Realty Executives Midwest

October is one of the best times of year to plan a home renovation. As the weather cools down, many homeowners are looking to refresh their living spaces and get ready for the holidays.

Whether you’re considering a bathroom remodel, flooring upgrade, or basement renovation, fall offers the perfect opportunity to begin your project before the busy holiday season.

Ideal Weather Conditions: The cooler fall temperatures create the perfect environment for both interior and exterior work. From painting and flooring installation to tile work and carpentry, projects move efficiently without the humidity and heat of summer.

Be Ready for the Holidays: Starting your renovation in October gives you enough time to complete it before family gatherings and celebrations. A newly renovated bathroom or updated kitchen makes entertaining guests easier and more enjoyable.

Seasonal Material Discounts: Many suppliers offer end-of-year promotions on flooring, cabinetry, and fixtures. Fall is the perfect time to take advantage of these savings while updating your home with modern, high-quality materials.

Bathroom Remodeling: A bathroom remodel can transform one of the most used spaces in your home. This season, many homeowners are choosing porcelain tile, brushed gold hardware, and light neutral paint tones to create a spa-like retreat. Even small upgrades—like new lighting or fixtures—can make a big difference.

Flooring Installation: New flooring is one of the fastest ways to refresh your space. Our team installs vinyl, laminate, engineered hardwood, and tile flooring with precision and care. Fall’s steady temperatures help ensure a smooth and lasting finish.

Kitchen Upgrades: From shaker-style cabinet doors and quartz countertops to modern backsplash designs, a kitchen update can completely transform the heart of your home.

Basement Finishing and Remodeling: Turn your unused basement into a cozy living area, gym, or home office. A finished basement adds both comfort and value to your home—especially as we head into the colder months.

“Fall is all about layering textures and creating warmth through design. Combining wood finishes, soft neutrals, and modern fixtures can make any room feel more inviting. The goal is to design spaces that look beautiful and function beautifully for everyday living.”— Gabriela, Interior Designer at Real Time Home Improvement

