Realty Executives Midwest

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

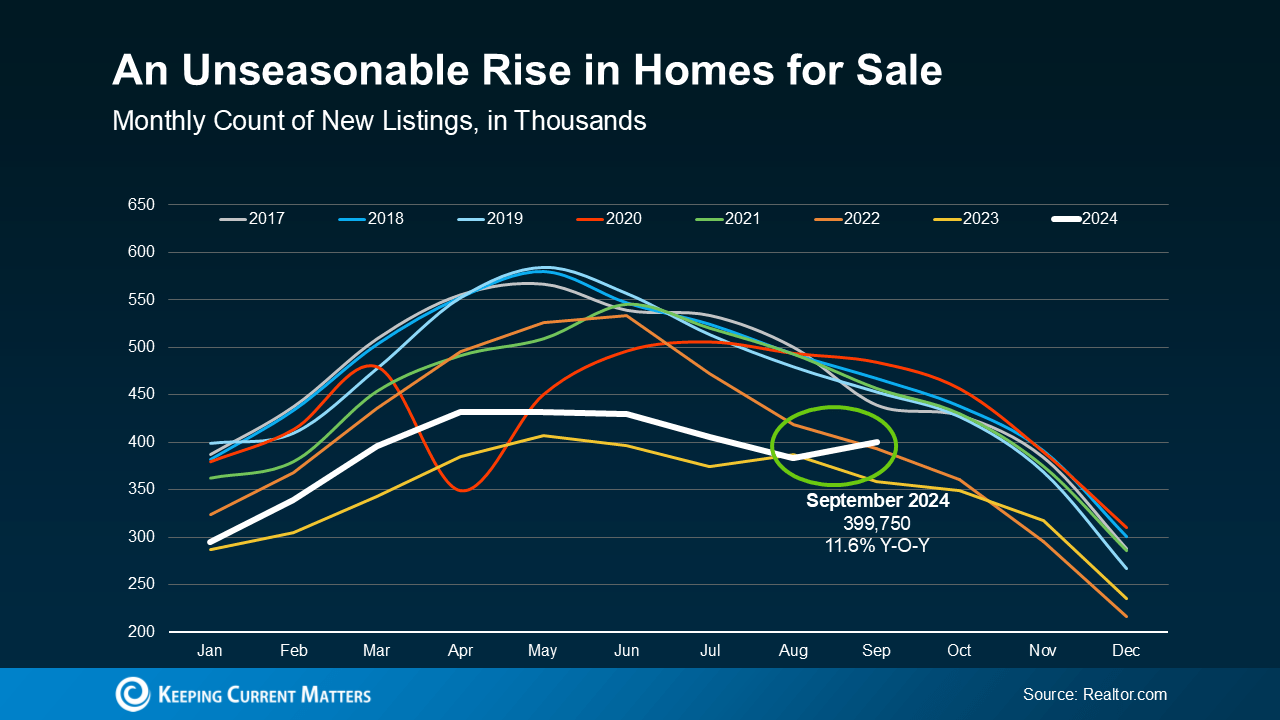

Homeowners typically slow down their moving plans as the summer months wrap up, and as a result, fewer homes are listed for sale in the fall. It’s a predictable, seasonal trend in real estate. But this year, mortgage rates came down at the same time the number of homes on the market usually starts to decline. So, what happened? More homeowners decided to sell, so more homes came to the market.

The most recent data from Realtor.com reveals that in September, the number of homes put up for sale increased by 11.6% compared to this time last year.

As the green circle in the graph below shows, the typical September decline in homes coming to the market didn’t happen – that number actually went up (see graph below):

Ralph McLaughlin, Senior Economist at Realtor.com, explains why there was an unseasonable rise:

Ralph McLaughlin, Senior Economist at Realtor.com, explains why there was an unseasonable rise:

“This sharp increase is largely due to the decline in mortgage rates in mid-August, enticing homeowners to sell.”

So, as rates came down at the end of the summer, more people jumped into the market and decided to make their move.

