Realty Executives Midwest

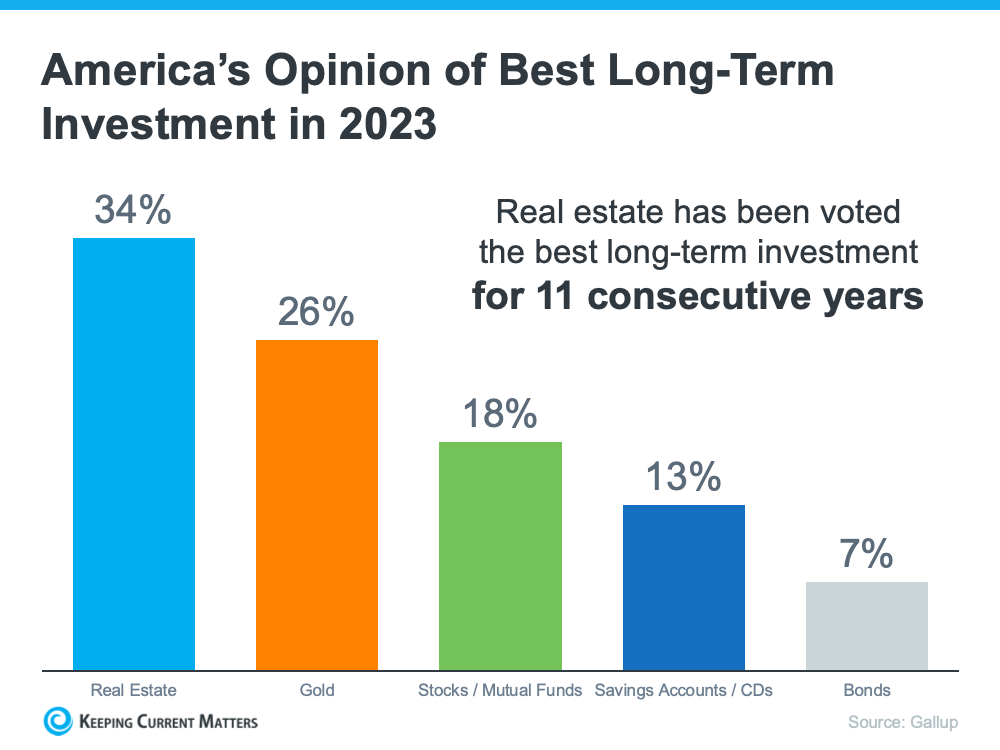

With all the headlines circulating about home prices and rising mortgage rates, you may wonder if it still makes sense to invest in homeownership right now. A recent poll from Gallup shows the answer is yes. In fact, real estate was voted the best long-term investment for the 11th consecutive year, consistently beating other investment types like gold, stocks, and bonds (see graph below):

If you’re thinking about purchasing a home, let this poll reassure you. Even with everything happening today, Americans recognize owning a home is a powerful financial decision.

Purchasing real estate has typically been a solid long-term strategy for building wealth in America. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“. . . homeownership is a catalyst for building wealth for people from all walks of life. A monthly mortgage payment is often considered a forced savings account that helps homeowners build a net worth about 40 times higher than that of a renter.”

That’s because owning a home grows your net worth over time as your home appreciates in value and as you pay down your mortgage. And, since building that wealth takes time, it may make sense to start as soon as you can. If you wait to buy and keep renting, you’ll miss out on those monthly housing payments going toward your home equity.

Buying a home is a powerful decision. So, it’s no wonder so many people view real estate as the best long-term investment. If you’re ready to start on your own journey toward homeownership, connect with a local real estate advisor today.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

If you’re considering selling your house or a rental property, you may be asking what you can do to increase its value before it goes on the market. Even if selling is not in the cards right now but you are thinking about making home improvements, it is always a good idea to ensure you are getting the most bang for your money.

With that in mind, let us look at five ways to add significant value to your property. Then you can decide which upgrades will be most beneficial for you and your family while also boosting your home value significantly.

When it comes to drawing buyer interest, curb appeal is crucial, but it doesn’t have to stop at a lovely lawn and garden. Replacing or simply repainting your front door can increase the value of your home.

According to Remodeling’s Cost vs. Value Report, a new steel door can return 65% of its cost, while a fiberglass door can reclaim 60.9%. Even a fresh coat of paint on an old door may make a difference. According to a Zillow poll, painting your front door black can improve the value of your home by 2.9%.

Homeowners frequently get shivers up their spines, whether from drafty windows or the prospect of changing them. While replacing all the windows will surely increase the worth of your home, it does result in a significant expense, which may be less than ideal if you are selling the home soon.

However, you can replace specific windows, such as those on the lowest floor or the front-facing windows. Buyers prefer to know that new items are not just installed but can also save them money, and new energy-efficient windows can reduce heating and cooling bills.

