Realty Executives Midwest

As the days grow longer and the temperature rises, it is time to dust off your gardening gloves and get ready to transform your outdoor space into a vibrant oasis. Whether you are a seasoned gardener or just starting, these gardening tips for warm weather will help you cultivate a lush and thriving garden that will be the envy of your neighborhood. From planting and watering to pest control and maintenance, we have you covered with everything you need to know to achieve gardening success this summer.

Before you start digging in the dirt, it is essential to choose plants that thrive in warm weather conditions. Here are some popular warm-weather plants to consider for your garden:

Before you start planting, take some time to plan your garden layout to maximize space and sunlight. Consider factors such as:

Proper watering is essential for the health and vitality of your plants, especially during the warm summer months. Here are some watering tips to keep your garden thriving:

Keeping pests and diseases at bay is essential for maintaining a healthy garden. Here are some natural pest control methods to try:

Regular maintenance is vital to keeping your garden looking its best throughout the summer. Here are some tasks to add to your gardening checklist:

With these gardening tips for warm weather in your toolkit, you are well-equipped to cultivate a thriving garden that will be the envy of your neighborhood this summer. From choosing the right plants and planning your garden layout to providing adequate water and practicing pest control, taking proactive steps will ensure a bountiful harvest and beautiful blooms all season long. So, grab your gardening tools, roll up your sleeves, and get ready to enjoy the joys of gardening in the warm summer sun.

In the wake of the National Association of Realtors’ (NAR) landmark $418 million settlement, a seismic shift is underway in the real estate industry, particularly in how agent commissions are handled. The changes, though seemingly straightforward, have profound implications that will fundamentally alter the landscape of buying and selling homes in America.

The heart of the matter is regarding the removal of commission rates from the MLS (multiple listing service), a change that might initially appear as a stride toward transparency and fairness. However, a closer examination reveals a potentially murky future, where the dynamics of real estate transactions become less transparent to the very individuals they are meant to serve: buyers and sellers.

Historically, the MLS has been the bedrock of real estate commissions, offering a level playing field for all parties involved. It ensured transparency in commission agreements, providing buyer’s agents with clear expectations of compensation prior to engaging in transaction discussions.

The settlement’s requirement to eliminate such disclosures threatens to upend this balance, ushering in an era where commission negotiations precede, and potentially influence, the discussions of a home’s purchase terms.

Commissions move behind closed doors

Consider a scenario where a buyer’s agent, prior to even scheduling a showing, inquires about the commission a listing agent is willing to offer. This conversation — occurring away from the eyes and ears of buyers and sellers — sets the stage for a transaction where the agent’s compensation could take precedence over the buyer’s best interest.

In the worst kind of scenario, there’s a risk that a buyer’s agent might not be completely honest with their customer. For example, before starting negotiations for a purchase, they might quietly sort out what they need to do to secure a certain commission rate with the seller’s agent.

Even more concerning, they might mislead the buyer about the commission being paid by the seller and factor this incorrect commission into the negotiation process. Essentially, the problem here is that agents could end up negotiating their commissions without their customer’s knowledge or approval, which isn’t how it should be. Agents’ compensation discussions should be transparent to buyers and sellers.

The end of buyer agent incentives

One aspect of the settlement that stands out involves limitations on how much a Realtor can be compensated, specifically stating that they cannot accept compensation that exceeds the agreed-upon amount with the buyer.

For instance, if a seller offers an additional 1 percent beyond the buyer and buyer’s agent’s agreement, the agent is barred from accepting it, even if this doesn’t affect the purchase price — potentially leaving more money with the seller.

Essentially, all buyer agent incentives offered by a seller are now gone. The unfortunate recourse for this is to increase the commission required by the buyer to ensure that as much of seller-paid commission is captured as possible. The most likely scenario seems to be that this rule will be often ignored by the industry and that buyer’s agents will be accepting higher commissions due to a lack of checks and balances.

While some sellers might welcome the idea of not offering buyer agent incentives, it could be viewed as anti-competitive by other sellers, as it prevents them from using incentives to attract buyer agents, a tactic often used by builders and investors.