It means more fresh options to choose from than you’ve had in a while – not the ones that have been sitting around, unsold.

But keep in mind, mortgage rates have been volatile lately, ticking up slightly in recent weeks, which could limit the number of people who feel comfortable with the idea of selling in the months ahead. And in this market, it’s mortgage rates that are largely driving homeowner decisions.

Whether you’re looking for a starter home, an upgrade, or hoping to downsize, you have more homes to choose from right now. And if you can find what you’re looking for, know that these new, fresh options won’t be on the market forever. So, staying on top of what’s available in your local area with a trusted agent is key.

And remember, one month doesn’t make a trend. So, what does that mean going forward? Whether more homeowners than normal continue to put their houses on the market will largely depend on what happens with mortgage rates and the economic factors that impact them, like inflation, employment, and the reactions by the Federal Reserve.

With that in mind, now might be your moment, while more homes are available – if you’re ready, willing, and able to buy this fall.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“The rise in inventory – and, more technically, the accompanying months’ supply – implies home buyers are in a much-improved position to find the right home and at more favorable prices.”

As rates came down at the end of the summer, sellers started to trickle back into the market, which means buyers have more choices right now. And working with a trusted local real estate agent is the best way to take advantage of your new options before they’re all scooped up.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

As the cooler months of fall and winter settle in, nothing beats the comforting taste of pumpkin-based dishes. Pumpkins are versatile and can be used in both savory meals and sweet treats, making them the perfect ingredient for warm, cozy recipes. Here are seven of the best meal ideas with pumpkin to try during the cold months to fill your home with delicious aromas and satisfy your cravings.

A bowl of pumpkin soup is the ultimate comfort food for chilly evenings. This creamy and flavorful dish is made using pumpkin, onion, garlic, vegetable broth, and a touch of cream. The secret to a delicious pumpkin soup lies in the spices, with a pinch of nutmeg or cinnamon adding the warmth and sweetness that pairs so well with the natural pumpkin flavor. Serve it with a side of crusty bread for a perfect meal.

An added benefit of this meal idea with pumpkin is the ability to make it in advance or in large batches. Freeze what you do not use for another meal!

Soft and full of seasonal spices, pumpkin bread is a favorite during fall and winter. It is a moist, spiced bread made with pumpkin puree, flour, eggs, and warm spices like cinnamon and cloves. Whether you enjoy it plain, with a smear of butter, or topped with nuts, pumpkin bread makes a wonderful snack or breakfast treat.

To make it healthier, you can use whole wheat flour or add raisins and seeds to pack in more nutrients. This bread also freezes well, making it convenient for quick, warm treats.

No fall or winter gathering is complete without the traditional pumpkin pie. This classic dessert features a smooth pumpkin filling made with pumpkin puree, eggs, sugar, and warm spices baked into a buttery crust. Regardless of the holiday or celebration, pumpkin pie is a timeless favorite. It is typically topped with a generous dollop of whipped cream, making each bite a perfect balance of creamy and sweet.

This is an easy dessert to find in the store, so if you want to skip the baking and head straight to enjoying pie, this is a great option to add to your shopping list!

Start your day with a warm, hearty breakfast of pumpkin pancakes. These fluffy pancakes are packed with pumpkin puree and spices like cinnamon and nutmeg, giving them the unmistakable flavors of fall. You can easily prepare them just like regular pancakes, but with a seasonal twist. Pair them with syrup, butter, or even a sprinkling of cinnamon sugar for an extra touch of sweetness.

For a savory and filling meal idea with pumpkin, pumpkin risotto is a must-try. This dish is made by cooking arborio rice with vegetable broth, pumpkin puree, and a splash of white wine. The creamy texture of the risotto combined with the subtle sweetness of the pumpkin makes for a satisfying meal that is both flavorful and elegant. It is the perfect dish for cozy dinners and can be topped with Parmesan cheese for extra richness. Think about adding additional vegetables to make your risotto unique!

