Realty Executives Midwest

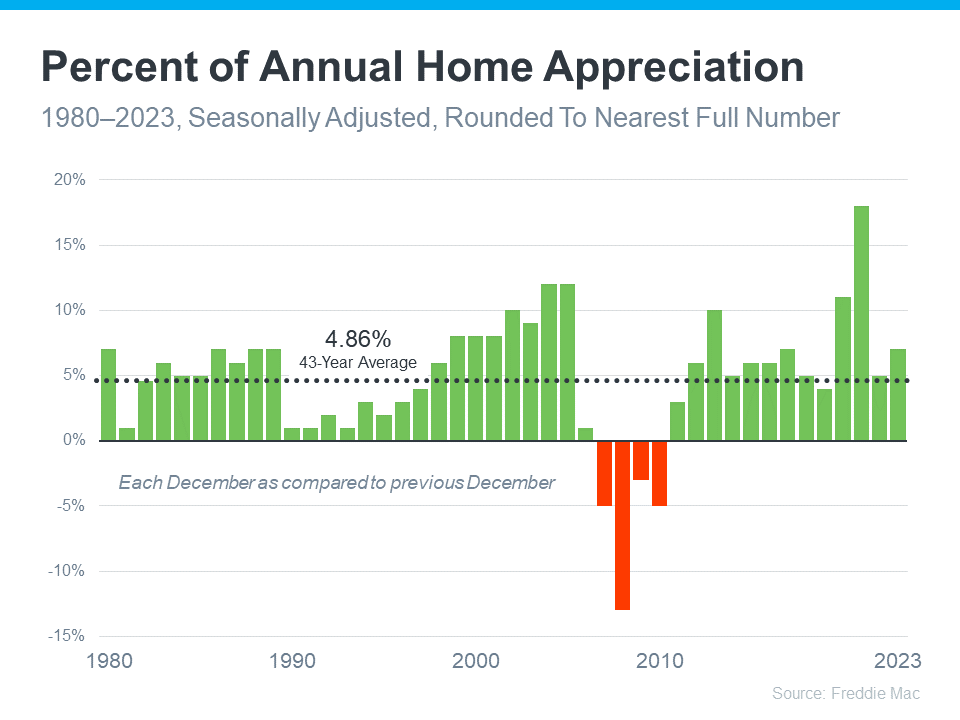

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash. Some in the media were even forecasting home prices would drop by as much as 10-20%—and that might have made you feel a bit unsure about buying a home.

But here’s what actually happened: home prices went up more than usual. Brian D. Luke, Head of Commodities at S&P Dow Jones Indices, explains:

“Looking back at the year, 2023 appears to have exceeded average annual home price gains over the past 35 years.”

To put last year’s growth into context, the graph below uses data from Freddie Mac on how home prices have changed each year going back to 1980. The dotted line shows the long-term average for appreciation:

As an article from Forbes says:

“. . . the U.S. real estate market has a long and reliable history of increasing in value over time.”

In fact, since 1980, the only time home prices dropped was during the housing market crash (shown in red in the graph above). Fortunately, the market today isn’t like it was in 2008. For starters, there aren’t enough available homes to meet buyer demand right now. On top of that, homeowners have a tremendous amount of equity, so they’re on much stronger footing than they were back then. That means there won’t be a wave of foreclosures that causes prices to fall.

The fact that home values went up every single year except those four in red is why owning a home can be one of the smartest moves you can make. When you’re a homeowner, you own something that typically becomes more valuable over time. And as your home’s value appreciates, your net worth grows.

So, if you’re financially stable and prepared for the costs and expenses of homeownership, buying a home might make a lot of sense for you.

Home prices almost always go up over time. That makes buying a home a smart move, if you’re ready and able. Connect with a local real estate agent to talk about your goals and what’s available in our area.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Are you thinking about making a move? If so, now may be the perfect time to start the process. That’s because experts say the best week to list your house is just around the corner.

A recent Realtor.com study looked at housing market trends over the past several years (with the exception of 2020, since it was an unusual year), and found the best week to put your house on the market this year is April 14-20:

“Every year, one week stands out from the rest as that perfect stretch of time when it’s great to be a home seller. This year, the week of April 14–20 is the best time to sell—that is, if sellers want to see lots of interest in their homes, sell quickly, and pocket some extra cash, according to Realtor.com® data.”

Here’s why this matters for you. While the spring market is a great time to sell no matter the week, this may be the peak sweet spot. And if you’ve been putting your plans on the back burner and waiting for the right time to act, this could be the nudge you need to make your move happen. As Hannah Jones, Senior Economic Research Analyst at Realtor.com explains:

“The third week of April brings the best combination of housing market factors for sellers. The best week offers higher buyer demand, lower competition [from other sellers], and fewer price reductions than the typical week of the year.”

But, if you want to get in on the action, you’ll need to move quickly and lean on the pros. Your local real estate agent is the perfect go-to when it comes to figuring out a plan to prep your house and get it on the market.

They’ll be able to offer advice to balance your target listing date with what you need to do from a repair and renovation standpoint. And they can walk you through exactly how to prioritize your list so you know what to tackle first.