Your kitchen and bathrooms may need to be updated if you live in an older home. While this can be costly, you will see a return on your investment when you sell your property. If remodeling the entire kitchen and bathrooms proves too costly, consider some little changes.

You can, for example, replace all the kitchen and bathroom hardware. It will not only quickly brighten up your home, but it is also quite inexpensive. You may also replace your flooring and add decorative components to bring in pops of color. As a result, even simple improvements to your home will help raise its market worth.

As a homeowner, making your home more energy efficient and eco-friendly can help you save money while increasing its value. In addition, these improvements, like many others, can be done without breaking the bank.

For example, switching to LEDs, compact fluorescent lightbulbs, or upgrading to energy-efficient appliances is one of the many ways to make your home energy-efficient and increase its value. You can also put household solar panels on your roof, smart thermostats, or low-flow showerheads in your bathroom. To select the most efficient appliances for your home, look for those with the Energy Star label.

The square footage of a home has a significant impact on its value. It can also significantly improve your personal home experience. If you already live in a smaller home, you can increase the value of your property and create additional space by adding on to the existing structure.

Larger properties frequently sell for a higher price. Consider adding a deck to the rear of your house, extra rooms above the garage, or a tiny guest house or office in your backyard to increase the value of your property.

Aside from extensions, increasing the usable space within your home’s current structure can significantly increase its value. For example, you can enhance the amount of usable square footage in your home by finishing your basement or tearing down non-load-bearing walls to create a more open-concept living space.

Before beginning any home renovation improvements, ensure your home is in the best shape. Cleaning your living area will significantly improve its appearance and storage capacity and resolve minor issues that may have been detracting from the value of your property, such as foul odors or mold growth.

It is important to declutter to boost the home’s appeal to potential buyers. If you want to sell quickly, get rid of all the clutter, box it up, and store it properly. If you intend to stay in your current house, you may want to consider installing a cabinet or closet to increase storage.

There is no doubt that the tips above will assist you in improving the market value of your home. Remember that you do not have to spend much money to improve and update your living spaces. However, every investment is equivalent to putting money in the bank. Your home is your savings account, and it is time to start planning for its future.

Comparing real estate metrics from one year to another can be challenging in a normal housing market. That’s due to possible variability in the market making the comparison less meaningful or accurate. Unpredictable events can have a significant impact on the circumstances and outcomes being compared.

Comparing this year’s numbers to the two ‘unicorn’ years we just experienced is almost worthless. By ‘unicorn,’ this is the less common definition of the word:

“Something that is greatly desired but difficult or impossible to find.”

The pandemic profoundly changed real estate over the last few years. The demand for a home of our own skyrocketed, and people needed a home office and big backyard.

It was a market that forever had been “greatly desired but difficult or impossible to find.” A ‘unicorn’ year.

Now, things are getting back to normal. The ‘unicorns’ have galloped off.

Comparing today’s market to those years makes no sense. Here are three examples:

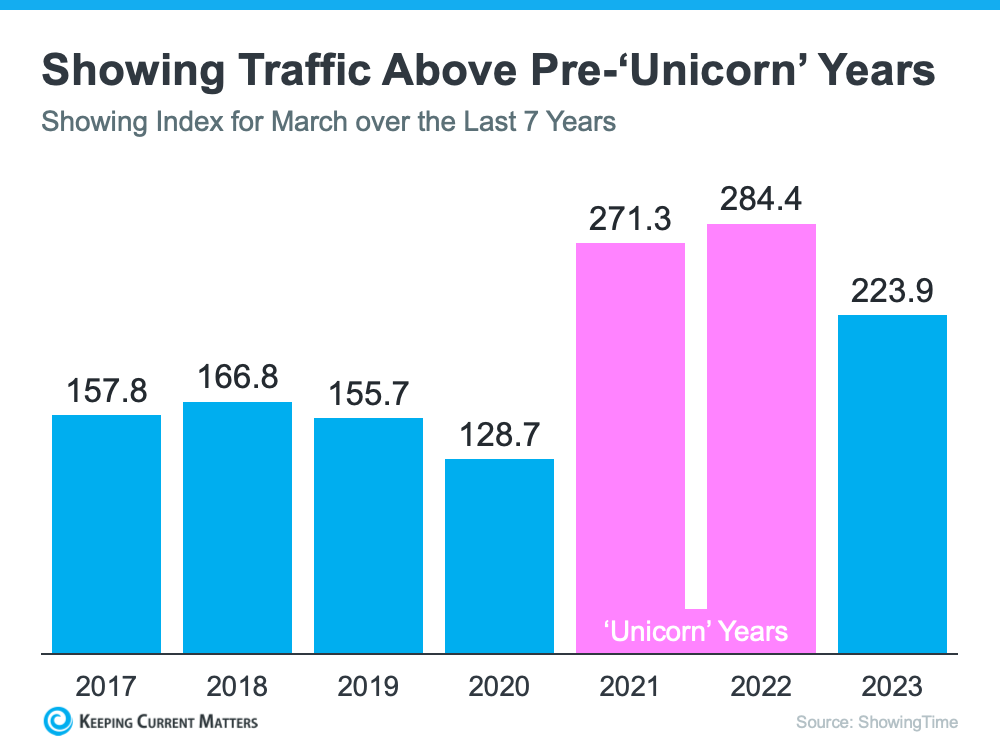

If you look at the headlines, you’d think there aren’t any buyers out there. We still sell over 10,000 houses a day in the United States. Of course, buyer demand is down from the two ‘unicorn’ years. But, according to ShowingTime, if we compare it to normal years (2017-2019), we can see that buyer activity is still strong (see graph below):

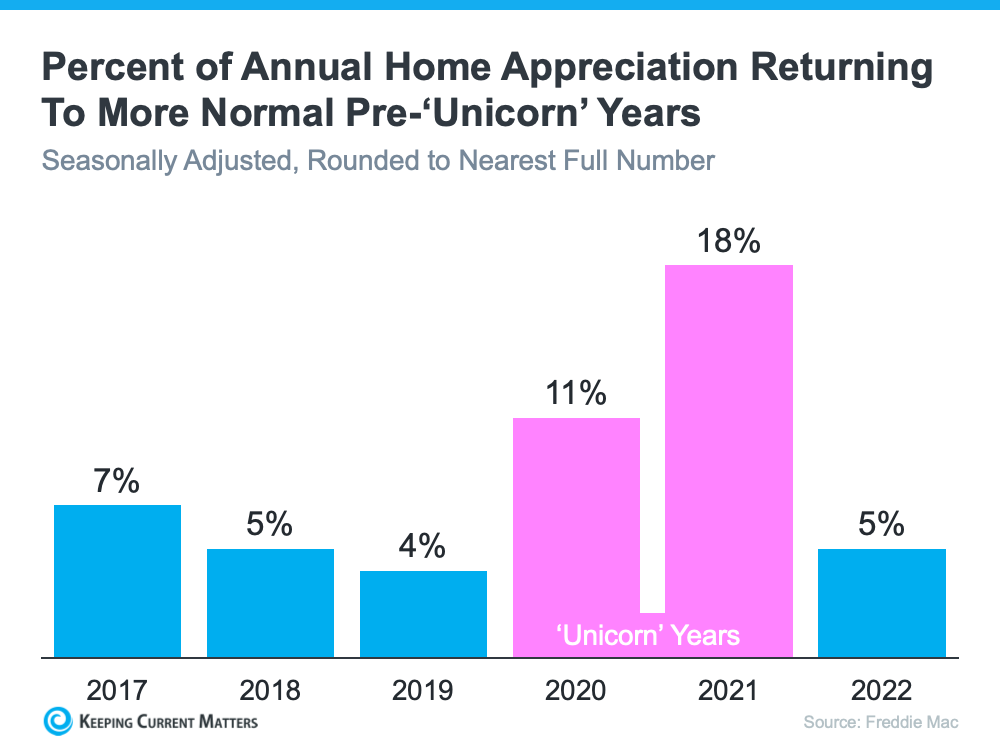

We can’t compare today’s home price increases to the last couple of years. According to Freddie Mac, 2020 and 2021 each had historic appreciation numbers. Here’s a graph also showing the more normal years (2017-2019):

We can see that we’re returning to more normal home value increases. There were several months of minimal depreciation in the second half of 2022. However, according to Fannie Mae, the market has returned to more normal appreciation in the first quarter of this year.

