(Published on - 4/13/2023 2:44:05 PM)

Want To Sell Your House This Spring? Price It Right.

Over the last year, the housing market’s gone through significant change. While it’s still a sellers’ market, homes that are priced right are selling, and they get the most attention from buyers right now. If you’re thinking of selling your house this spring, it’s important to lean on your expert real estate advisor when it comes to setting a list price. As Realtor.com explains:

“Move-in-ready homes with curb appeal and in desirable areas—and that are priced to sell—are especially likely to move quickly this spring.”

In today’s market, how you price your house will not only make a big difference to your bottom line, but to how quickly your house will sell.

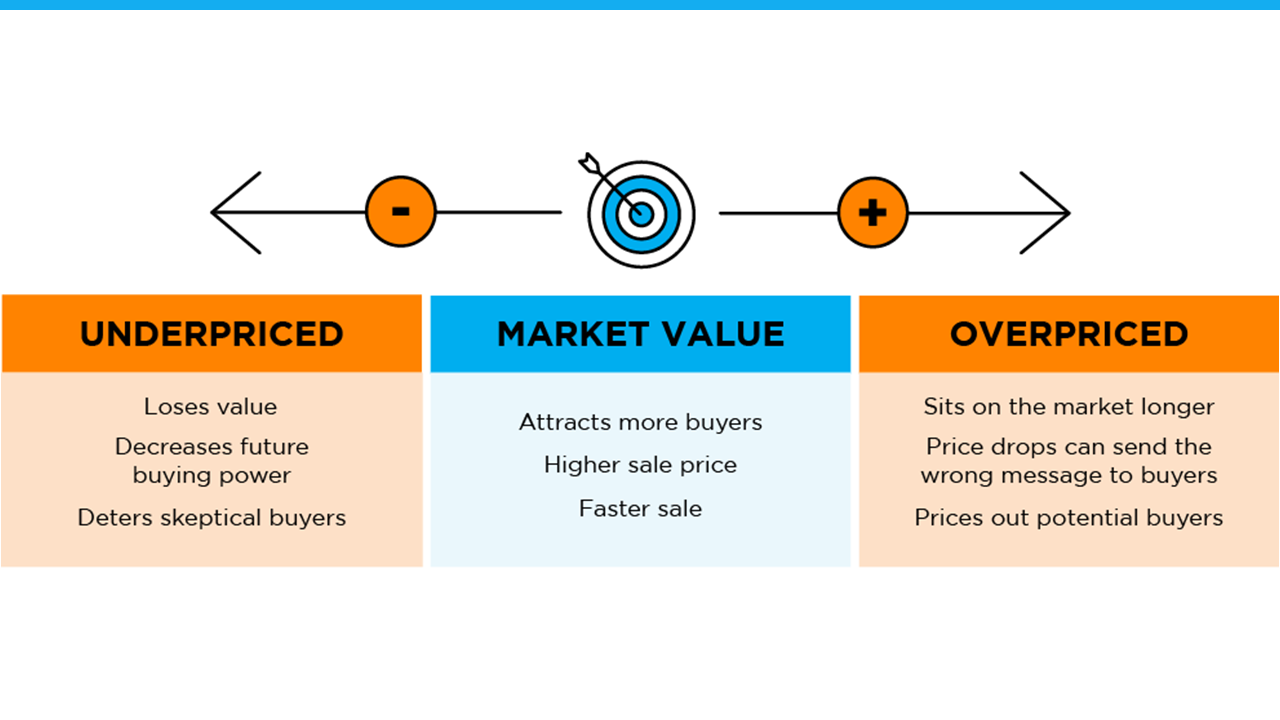

Why Pricing Your House Right Matters

Your asking price sends a message to potential buyers, especially today.

If it’s priced too low, you may leave money on the table or discourage buyers who may see a lower-than-expected price tag and wonder if that means something is wrong with the home.

If it’s priced too high, you run the risk of deterring buyers. When that happens, you may have to lower the price to drive interest when your house sits on the market for a while. But be aware that a price drop can be seen as a red flag by some buyers who will wonder what it means about the home.

To avoid either headache, price it right from the start. A real estate professional knows how to determine the ideal asking price. They balance the value of homes in your neighborhood, current market trends, buyer demand, the condition of your house, and more to find the right price. This helps lead to stronger offers and a greater likelihood your house will sell quickly.

The visual below helps summarize the impact your asking price can have:

Bottom Line

Homes priced at the current market value are selling faster and at a better price right now. To make sure you price your house appropriately, maximize your sales potential, and minimize your hassles, let’s connect today.