Realty Executives Midwest

If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.

In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the trends, and what they mean for your search.

According to Realtor.com, the national median asking price was $430,000 in June, nearly $11,000 under what it was the year before (see graph below):

That’s the eighth month in a row that the typical asking price has dipped below where they were the previous year, according to the same Realtor.com report.

And while falling prices can sound worrying, this isn’t a sign of an impending crash. We’re talking about asking prices, not sold prices. This is a sign that today’s sellers are meeting the market where it is and pricing to draw buyers. And that’s actually something normal we’d expect from the market. As Danielle Hale, Chief Economist at Realtor.com, puts it:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to climb forever – now they’re just settling closer to what buyers can actually pay. That signals a healthier market, and sellers re-adjusting their expectations.

If you’ve spent the past few years watching homes disappear before you could even schedule a tour, this is for you.

Supply is starting to catch up. According to Realtor.com, the number of homes listed for sale in June was the highest June number we’ve seen in three years (see graph below):

This means more options for you and less competition for each one.

Now, supply is not back to normal everywhere. As you can see, we’re still down from where we were back in 2017-2019. But in many places, it’s better than it’s been in a while. Here’s how that helps you.

You don’t have to rush an offer just to stay in the running, and you have better odds of finding and landing the right home, not just the one that’s available. Plus, you’ll have more room to negotiate, so you’re searching from a stronger position than buyers had even a year ago.

For first-time buyers looking for lower-priced homes, these trends line up especially well. Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

So, if you’re searching for your first place or your next house, there’s a little more to choose from and a little more give on price.

If a tight budget or a thin selection has kept you from buying a home, now might be the time to restart your search.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