Agents may also feel this rule is anti-competitive because it puts a cap on how much commission they can make in a transaction by automatically undercutting the commission being offered to them by agreeing parties. Buyers may feel similarly, that they are being held fully responsible for their agent’s commissions even when the seller is willing to pay it.

This part of the settlement in particular prohibits free market activities and aggressively restricts the ability for the sellers, buyers and agents to negotiate terms they believe are in their best interest.

A potential for miscommunication on commissions

Moreover, the settlement strips away the guarantees of commission compensation through the MLS, opening the door for potential misunderstandings or miscommunications about commissions.

Such disputes between brokers, previously resolved through binding arbitrations through the local Realtor associations, will essentially cease to exist. In a scenario where it falls on buyers to directly cover their agents’ commissions, we might see a shift toward legal tangles between buyers and brokerages.

Buyers could even be liable for two or more commissions on the same transaction because they didn’t understand the terms and conditions they signed with previous agents.

This could spell trouble for the industry’s reputation. Imagine a situation where real estate agents need to take legal action to secure their earnings, potentially leading to liens on a buyer’s newly purchased home or lawsuits for unpaid commissions. Actions like these could dramatically alter the public’s perception of Realtors.

A significant and concerning aspect of this new era is the absence of recorded commissions, which means that agents and consumers will lack a true understanding of the range of commissions being charged in the market.

According to NAR’s Profile of Home Buyers and Sellers, 71 percent of buyers only interviewed one agent. Although you would hope this trend would change given the terms of the settlement, the same report states that 81 percent of recent sellers contacted only one agent before listing their home.

The unfortunate truth is that consumers are not interviewing multiple agents to ensure they are receiving the best service at the best price. If buyers and sellers are entrusting the first agent they meet, they won’t have access to readily available information to know if they are being charged a fair commission.

It’s important to acknowledge that most real estate agents operate with integrity and professionalism. However, like any industry, there are bad actors who may exploit these new rules for personal gain, especially in a landscape where their source of income has been significantly diminished because of this settlement.

The lack of transparent commission structures opens the door to unethical actions, making it crucial for regulatory bodies and industry associations to remain vigilant and for consumers to be well-informed.

Despite the concerns surrounding the new commission structure, there’s a silver lining. If it goes in the right direction, this shift could drive a much-needed increase in open communication and ethical practices within the real estate industry.

For agents willing to navigate these changes with integrity, there’s a significant opportunity to stand out and thrive. The future of real estate may look different, but it also holds the possibility of being more consumer-friendly and professional.

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros.

They coach people through market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you.

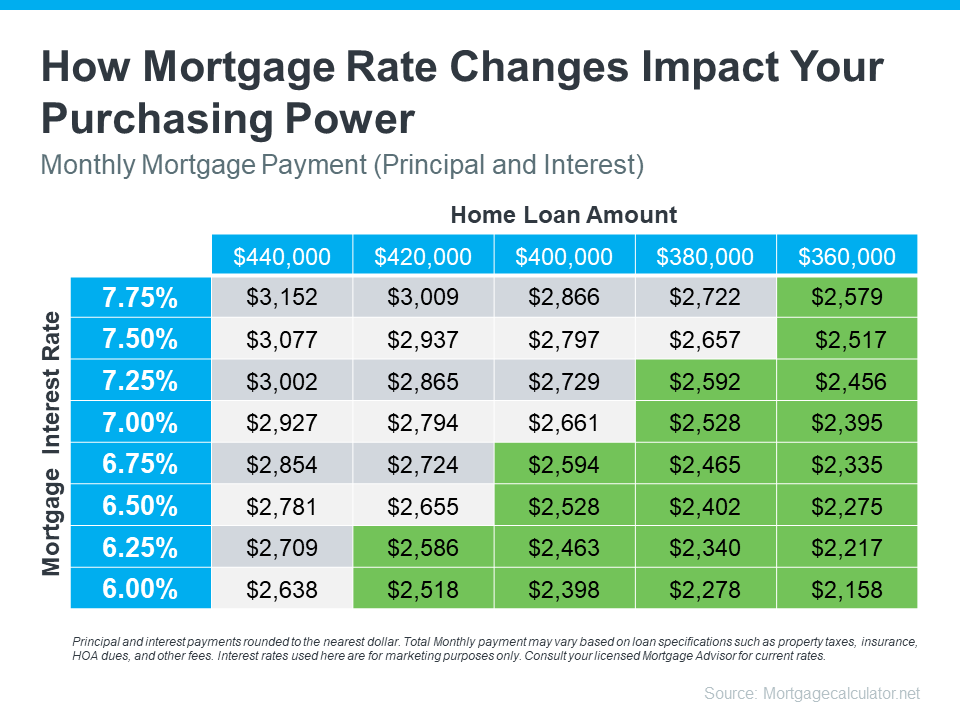

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them.