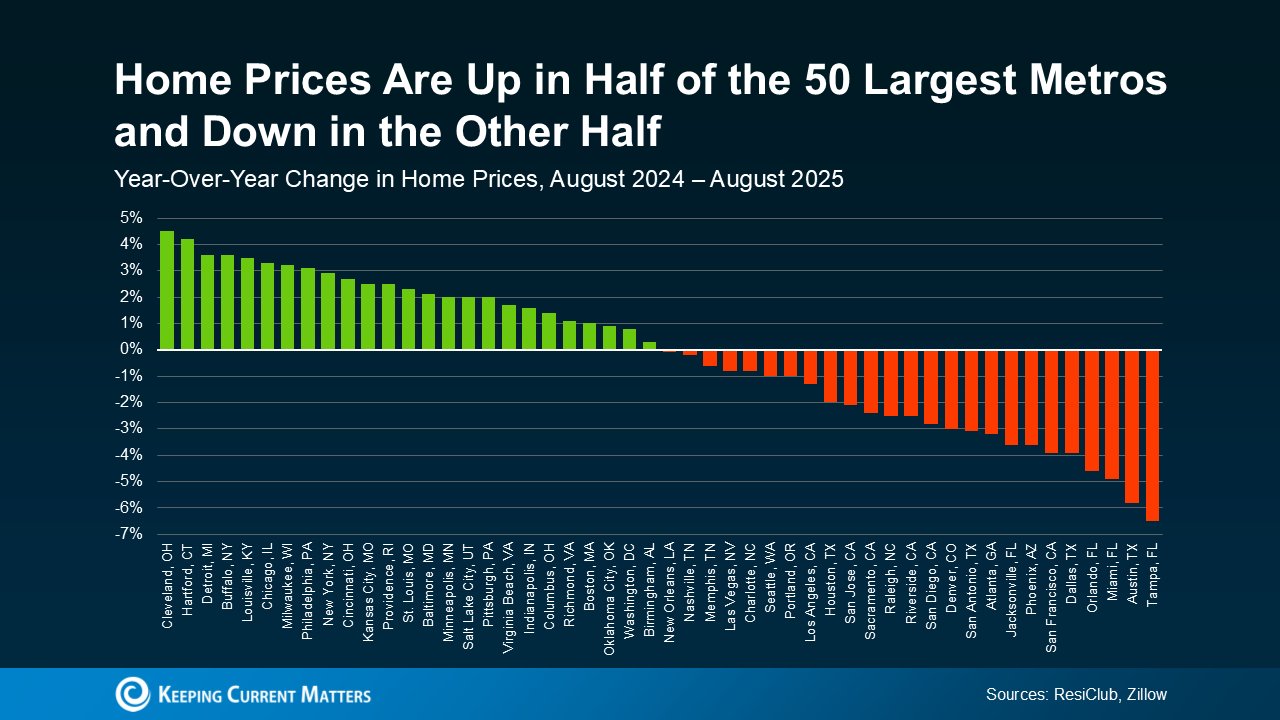

If you’ve been following real estate news lately, you’ve probably seen headlines saying home prices are flat. And at first glance, that sounds simple enough. But here’s the thing. The reality isn’t quite that straightforward.

In most places, prices aren’t flat at all.

While we’ve definitely seen prices moderate from the rapid and unsustainable climb in 2020-2022, how much they’ve changed is going to be different everywhere.

If you look at data from ResiClub and Zillow for the 50 largest metros, this becomes very clear. The real story is split right down the middle. Half of the metros are still seeing prices inch higher. The other half? Prices are coming down slightly (see graph below).

The big takeaway here is “flat” doesn’t mean prices are holding steady everywhere. What the numbers actually show is how much price trends are going to vary depending on where you are.

The big takeaway here is “flat” doesn’t mean prices are holding steady everywhere. What the numbers actually show is how much price trends are going to vary depending on where you are.

One factor that’s driving the divide? Inventory. The Joint Center for Housing Studies (JCHS) of Harvard University explains:

“ . . . price trends are beginning to diverge in markets across the country. Prices are declining in a growing number of markets where inventories have soared while they continue to climb in markets where for-sale inventories remain tight.”

When you average those very different trends together, you get a number that looks like it’s flat. But it doesn’t give you the real story and it’s not what most markets are feeling today. You deserve more than that.

And just in case you’re really focusing on the declines, remember those are primarily places where prices rose too much, too fast just a few years ago. Prices went up roughly 50% nationally over the past 5 years, and even more than that in some of the markets that are experiencing a bigger correction today. So, a modest drop in some local pockets still puts most of those homeowners ahead when it comes to the overall value of their home. And based on the fundamentals of today’s housing market, experts are not projecting a national decline going forward.

So, what’s actually important for you to know?

You need to know what’s happening in your area because that’s going to influence everything from how quickly you need to make an offer to how much negotiating power you’ll have once you do.

The bottom line? Knowing your local trend puts you in the driver’s seat.

You’ll want to be aware of local trends, so you’ll know how to price your house and how much you can expect to negotiate.

The big action item for homeowners? Sellers need to have an agent’s local perspective if they want to avoid making the wrong call on pricing – and homes that are priced right are definitely selling.

The national averages can point to broad trends, and that’s helpful context. But sometimes you’re going to need a local point of view because what’s happening in your zip code could look different. As Anthony Smith, Senior Economist at Realtor.com, article puts it:

“While national prices continued to climb, local market conditions have become increasingly fragmented…This regional divide is expected to continue influencing price dynamics and sales activity as the fall season gets underway.”

That’s why the smartest move, whether you’re buying or selling, is to lean on a local agent who’s an expert on your market.

They’ll have the data and the experience to tell you whether prices in your area are holding steady, moving up, or softening a bit – and how that could impact your move.

Headlines calling home prices flat may be grabbing attention, but they’re not giving you the full picture.

Has anyone taken the time to walk you through what’s happening in your market?

If you want the real story about what prices are doing in your area, connect with a local agent.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