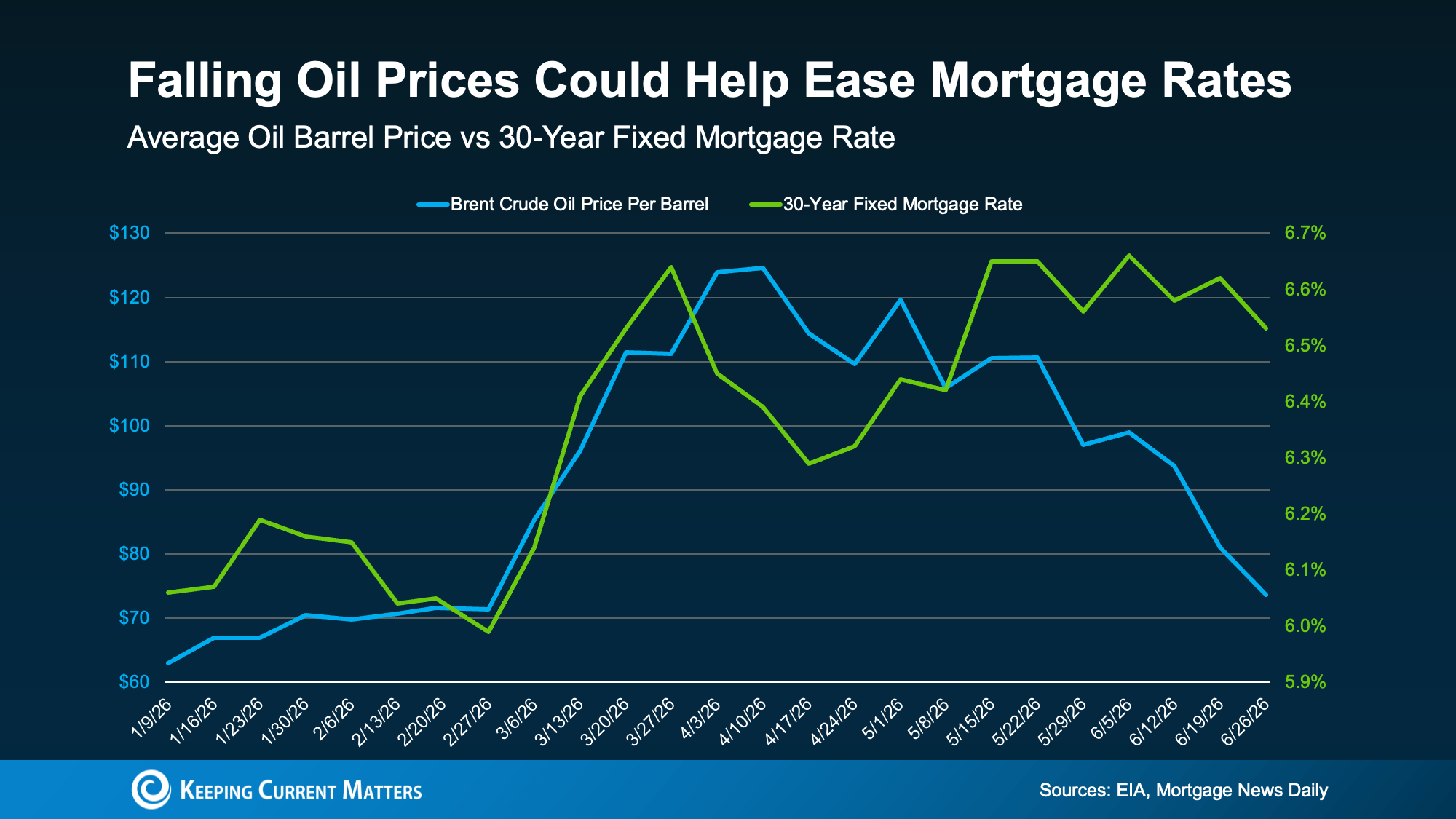

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

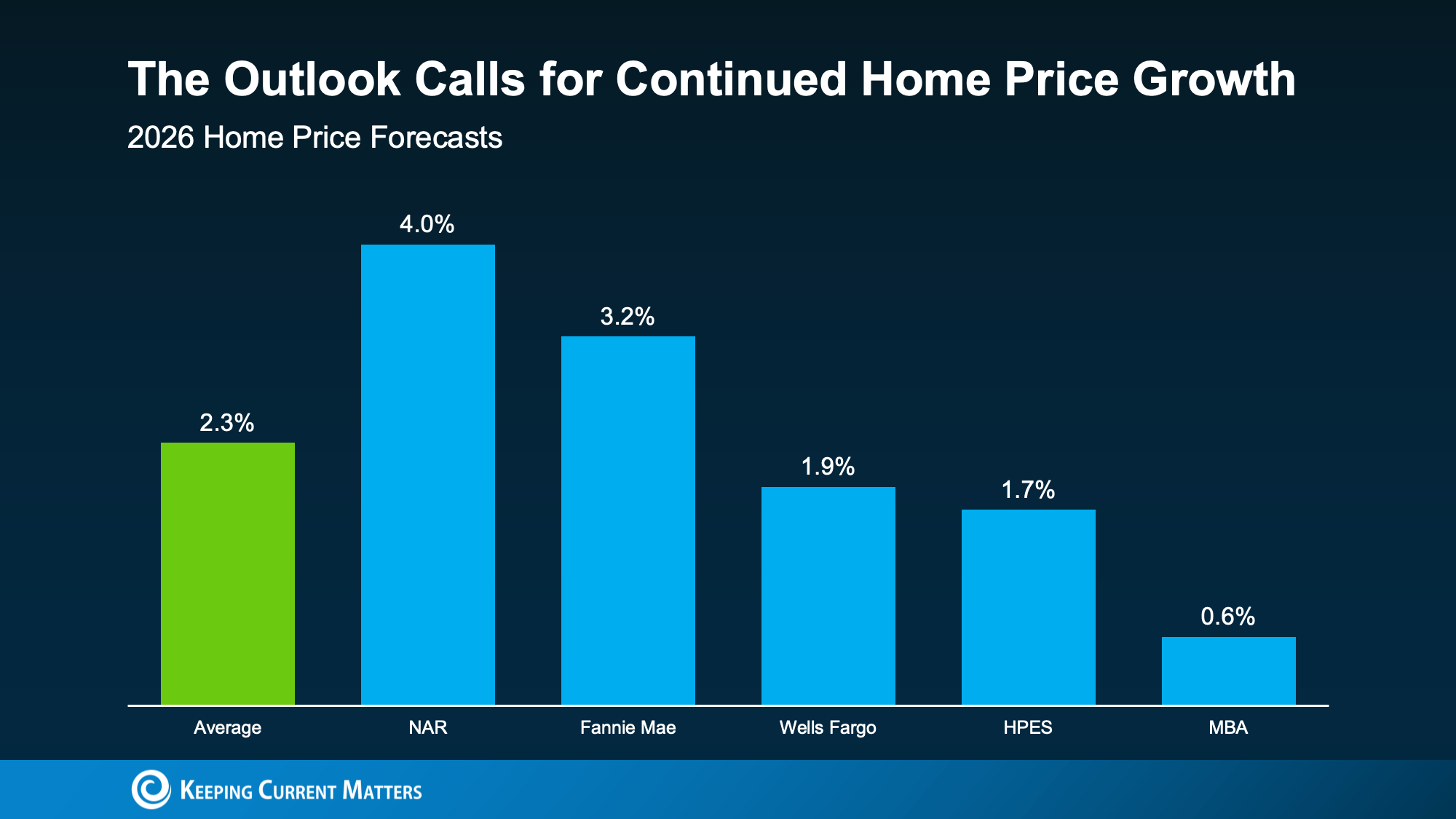

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

