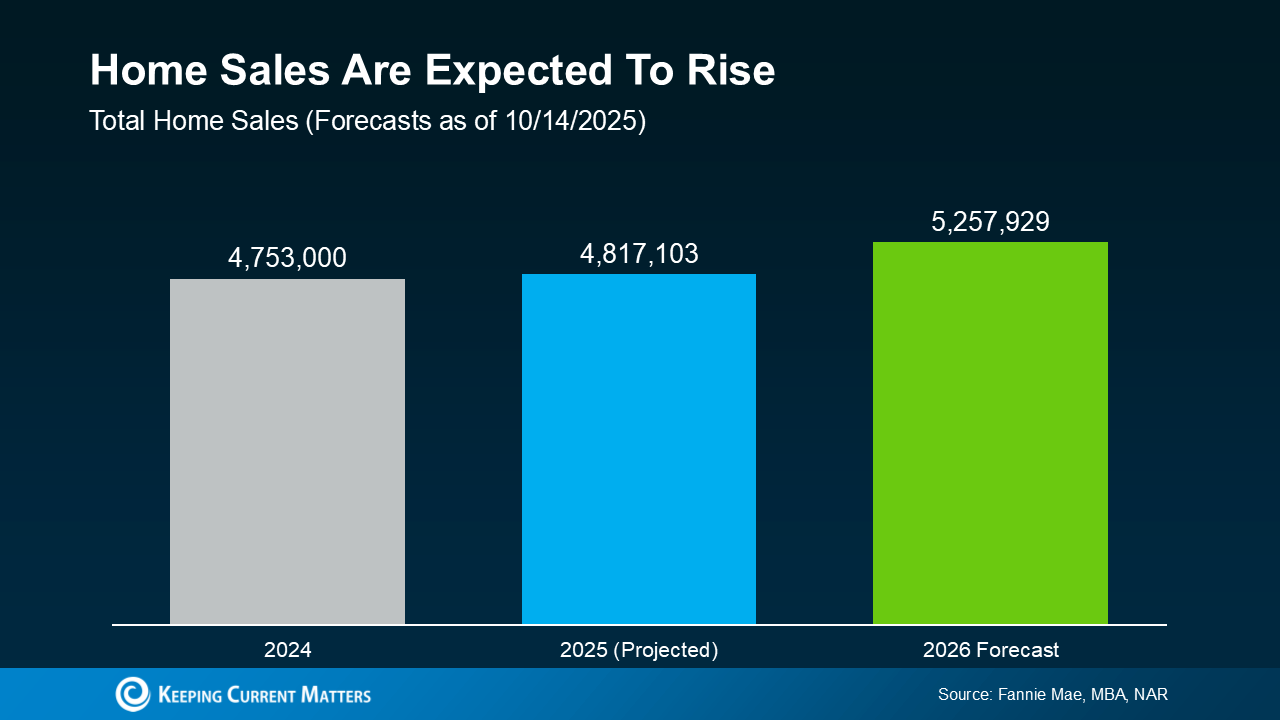

After a couple of years where the housing market felt stuck in neutral, 2026 may be the year things shift back into gear. Expert forecasts show more people are expected to move – and that could open the door for you to do the same.

With all of the affordability challenges at play over the past few years, many would-be movers pressed pause. But that pause button isn’t going to last forever. There are always people who need to move. And experts think more of them will start to act in 2026 (see graph below):