For example, if your house is already in good shape, you’ll be able to really focus in on the smaller things that are easy to do and make a big impact. As an article from Investopedia says:

“You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”

Here are some specific examples from that article:

Just remember, even if you’re not ready to list within the next couple of weeks, that’s okay. The window of opportunity doesn’t close when this week ends. Spring is the peak homebuying season and it’s still a seller’s market, so you’ll be in the driver’s seat all season long.

Ready to get the ball rolling? Connect with a real estate agent to schedule a time to go over your next steps.

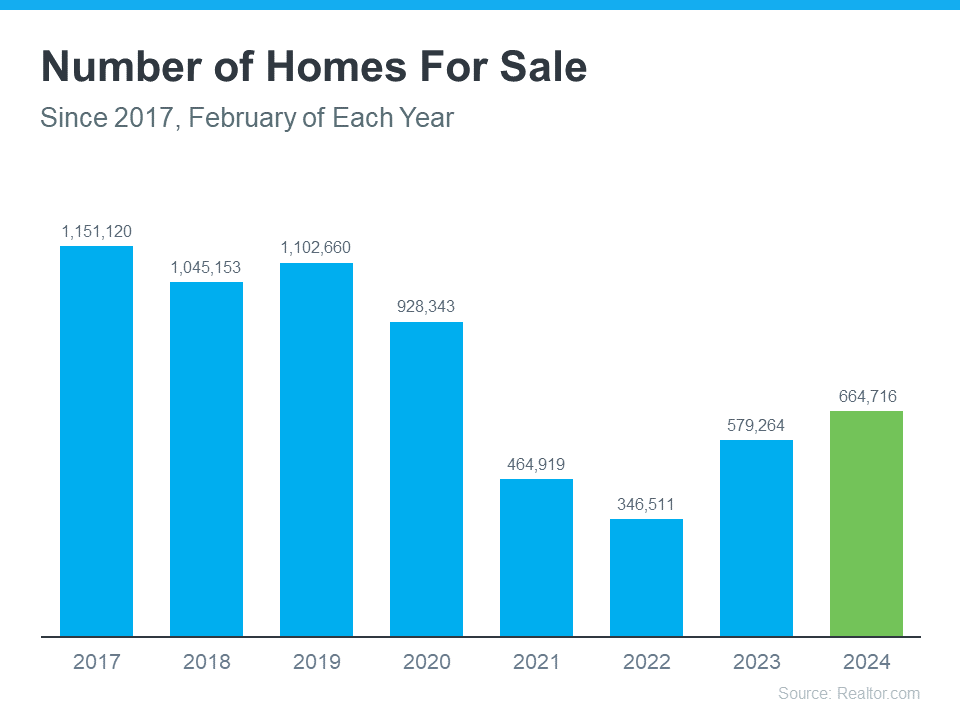

Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because the number of homes for sale is still low – and that’s leading to multiple-offer scenarios. And moving into the peak homebuying season this spring, this is only expected to ramp up more.

Remember these four tips to make your best offer.

Rely on a real estate agent who can support your goals. As PODS notes:

“Making an offer on a home without an agent is certainly possible, but having a pro by your side gives you a massive advantage in figuring out what to offer on a house.”

Agents are local market experts. They know what’s worked for other buyers in your area and what sellers may be looking for. That advice can be game changing when you’re deciding what offer to bring to the table.

Knowing your numbers is even more important right now. The best way to understand your budget is to work with a lender so you can get pre-approved for a home loan. Doing so helps you be more financially confident and shows sellers you’re serious. That gives you a competitive edge. As Investopedia says:

“. . . sellers have an advantage because of intense buyer demand and a limited number of homes for sale; they may be less likely to consider offers without pre-approval letters.”

It’s only natural to want the best deal you can get on a home, especially when affordability is tight. However, submitting an offer that’s too low does have some risks. You don’t want to make an offer that’ll be tossed out as soon as it’s received just to see if it sticks. As Realtor.com explains:

“. . . an offer price that’s significantly lower than the listing price, is often rejected by sellers who feel insulted . . . Most listing agents try to get their sellers to at least enter negotiations with buyers, to counteroffer with a number a little closer to the list price. However, if a seller is offended by a buyer or isn’t taking the buyer seriously, there’s not much you, or the real estate agent, can do.”

The expertise your agent brings to this part of the process will help you stay competitive and find a price that’s fair to you and the seller.

After you submit your offer, the seller may decide to counter it. When negotiating, it’s smart to understand what matters to the seller. Once you do, being as flexible as you can on things like moving dates or the condition of the house can make your offer more attractive.

Your real estate agent is your partner in navigating these details. Trust them to lead you through negotiations and help you figure out the best plan. As an article from the National Association of Realtors (NAR) explains:

“There are many factors up for discussion in any real estate transaction—from price to repairs to possession date. A real estate professional who’s representing you will look at the transaction from your perspective, helping you negotiate a purchase agreement that meets your needs . . .”

In today's competitive market, be sure to work with a local real estate agent to find you a home you love and craft a strong offer that stands out.