Looking for a hearty and savory dish with a twist? Try pumpkin chili. The pumpkin adds a slight sweetness that balances out the spicy flavors of traditional chili. Combine ground beef or turkey with kidney beans, tomatoes, chili powder, cumin, and pumpkin puree for a unique and comforting meal. Pumpkin chili is a filling dish that is perfect for warming up on a frosty night and goes wonderfully with cornbread.

After carving your pumpkins, do not let the seeds go to waste! Roasted pumpkin seeds are a crunchy and nutritious snack that is easy to make. Simply rinse the seeds, dry them, toss with olive oil and seasonings, and roast in the oven until crispy. These seeds are great for snacking on their own or sprinkling over salads for added crunch. You can experiment with flavors, using savory seasonings like garlic powder and salt or sweet options like cinnamon and sugar.

Pumpkins are an incredibly versatile ingredient, allowing you to create both sweet and savory dishes that are perfect for the fall and winter seasons. From the creamy comfort of soup to the classic delight of pie, these meal ideas with pumpkin will help keep you warm and satisfied when the weather turns cold. Whether you are making a cozy meal for yourself or serving guests, these pumpkin recipes are sure to bring warmth to your table.

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

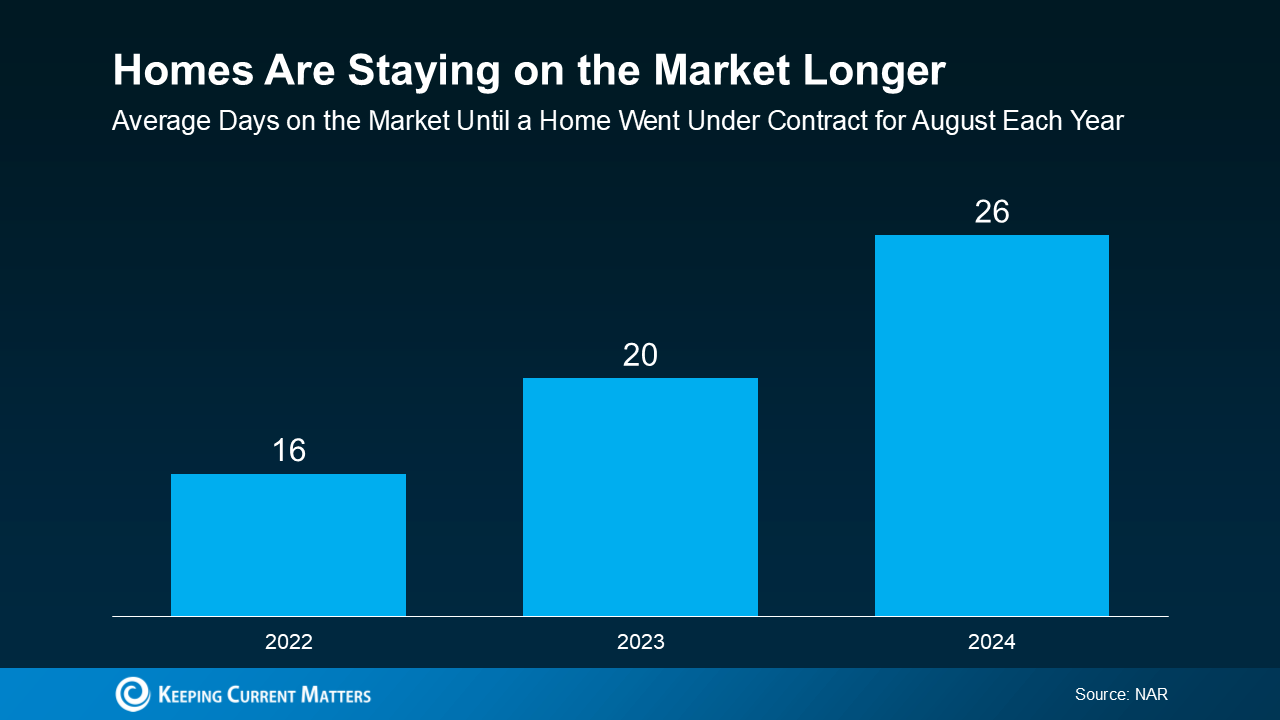

Seeing your house sit on the market without any bites is the ultimate frustration. And unfortunately, some sellers are in that tricky spot today.