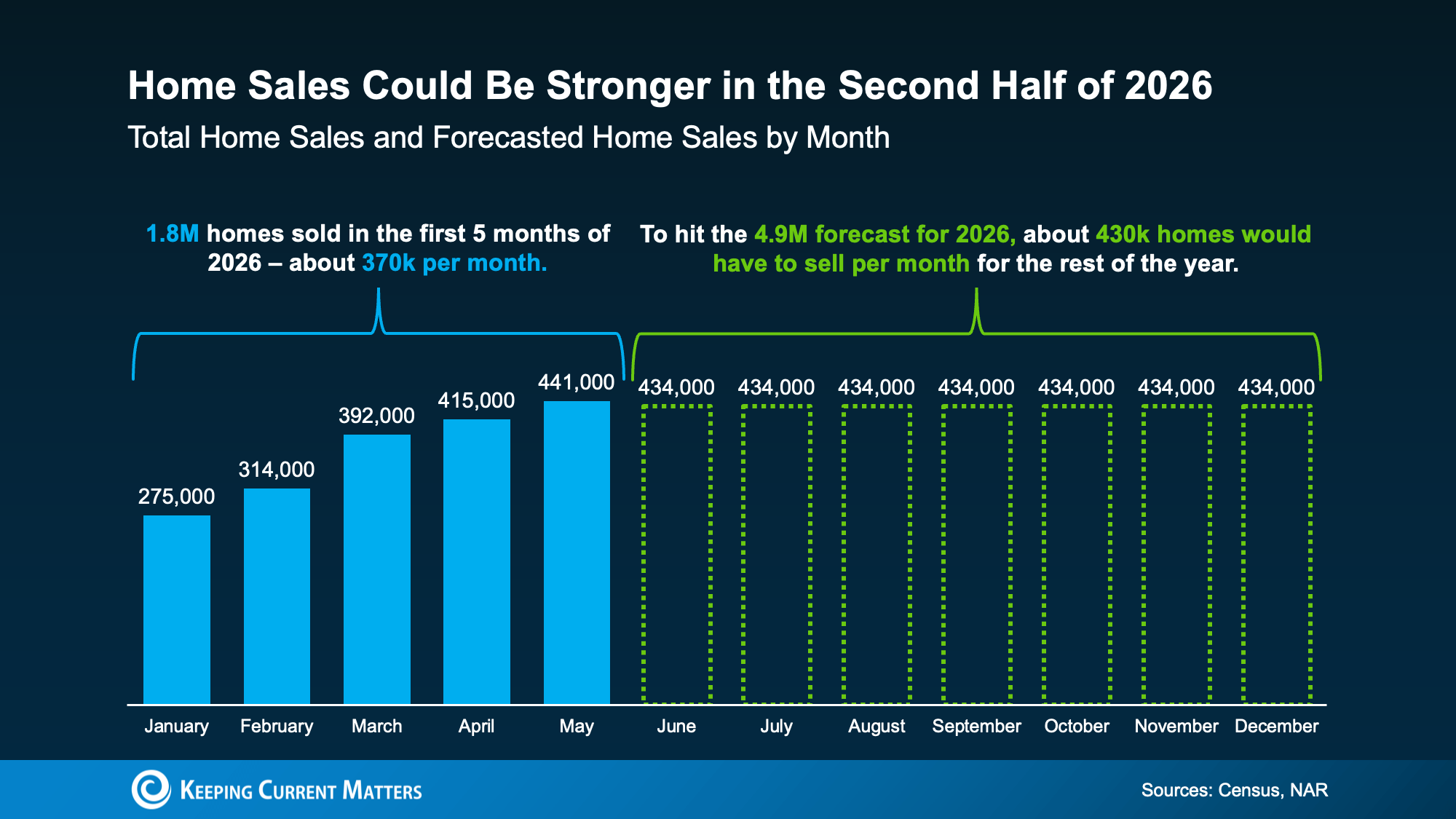

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

The second half of the year probably won't be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you've been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in your local market, connect with an agent.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