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

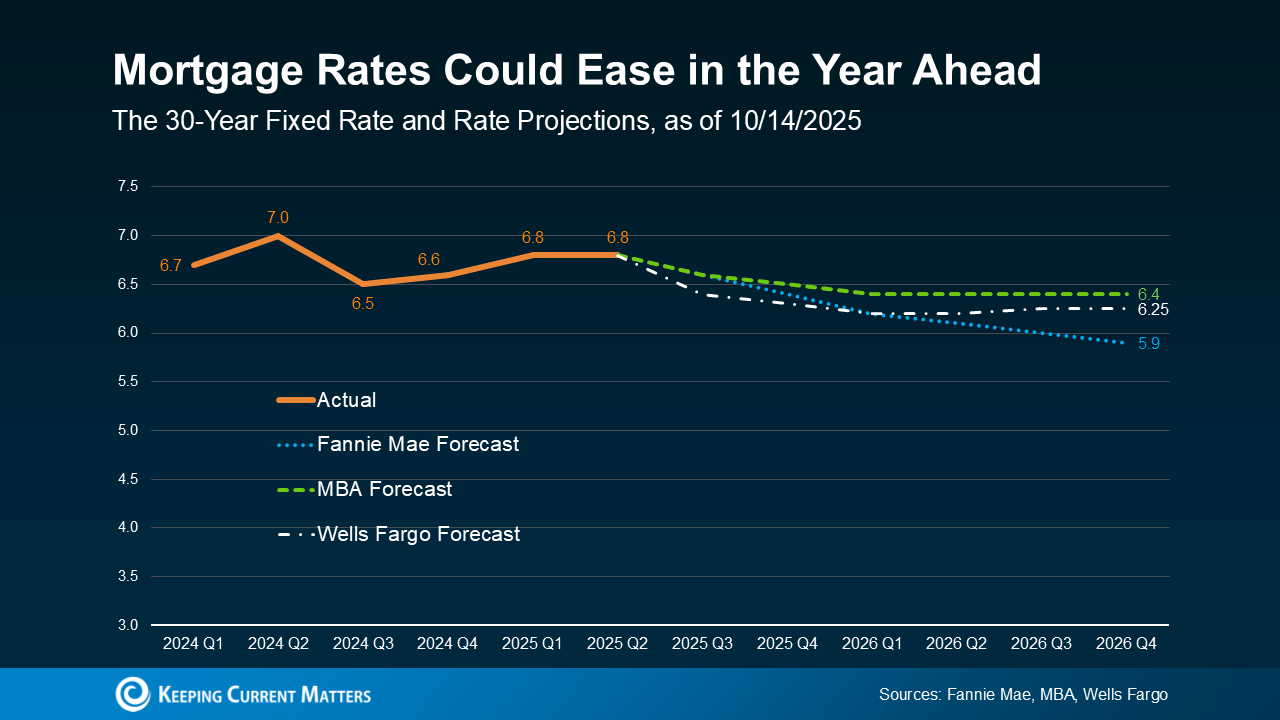

The #1 thing just about every buyer has been looking for is lower mortgage rates. And after peaking near 7% earlier this year, rates have started to ease.

The latest forecasts show that could continue throughout 2026, but it won’t be a straight line down (see graph below):

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

Expect modest improvement in mortgage rates over the next year but be ready for some volatility. There will be volatility along the way as new economic data comes out. Just don’t let it distract you from the bigger picture: the overall trend will be a slight decline. Forecasts say we could hit the low 6s, or maybe even the high 5s.

And remember, there doesn’t have to be a big drop for you to feel a change. Even a smaller dip helps your bottom line.

If you compare where rates are now to when they were at 7% earlier this year, you’re already saving hundreds on your future mortgage payment. And that’s a really good thing. It’s enough to make a real difference in affordability for some buyers.

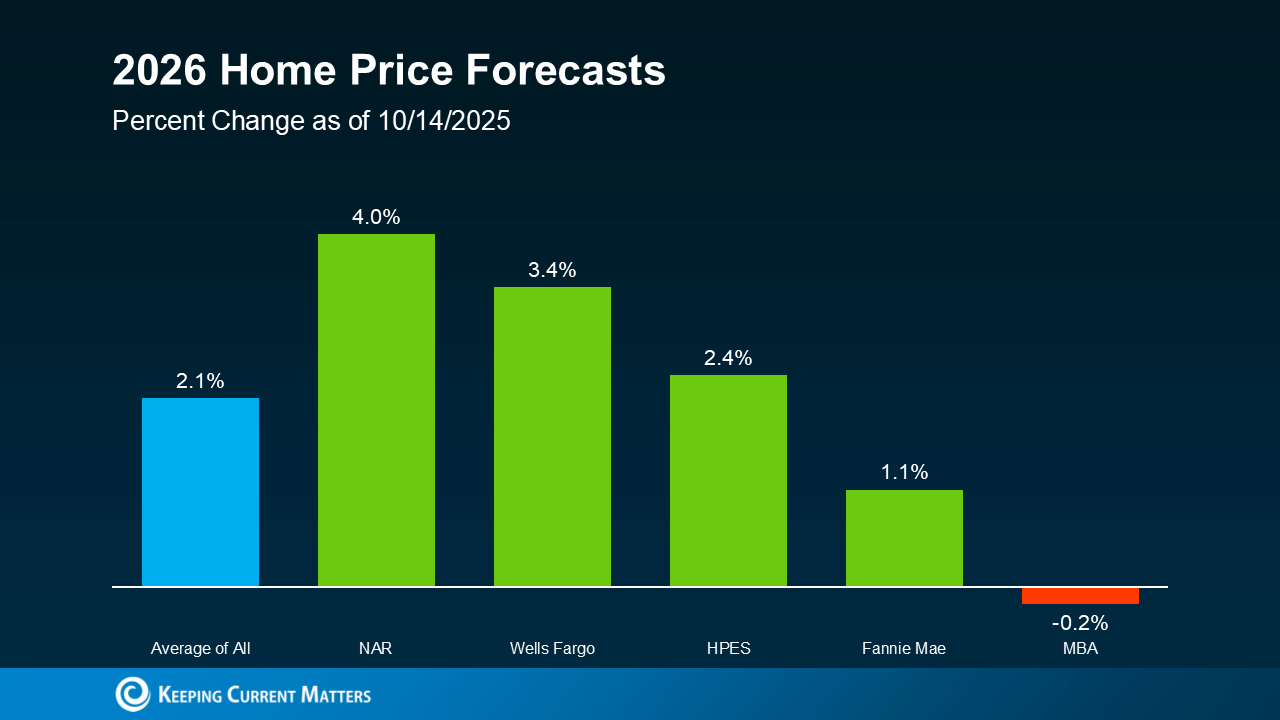

What about prices? On a national scale, forecasts say they’re still going to rise, just not by a lot. With rates down from their peak earlier this year, more buyers will re-enter the market. And that increased demand will keep some upward pressure on prices nationally – and prevent prices from tumbling down.

So, even though some markets are already seeing slight price declines, you can rest easy that a big crash just isn’t in the cards. Thanks to how much prices rose over the last 5 years, even the markets seeing declines right now are still up compared to just a few years ago.

Of course, price trends will depend on where you are and what’s happening in your local market. Inventory is a big driver in why some places are going to see varying levels of appreciation going forward. But experts agree we’ll see prices grow at the national level (see graph below):

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

After a quieter couple of years, 2026 is expected to bring more movement – and more opportunity. With sales projected to rise, mortgage rates trending lower, and price growth slowing down, the stage is set for a healthier, more active market.

So, the big question: will you be one of the movers making 2026 your year?

Connect with an agent if you want to get ready.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.