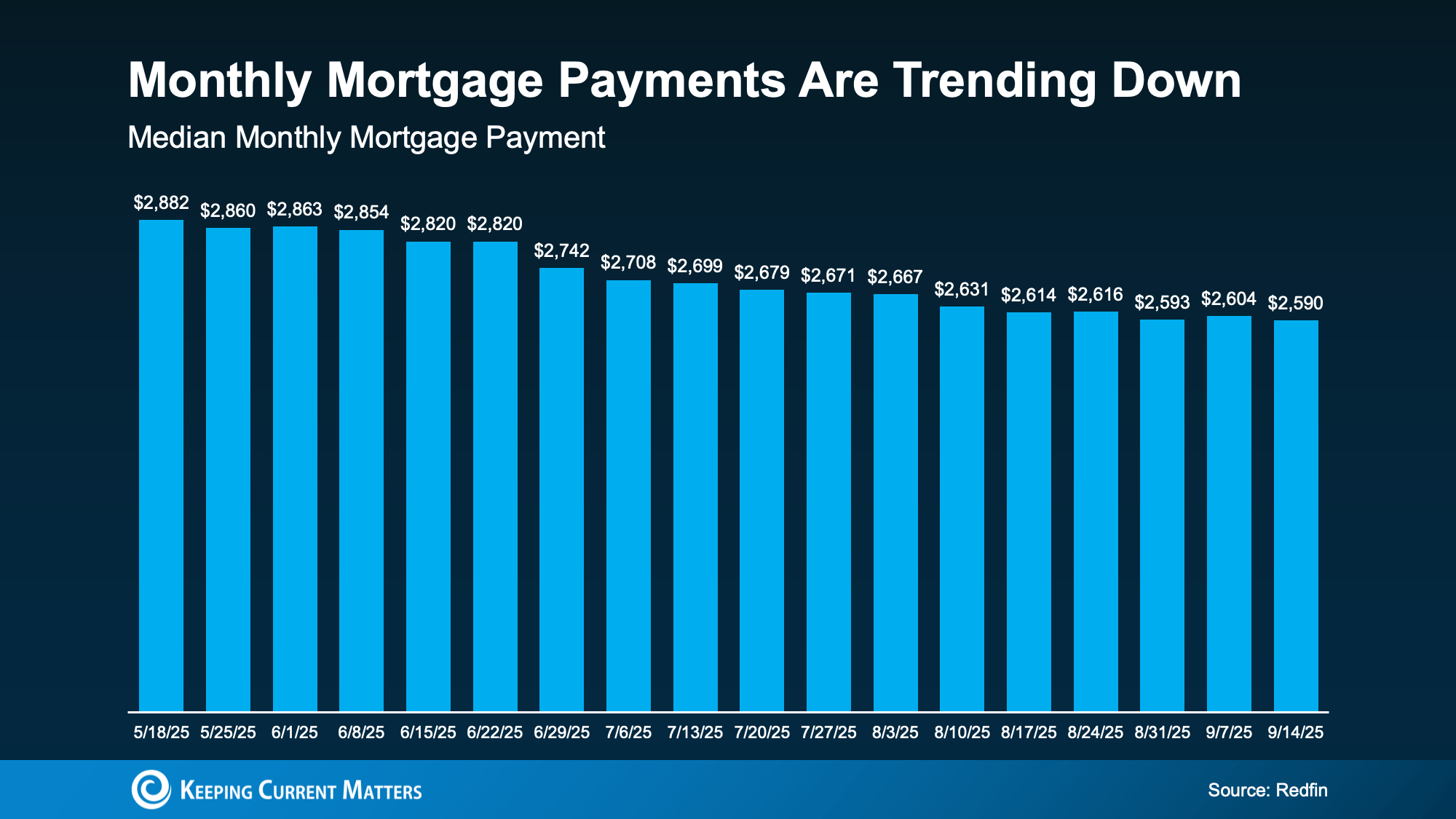

For the past couple of years, it’s been tough for a lot of homebuyers to make the numbers work. Home prices shot up. Mortgage rates too. And a number of people hit pause because it just didn’t feel possible. Maybe you were one of them.

But there’s some encouraging news. If you’ve been waiting for a better time to jump back in, affordability may finally be showing signs of improvement this fall.

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here’s why this is happening. The cost of buying a home really comes down to three things:

And here’s why this is happening. The cost of buying a home really comes down to three things:

Right now, all three are finally moving in a better direction for you. While that doesn’t mean it’s suddenly easy to buy at today’s rates and prices, it does mean it’s not as challenging.