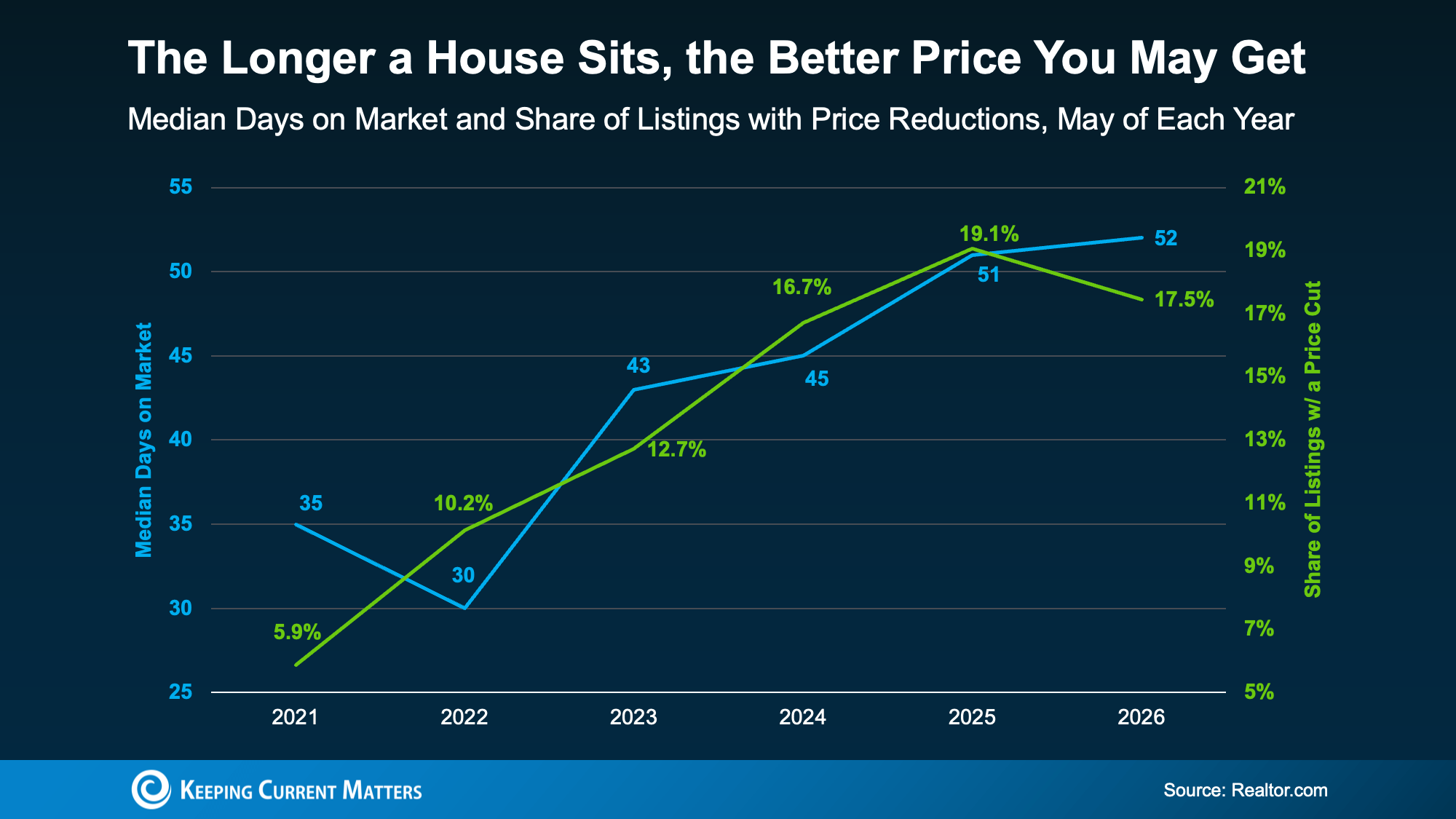

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

The asking price was set too high to start

The home didn’t show well online

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, connect with a local real estate agent.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Summer is the perfect time to enjoy backyard barbecues, gardening, evenings on the patio, and outdoor family activities. Unfortunately, warmer temperatures also bring mosquitoes, flies, ants, wasps, and other unwanted pests that can quickly put a damper on outdoor fun.

The good news is that keeping summer pests under control doesn’t always require harsh chemicals. With a combination of preventative maintenance, strategic landscaping, and natural repellents, homeowners can create a more comfortable outdoor environment while minimizing the impact on people, pets, and beneficial pollinators.

One of the most effective ways to reduce mosquito populations is to eliminate standing water around your property. Mosquitoes can lay eggs in surprisingly small amounts of water, making even minor sources a potential breeding ground.

Regularly inspect your property for:

Refreshing bird bath water every few days and ensuring proper drainage throughout your yard can significantly reduce mosquito activity.

Certain plants are known for their natural insect-repelling properties and can be attractive additions to patios, gardens, and outdoor living spaces.

Popular options include:

While these plants won’t eliminate insects entirely, they can help discourage some pests while adding beauty and fragrance to your outdoor spaces.

As an added benefit, many of these herbs can also be used in summer recipes and beverages.

Pests thrive in areas where they can hide, nest, and access moisture. Maintaining your landscape can make your property less inviting to unwanted visitors.

Simple steps include:

A tidy yard not only helps reduce pests but also improves curb appeal and creates a more enjoyable outdoor environment.

Seal Entry Points Around Your Home

Summer pests don’t just stay outside. Ants, spiders, flies, and other insects often find their way indoors through small gaps and openings.

Take time to inspect:

Replacing damaged screens and sealing openings can help keep insects outside where they belong.

For homeowners who prefer alternatives to traditional chemical insecticides, there are several natural options available.

Many natural bug sprays use plant-based ingredients such as:

These products are often used to repel mosquitoes and other common insects around patios, decks, and outdoor seating areas.

When shopping for natural repellents, look for products specifically labeled for outdoor pest control and follow all manufacturer instructions. Some sprays are designed for personal use on skin or clothing, while others are formulated for treating outdoor areas and landscaping.

It’s important to remember that natural repellents may require more frequent application than conventional products, especially after rain or extended outdoor use.

Outdoor entertaining areas often become gathering places for both guests and insects.

To help keep bugs at bay:

Many flying insects struggle in moving air, making outdoor fans a surprisingly effective addition to patios and decks.

Not all insects belong on the “unwanted” list. Many species play important roles in maintaining a healthy ecosystem.

Birds, dragonflies, and certain beneficial insects naturally feed on mosquitoes and other pests. Creating a balanced landscape with native plants can help attract these helpful visitors while supporting local biodiversity.

The goal isn’t to eliminate all insects—it’s to create a healthier outdoor environment where pest populations remain manageable.

Summer should be a time for relaxing outdoors, not constantly swatting away insects. By eliminating standing water, maintaining your landscape, sealing entry points, and using natural repellents when needed, you can create a more comfortable outdoor space without relying heavily on harsh chemicals.

Small preventative measures often make the biggest difference. A few simple habits can help keep summer pests under control while allowing you to enjoy everything the season has to offer—from backyard gatherings to peaceful evenings on the patio.

Source: Realty Executives

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

While waiting sounds like a good plan, there’s something worth knowing before you decide. Rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there may be other things you miss out on in the meantime.

Historically, Summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until Fall or Winter, some of those opportunities may already be fading.