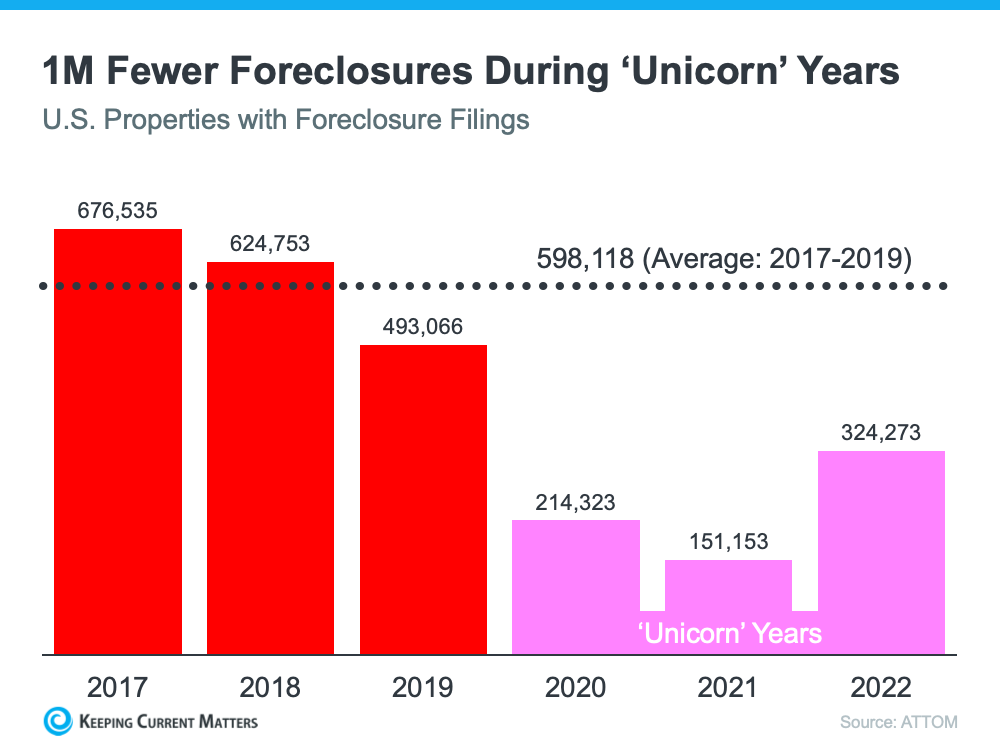

There have already been some startling headlines about the percentage increases in foreclosure filings. Of course, the percentages will be up. They are increases over historically low foreclosure rates. Here’s a graph with information from ATTOM, a property data provider:

There will be an increase over the numbers of the last three years now that the moratorium on foreclosures has ended. There are homeowners who lose their home to foreclosure every year, and it’s heartbreaking for those families. But, if we put the current numbers into perspective, we’ll realize that we’re actually going back to the normal filings from 2017-2019.

There will be very unsettling headlines around the housing market this year. Most will come from inappropriate comparisons to the ‘unicorn’ years. A real estate professional is a great resource to help you keep everything in proper perspective.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

The National Association of Realtors (NAR) will release its latest Existing Home Sales Report tomorrow. The information it contains on home prices may cause some confusion and could even generate some troubling headlines. This all stems from the fact that NAR will report the median sales price, while other home price indices report repeat sales prices. The vast majority of the repeat sales indices show prices are starting to appreciate again. But the median price reported on Thursday may tell a different story.

Here’s why using the median home price as a gauge of what’s happening with home values isn’t ideal right now. According to the Center for Real Estate Studies at Wichita State University:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less. While this is a good measure of the typical sale price, it is not very useful for measuring home price appreciation because it is affected by the ‘composition’ of homes that have sold.

For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

People buy homes based on their monthly mortgage payment, not the price of the house. When mortgage rates go up, they have to buy a less expensive home to keep the monthly expense affordable. More ‘less-expensive’ houses are selling right now, and that’s causing the median price to decline. But that doesn’t mean any single house lost value.

Even NAR, an organization that reports on median prices, acknowledges there are limitations to what this type of data can show you. NAR explains:

“Changes in the composition of sales can distort median price data.”

For clarification, here’s a simple explanation of median value:

The same thing applies to today’s real estate market.

Actual home values are going up in most markets. The median value reported tomorrow might tell a different story. For a more in-depth understanding of home price movements, reach out to a local real estate professional.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

The process of buying a home can feel a bit intimidating, even under normal circumstances. But today’s market is still anything but normal. There continues to be a very limited number of homes for sale, and that’s creating bidding wars and driving home prices back up as buyers compete over the available homes.

Navigating all of this can be daunting if you’re trying to do it alone. That’s why having a skilled expert to guide you through the homebuying process is essential, especially today. Bankrate shares this perspective:

“Advice and guidance from a professional real estate agent can be invaluable, particularly amid a hot or unpredictable housing market.”

All of these reasons combined may be why 86% of recent buyers used an agent according to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR). NAR also has this to say about why an agent is so essential today:

“A great real estate agent will guide you through the home search with an unbiased eye, helping you meet your buying objectives while staying within your budget. Agents are also a great source when you have questions about local amenities, utilities, zoning rules, contractors, and more.”

It starts with trust. You’ll want to know you can trust the advice they’re giving you, so you need to make sure you’re connected with a true professional. No one can provide perfect advice because it’s impossible to know exactly what’s going to happen at every turn – especially in today’s market. But a true professional can give you the best possible advice based on the information and situation at hand.

They’ll help advocate for you throughout the process and coach you on the essential knowledge you need to make confident decisions. That’s exactly what you want and deserve.

It’s critical to have an expert on your side who is skilled in navigating today’s housing market. If you’re planning to buy a home this year, connect with a real estate advisor who will give you the best advice and guide you along the way.

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.