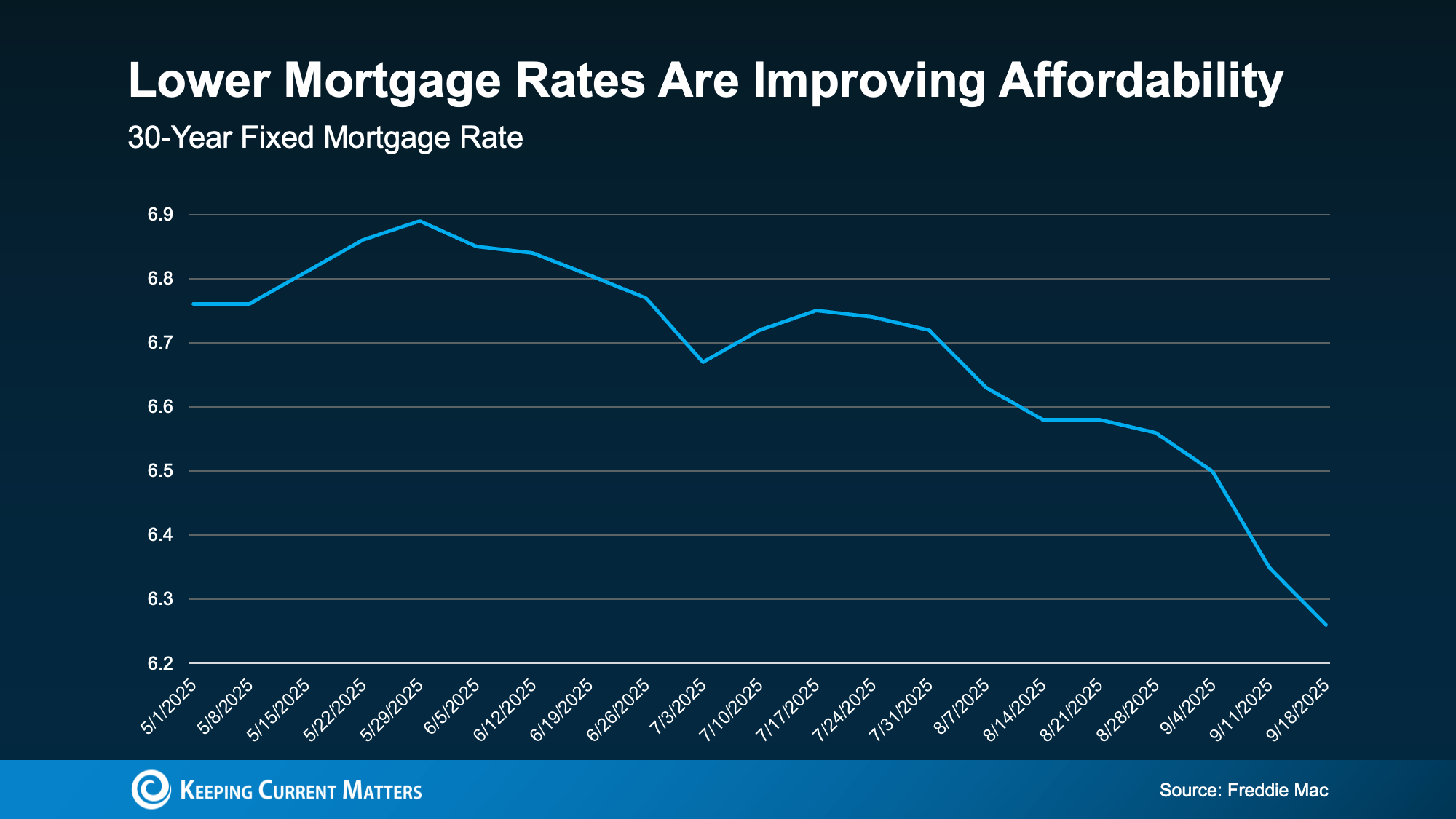

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they’re closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

And for some people, that’s been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

For buyers, that’s actually a big relief. That moderation makes it easier to plan your budget. And in some markets, prices have even dipped slightly. If you’re in one of the markets, you may be able to find something that’s more affordable than you’d expect.

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it’s not a big difference, but in a market like this, every bit counts.

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it’s a little easier on your wallet to buy now than it was just few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year.

Have you been wondering if it’s worth taking another look at buying?

Work with a professional to re-run the numbers. Together you can go over your budget, see what’s changed, and figure out if this fall is the time to turn window-shopping into key-turning.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