As the winter season comes to an end, many of us look forward to the fresh start that spring brings. It is the perfect time to declutter, organize, and deep clean our homes. Spring cleaning allows us to create a clean and refreshing environment, promoting a sense of well-being and productivity. In this article, we will look at some practical tips and tricks to organize your spring cleaning in a tidy and productive manner.

Before embarking on your spring cleaning, creating a checklist of to-do activities is important. This helps you stay organized and ensure you do not miss any areas needing attention. Start by going through each room in your home and note what needs to be cleaned, decluttered, or organized. Split your checklist into manageable sections, such as cleaning the kitchen, decluttering the bedroom, and organizing the garage. Having a clear plan will make your spring cleaning process much smoother.

One of the most important steps in spring cleaning is decluttering. Take the time to go through your belongings and decide what you want to keep, donate, or discard. Start with one area at a time, such as a closet or a drawer, and sort through each item. Ask yourself if you have used or worn the item in the past year. If not, it may be time to let it go. Decluttering creates more space in your home, helps create a sense of calm, and reduces visual clutter.

When cleaning each room, starting from the top and working your way down is best. Kick-start by dusting shelves, light fittings, and ceiling fans. Then, move on to cleaning windows, blinds, and curtains. Next, focus on wiping down surfaces such as countertops, tables, and cabinets. Finally, vacuum or mop the floors. When you clean from top to bottom, you ensure that any dust or dirt that drops while cleaning is captured and removed.

During your spring cleaning, do not forget to pay attention to the often-neglected areas of your home. These include baseboards, vents, and light switches. Use a mild cleaning solution or damp cloth to wipe down these areas and remove accumulated dust or grime. Also, remember to clean behind large appliances, such as the refrigerator and stove, to ensure that no dirt or debris lurks in these hidden spaces.

Spring is the perfect time to give your carpets and upholstery a deep clean. Thoroughly vacuum your carpets to get rid of any dust or debris. Consider hiring a professional cleaning service or renting a carpet cleaner for stains or high-traffic areas. Similarly, clean your upholstery using appropriate cleaning products or consider cleaning it professionally. You can revive their appearance and prolong their lifespan by giving your carpets and upholstery some extra attention.

Refreshing your linens and bedding is a great idea when doing spring cleaning. Wash your sheets, pillowcases, and duvet covers in hot water to remove any allergens or dust mites that may have accumulated over time. To keep your mattress clean and prolong its life, consider rotating it and using a mattress protector. Do not forget to wash or dry clean your curtains and give your pillows a good fluff in the dryer to restore their shape.

Take the time to organize and declutter your storage spaces, such as closets, cabinets, and drawers. Remove everything from the area and sort through each item. Donate or discard items that you no longer use or need. Invest in storage solutions such as drawer organizers, boxes, or baskets to keep things accessible and tidy. To make locating stuff in the future simpler, label the storage containers you use. Over time, having a well-organized storage system will save you time and lessen your stress.

Spring cleaning is not just about the interior of your home; it is also a great time to clean and maintain your outdoor spaces. Sweep away any debris from your patio or deck, and wash the surfaces using a pressure washer if necessary. Clean your outdoor furniture and cushions, and check for any repairs or replacements that may be needed. Also, take the time to inspect and clean your gutters and downspouts to ensure proper drainage. When you pay attention to your outdoor spaces, you create a welcoming environment for outdoor activities during the spring and summer months.

Spring cleaning is a great time to give your house a makeover and make it a tidy, orderly place to live. These tips and tricks can make your spring cleaning process efficient and effective. Remember to create a checklist, declutter first, clean from top to bottom, and pay attention to neglected areas. Keep in mind to deep clean carpets and upholstery, refresh your bedding and linens, and organize storage spaces. Last, take the time to clean and maintain outdoor spaces for a complete spring cleaning experience. With these strategies, you can enjoy a fresh and revitalized home as you embrace the new season. Happy spring cleaning!

If you’re taking a look at your expenses as you retire, saving money where you can has a lot of appeal.

One long-standing, popular way to do that is by downsizing to a smaller home.

When you think about cutting down on your spending, odds are you think of frequent purchases, like groceries and other goods. But when you downsize your house, you often end up downsizing the bills that come with it, like your mortgage payment, energy costs, and maintenance requirements. Realtor.com shares:

“A smaller home typically means lower bills and less upkeep. Then there’s the potential windfall that comes from selling your larger home and buying something smaller.”

That windfall is thanks to your home equity. If you’ve been in your house for a while, odds are you’ve built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Daniel Hunt, CFA at Morgan Stanley, explains:

“Home equity can be a significant source of wealth for retirees, often representing a large portion of their net worth. . . . Retirement planning can be complex, but your home equity shouldn’t be overlooked.”

And when you’re ready to use that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

If you’re thinking about downsizing, ask yourself these questions:

Then, meet with a real estate agent to get an answer to this one: What are my options in the market right now? A local real estate agent can walk you through how much equity you have in your house and how it positions you to win when you downsize.

Want to save money in retirement? Consider downsizing – it could really help you out. When you’re ready, connect with a local real estate agent about your goals in the housing market this year.

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.