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

You find a house you like, but it’s out of your budget.

You find something in your budget, but you don’t like it.

Or worse, nothing interesting hits the market for weeks.

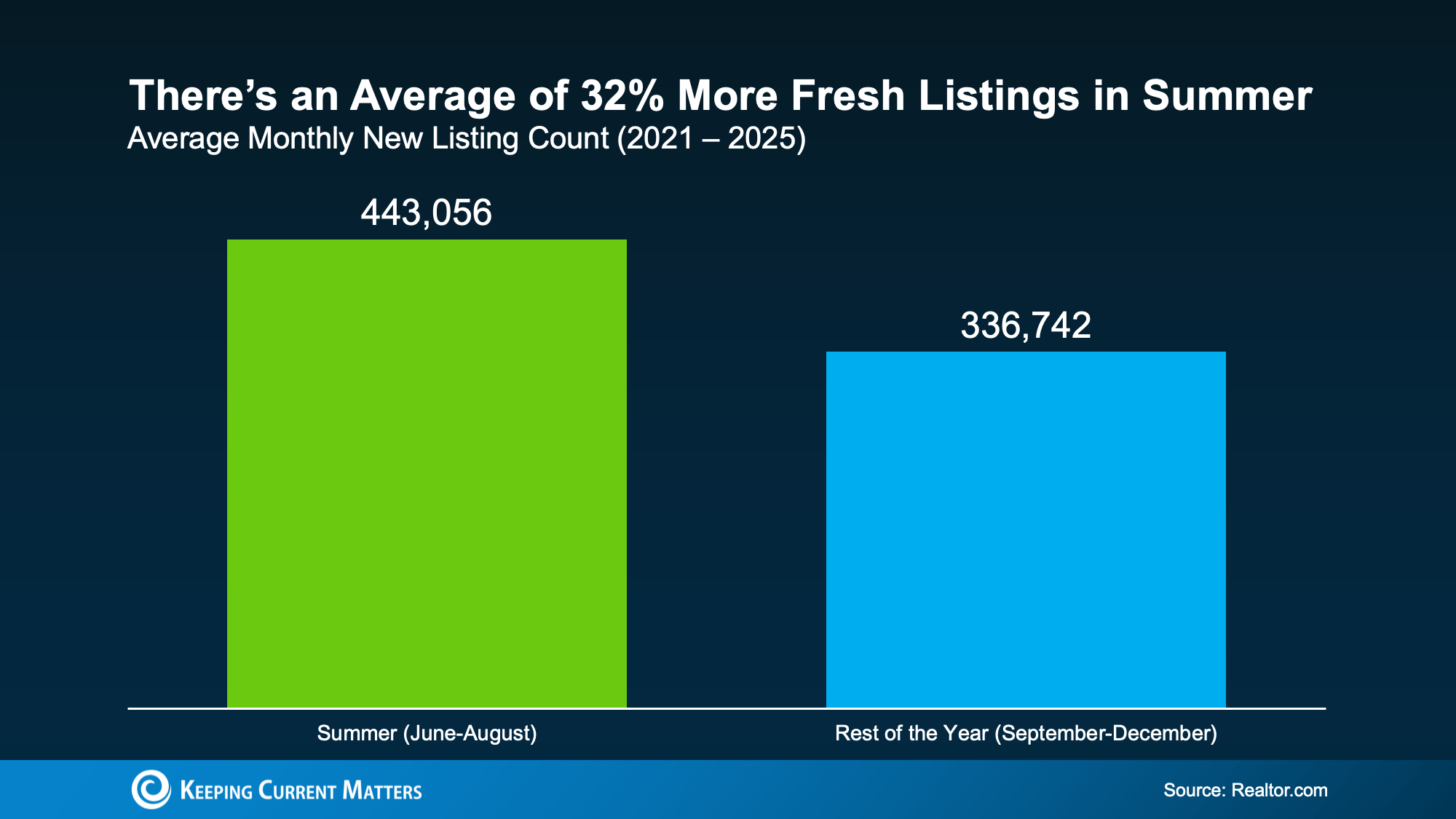

Historically, Summer helps with that.