You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side.

Have questions about what’s going on in the housing market? Connect with a real estate professional to take what’s happening right now and figure out what it really means for you.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Who does not love lounging by the pool or hosting a barbecue on the patio during warm summer days? Your outdoor spaces are an extension of your home, and with a bit of creativity and effort, you can turn them into inviting retreats that you will love spending time in. Whether you are looking to spruce up your patio for personal enjoyment or to impress potential buyers, we have you covered with these easy and affordable ways to decorate and dress up your patio and pool areas.

Start by selecting the right furniture to anchor your outdoor living area. Opt for weather-resistant materials like rattan, aluminum, or teak. A comfortable sofa, chairs, and coffee table can create a cozy seating area for relaxing with friends and family.

Inject some personality into your outdoor space with vibrant cushions and throws. Choose colors and patterns that complement your patio furniture and reflect your style. Cushions and throws add comfort and make your outdoor seating area feel warm and inviting.

Set the mood in your outdoor oasis with strategic lighting. Hang string lights above your patio or pool area at night to create a magical ambiance. You can also use lanterns, candles, or solar-powered stake lights to add a soft glow and enhance the atmosphere.

Lay down outdoor rugs to define different zones within your outdoor space. Rugs add warmth and texture and help anchor your furniture arrangement. Opt for durable, weather-resistant rugs that can withstand exposure to sunlight and rain.

Bring life to your patio and pool areas with potted plants and greenery. Choose various plants in different sizes and textures to create visual interest. Place potted plants strategically around your outdoor space to soften hard surfaces and add a touch of nature. Keep ample distance from the pool to avoid shedding leaves and other debris from falling into the water.

Protect yourself from the sun’s harsh rays by incorporating shade solutions like umbrellas or awnings. Position umbrellas over seating areas or lounge chairs to provide relief from direct sunlight. Retractable awnings are another stylish option that offers adjustable shade whenever needed.

Install screens or trellises to create a sense of privacy and intimacy in your outdoor oasis. These decorative elements add visual interest and serve as a backdrop for climbing vines or hanging plants. Choose screens or trellises that complement your outdoor decor and provide the desired level of privacy.

Take your pool area to the next level with fun and functional accessories. Invest in pool floats, inflatable loungers, and water toys to enhance your poolside experience. Remember to provide ample seating and shade for spectators and guests who prefer to lounge by the pool.

Add a fire pit or outdoor fireplace to extend the use of your outdoor space into the cooler months. Gather around the fire with friends and family to roast marshmallows, sip hot cocoa, and enjoy cozy evenings outdoors. A fire feature adds warmth, ambiance, and a focal point to your patio or pool area.

Finally, finish your outdoor oasis with decorative accents that reflect your personality and style. Hang artwork or mirrors on exterior walls to add visual interest. Incorporate decorative elements like throw pillows, lanterns, and outdoor sculptures to infuse your space with character.

Implementing these easy and affordable decorating ideas can transform your patio and pool areas into inviting retreats where you will love spending time. Whether you are hosting a summer soiree or simply unwinding after a long day, your outdoor oasis will be the envy of the neighborhood. So, unleash your creativity and make the most of your outdoor living space.

Source: Realty Executives

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

You may have heard headlines in the news lately about agents in the real estate industry and discussions about their commissions. And if you’re following along, it can be pretty confusing. But here’s the thing you really need to know – expert advice from a trusted real estate agent is priceless, now more than ever. And here’s why.

A real estate agent does a lot more than you may realize.

Your agent is the person who will guide you through every step when buying a home and look out for your best interests along the way. They smooth out a complex process and take away the bulk of the stress of what’s likely your largest purchase ever. And that’s exactly what you want and deserve.