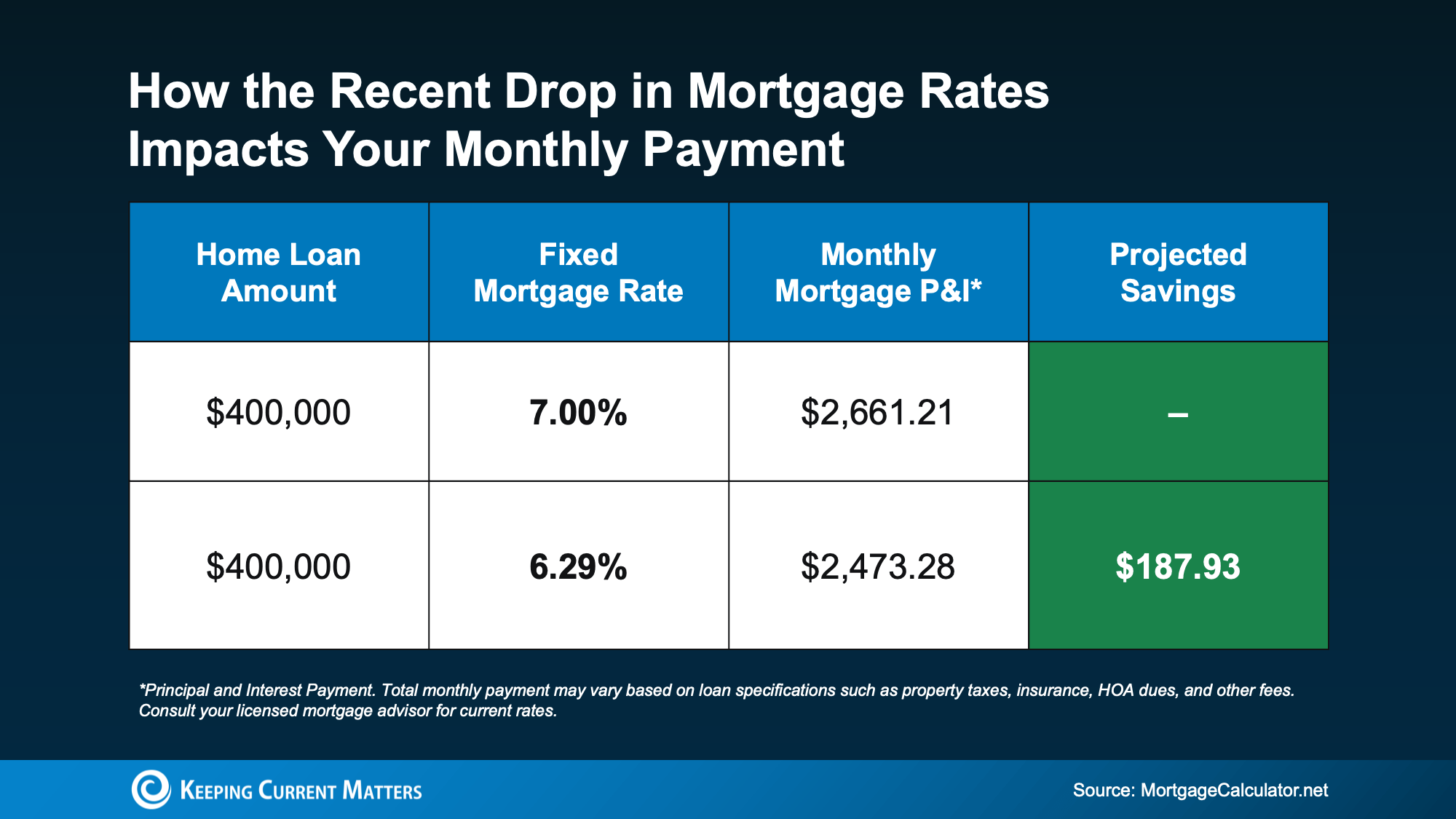

You’ve been waiting for what feels like forever for mortgage rates to finally budge. And last week, they did – in a big way.

On Friday, September 5th, the average 30-year fixed mortgage rate fell to the lowest level since October 2024. It was the biggest one-day decline in over a year.

According to Mortgage News Daily, this was a reaction to the August jobs report, which came out weaker-than-expected for a second month in a row. That sent signals across the financial markets, and then mortgage rates came down as a result.

Basically, we’re seeing signs the economy may be slowing down, and as certainty grows in the direction the economy is going, the markets are reacting to what is likely ahead. That historically brings mortgage rates down.

But this isn’t just about one day of headlines or one report. It’s about what the drop means for you.

This recent change saves you money when you buy a home. The chart below shows you an example of what a monthly mortgage payment (principal and interest) would be at 7% (where mortgage rates were in May) versus where rates roughly are now:

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

That really depends on where the economy and inflation go from here. Rates could drop lower, or they could inch up slightly.

So, make sure you’re connected with a good agent and trusted lender. They’ll keep a close eye on inflation indicators, job market updates, and reactions to upcoming Fed policy to gauge where mortgage rates may go from here.

But for now, focus on this. While no one can say for sure where rates are headed, the fact that rates broke out of their months-long rut is a good thing. If you’ve been feeling stuck, this could make the start of a new chapter. As Diana Olick, Senior Real Estate and Climate Correspondent at CNBC, says:

“Rates are finally breaking out of the high 6% range, where they’ve been stuck for months.”

