(Published on - 4/14/2026 3:28:46 PM)

Wondering If You Should Still Buy a Home Right Now? Here’s What To Keep in Mind.

With economic headlines, global events, and near constant talk about affordability, you may be wondering if this is the right time to move. But here’s what you need to remember.

While recent events do have some impact on the housing market, they don’t take buying off the table. You just have to use a different strategy.

Mortgage Rates Have Been Up Slightly – Here's Why

After trending down for most of 2025, mortgage rates have been higher again for over roughly a month now. And experts say it’s a result of what's happening overseas and in the broader economy. As Mark Fleming, Chief Economist at First American, explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

But what does that really mean for you? Should you wait for everything to settle back down before you buy a home?

The short answer is no. You don’t have to wait.

Your Window To Buy Didn’t Close

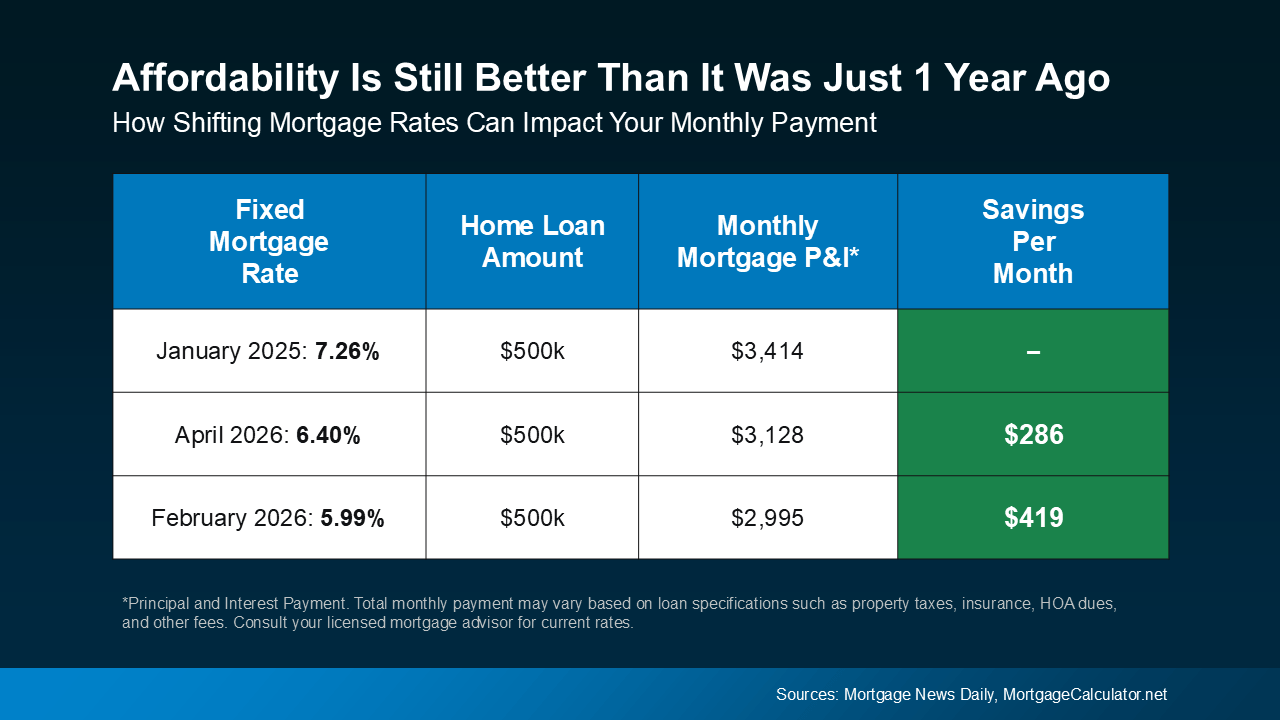

It’s true that a month or so ago, when rates were just shy of 6%, buying felt a bit more affordable. And now that rates are hovering around the mid-6s, monthly payment costs are higher.

But zoom out for a second.

Let’s say you’re taking out a loan for $500k. Even with rates in the mid 6s, you’re still saving roughly $300 on your monthly payment compared to buyers who made their purchase early last year.

That means this recent increase in rates hasn’t erased the progress we’ve seen. Buying is still more affordable than it was just one year ago (see below):

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

The goal moving forward shouldn’t be to perfectly time the market. Things change too quickly for that. Instead, the real goal is to make the best decision you can based on where things are today. And the best advice anyone can give is: brace for volatility.

When It Comes To Rates, Expect the Unexpected

Mortgage rates are going to continue to be move around in the weeks or months ahead as new information and economic reports come out.

Try to remember, you can’t control global events or where rates go next week (or even next month). But you can control how you prepare. If you do that, it becomes less about the headlines, and more about your situation.

If You Want or Need To Move, You Still Can

The simple truth is, if you want or need to move, you still can.

Some buyers are choosing to move forward right now because their needs haven’t changed. A growing family, a job relocation, a lifestyle shift – those things still matter.

And for buyers who do decide to move forward, there are ways to make it work.

For example, you could explore options like adjustable-rate mortgages (ARMs) to get a lower rate upfront. That may or may not be the right fit for you, but it highlights an important point: there are strategies that can help you move, even now.

What matters most is having a plan.

And working with the right agent and lender is a big part of that. With expert help, you’ll:

-

Understand your budget and what the math looks like at today's rates.

-

Explore your financing options, including ARMs and assistance programs.

-

Have trusted guidance from experts who'll keep you up to date throughout the process.

Bottom Line

Even though there’s some uncertainty, that doesn’t mean you’re out of options.

If you need to move, you still can. Let’s connect so we can explore all your options and make your move happen.