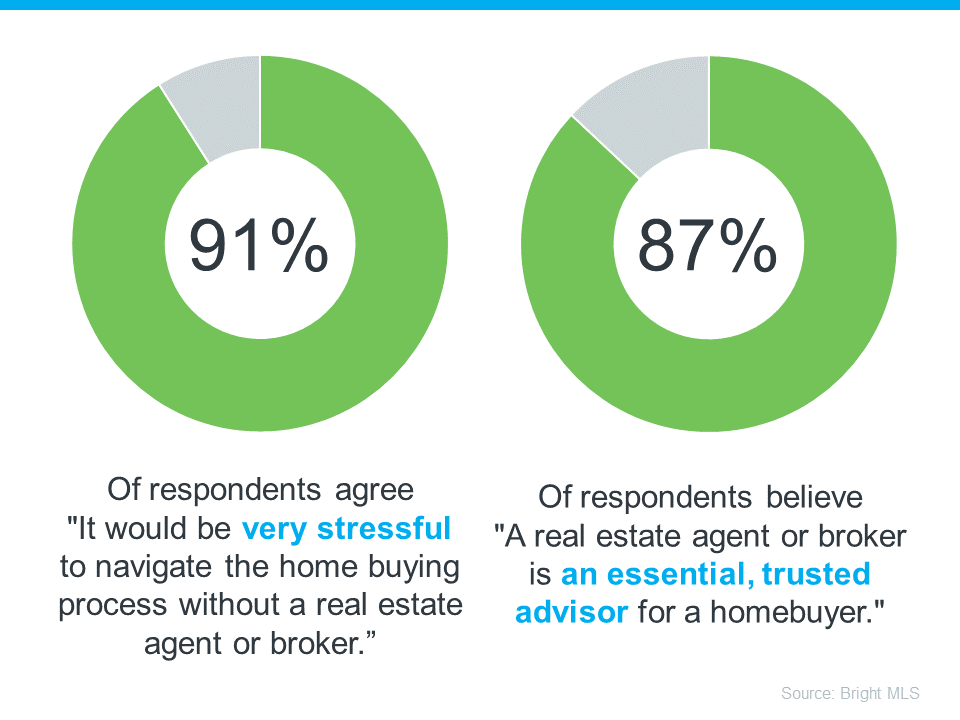

This is at least a part of the reason why a recent survey from Bright MLS found an overwhelming majority of people agree an agent is a key part of the homebuying process (see visual below):

To give you a better idea of just a few of the top ways agents add value, check out this list.

The right agent – the professional – will coach you through everything from start to finish. With professional training and expertise, agents know the ins and outs of the buying process. And in today’s complex market, the way real estate transactions are executed is constantly changing, so having the best advice on your side is essential.

In a world that’s powered by data, a great agent can clarify what it all means, separate fact from fiction, and help you understand how current market trends apply to your unique search. From how quickly homes are selling to the latest listings you don’t want to miss, they can explain what’s happening in your specific local market so you can make a confident decision.

Agents help you understand the latest pricing trends in your area. What’s a home valued at in your market? What should you think about when you’re making an offer? Is this a house that might have issues you can’t see on the surface? No one wants to overpay, so having an expert who really gets true market value for individual neighborhoods is priceless. An offer that’s both fair and competitive in today’s housing market is essential, and a local expert knows how to help you hit the mark.

In a fast-moving and heavily regulated process, agents help you make sense of the necessary disclosures and documents, so you know what you’re signing. Having a professional that’s trained to explain the details could make or break your transaction, and is certainly something you don’t want to try to figure out on your own.

From offer to counteroffer and inspection to closing, there are a lot of stakeholders involved in a real estate transaction. Having someone on your side who knows you and the process makes a world of difference. An agent will advocate for you as they work with each party. It’s a big deal, and you need a partner at every turn to land the best possible outcome.

Real estate agents are specialists, educators, and negotiators. They adjust to market changes and keep you informed. And keep in mind, every time you make a big decision in your life, especially a financial one, you need an expert on your side.

Expert advice from a trusted professional is priceless. Connect with a local real estate agent today.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.