Looking at data from the last few years, Summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given Summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into Fall and Winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

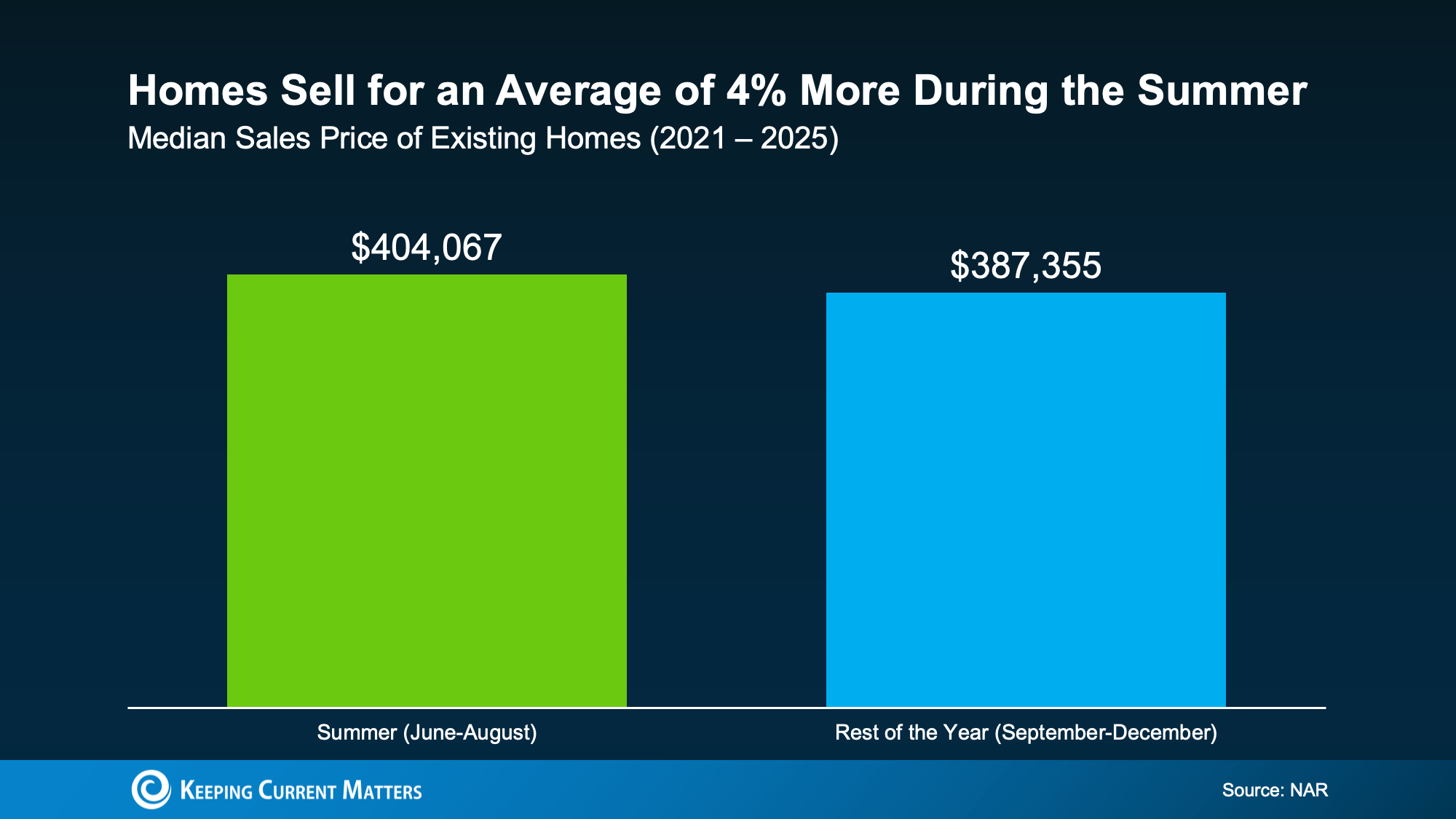

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

According to the National Association of Realtors (NAR), homes sold during a Summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this Summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a Summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the Fall or Winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Could waiting until later this year work out? Sure. But it's important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, talk to an agent about what matters most to you. Depending on your priorities, Summer could be your moment.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.