And that’s gives you more reason to hope than you’ve had in quite some time.

This is the shift you’ve been waiting for.

Mortgage rates just saw their biggest decline in over a year. And if rates stay near this level, it could make a home you couldn’t afford just a few months ago feel possible again.

What would today’s rates save you on your future monthly payment? Connect with an agent or lender so you can find out.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

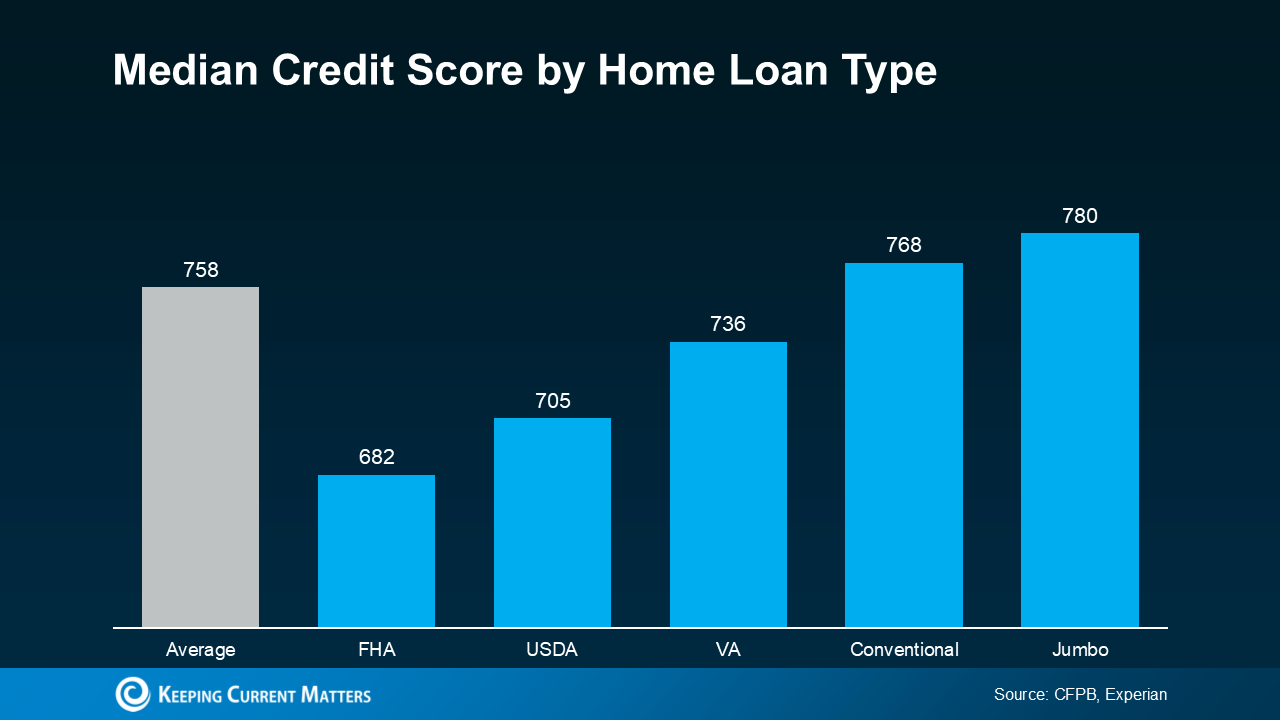

According to Fannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most homebuyers think they need better credit than they actually do – and maybe you’re one of them. And that could make you think buying a home is out of reach for you right now, even if that’s not necessarily true. So, let’s look at what the data really says about credit scores and homebuying.

There’s no universal credit score you absolutely have to have when buying a home. And that means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had among different home loan types:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

When you buy a home, lenders use your credit score to get a sense of how reliable you are with money. They want to see if you typically make payments on time, pay back debts, and more.

Your score can impact which loan types you may qualify for, the terms on those loans, and even your mortgage rate. And since mortgage rates are a big factor in how much house you’ll be able to afford, that may make your score feel even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That still doesn’t mean your credit has to be perfect. Even if your credit score isn’t as high as you’d like, you may still be able to get a home loan.

And if you talk to a lender and decide you want to improve your score (and hopefully your loan type and terms too), here are a few smart moves according to the Federal Reserve Board:

Your credit score doesn’t have to be perfect to qualify for a home loan. But a better score can help you get better terms on your home loan. The best way to know where you stand and your options for a mortgage is to connect with a trusted lender.?

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.