According to data from the National Association of Realtors (NAR), the average time a house spends on the market has increased over the past few years (see graph below):

A recent post from Realtor.com notes a similar trend:

A recent post from Realtor.com notes a similar trend:

“During the week ending Sept. 14, homes stayed on the market eight days longer compared to last year. With more choices available and mortgage rates expected to fall, buyers are taking their time, which means sellers will need to be patient and flexible.”

Some of that is because inventory has gone up, so buyers have more options. And higher mortgage rates have definitely slowed demand over the past two years, and that’s out of your control. But here’s the secret. There’s something you can control – it’s also where those other sellers missed the mark. They didn’t work with the right agent.

Make no mistake, with the right strategy and agent partner, your house can still sell quickly, even today.

If time matters to you, you need to partner with an agent who understands this shifting market. That agent will be your go-to resource on what buyers are looking for right now, and how to position your home to hit the mark.

Here are just a few tips a great real estate agent will walk you through. They may seem simple, but advice like this can make all the difference.

1. Competitive Pricing: One of the most critical factors in selling your home quickly is setting the right price. A local real estate agent will do a competitive market analysis by reviewing recent sales and current listings for your area. Then, they’ll use that data to make sure your home is priced accurately for today’s market. This strategic pricing approach is the best way to make sure you’re hitting the sweet spot on price. If you don’t lean on an agent for this, it can really slow your process down. As U.S. News says:

“. . . setting an unrealistically high price with the idea that you can come down later doesn’t work in real estate . . . A home that’s overpriced in the beginning tends to stay on the market longer, even after the price is cut, because buyers think there must be something wrong with it.”

2. The Home’s Condition: Homes that are well maintained, have great curb appeal, and are updated with modern finishes tend to sell faster. So, if speed is a priority, make sure your house makes a great first impression. An agent is a key resource on what buyers will be looking for, if staging is worthwhile, and what repairs you need to tackle before you list. Ramsey Solutions offers this advice:

“In the spirit of selling your home fast, take care of things now that will be a problem in the closing process. Talk to your agent about fixes you’ll need to make to pass the home inspection, like: plumbing problems, roof damage, electrical issues, HVAC glitches. . . These are issues you’ll be expected to take care of before any buyers close on your house—you might as well get ahead of the game to help your home sell faster.”

3. Incentives and Extras: If you want to stand out from those other homes on the market, offering incentives or concessions, like help with closing costs, a home warranty, or including additional items (like appliances or furniture) with the sale can sweeten the deal for buyers. A real estate agent can suggest the right incentives to offer based on current market conditions and buyer expectations, so you can close the sale even faster.

Selling a home quickly in a shifting market requires a strategic approach and an in-depth understanding of what buyers want. That’s why partnering with a local real estate agent is so important. As Forbes says:

“When time is of the essence, you can’t afford to take a chance on an inexperienced housing professional. Instead, you’ll want to work with a real estate agent who knows your market and has helped sellers in your situation before.”

Source: Keeping Current Matters

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.

Stock up on winter supplies. If you live in a region with cold, snowy winters, fall is the time to prepare.

- Check the condition of snow shovels and ice scrapers; replace as needed.

- Pick up a bag of pet- and plant-safe ice melt, if needed.

- Restock emergency kits for car and home.

- If you use a snow blower, have it serviced and purchase fuel.

Shut off exterior faucets and store hoses. Protect your pipes from freezing temperatures by shutting off water to exterior faucets before the weather dips below freezing. Drain hoses and store them indoors. Drain and winterize irrigation system, if using.Find a landscape contractor on Houzz