Brenda Lee Sherwood

Realty Executives Arizona Territory- White Mountains

If you’re one of the thousands of homebuyers waiting for rates to fall, you should know it’s already happening. And they recently crossed an important milestone. Rates officially dipped their toes into the 5s – something that hasn’t happened in about 3 years.

This moment marked a critical threshold. Now, rates are sitting in the low 6% territory. And expert forecasts project they’ll hover near this range throughout the year.

Here's why that’s so good for you.

A mortgage rate doesn’t just affect the interest you end up paying on your home loan. It shapes your entire buying experience.

When rates were up around 7% just one year ago, a lot of buyers felt priced out. Payments were higher. Budgets felt tighter. Affordability was a bigger challenge. That’s especially true for first-time homebuyers, who felt the biggest pinch.

But according to industry experts, that’s starting to change now that rates are slowly inching down. Let’s break down why.

Right now, borrowing costs are in their lowest range in almost 3 years. And that can change the type of home you can afford.

At 6% or below, you'll see:

In other words, you can now make a stronger offer, purchase in a different location, or buy a home that checks more of your boxes. And that feels like a big shift compared to when rates were at 7%.

To drive home just how much this helps potential homebuyers like you, consider this research from the National Association of Realtors (NAR). It shows that when mortgage rates sit around this level, millions more households can afford a home. When rates are at 6% or below:

That’s not just speculation. That’s pent-up demand finally getting the green light they’ve been waiting for. You’ve got the chance right now to get ahead and buy before more people notice the game has just changed.

Because whether rates stay in the low 6s or dip back down into the upper 5s, the math is already working in your favor. And the difference from a low 6% to a high 5% isn’t as big as you may think. But the difference from 7% to 6%? That is very much a big deal, and it’s a number that’s already working in your favor.

Mortgage rates don’t operate in a vacuum. Home prices, local inventory, property taxes, home insurance, and your personal finances still matter.

And a rate in this territory doesn’t mean every home suddenly works for every buyer. That’s why getting pre-approved and running your numbers with a trusted lender is key.

Still, this rate environment puts more buyers in play than we’ve seen in years. So, if buying didn’t work for you before, it’s worth taking another look.

Mortgage rates dropping to a 3-year low isn’t just a headline.

For many buyers, where rates are now could be the difference between watching from the sidelines and finally getting the keys to their next home.

If you’ve been waiting for a sign to re-run your numbers and see what’s possible now, this is it.

Let’s take a look at what today’s rates mean for your budget and your options.

What if you didn’t have a mortgage payment on your next house? It may sound a little unrealistic. But for a number of homeowners, it’s actually doable.

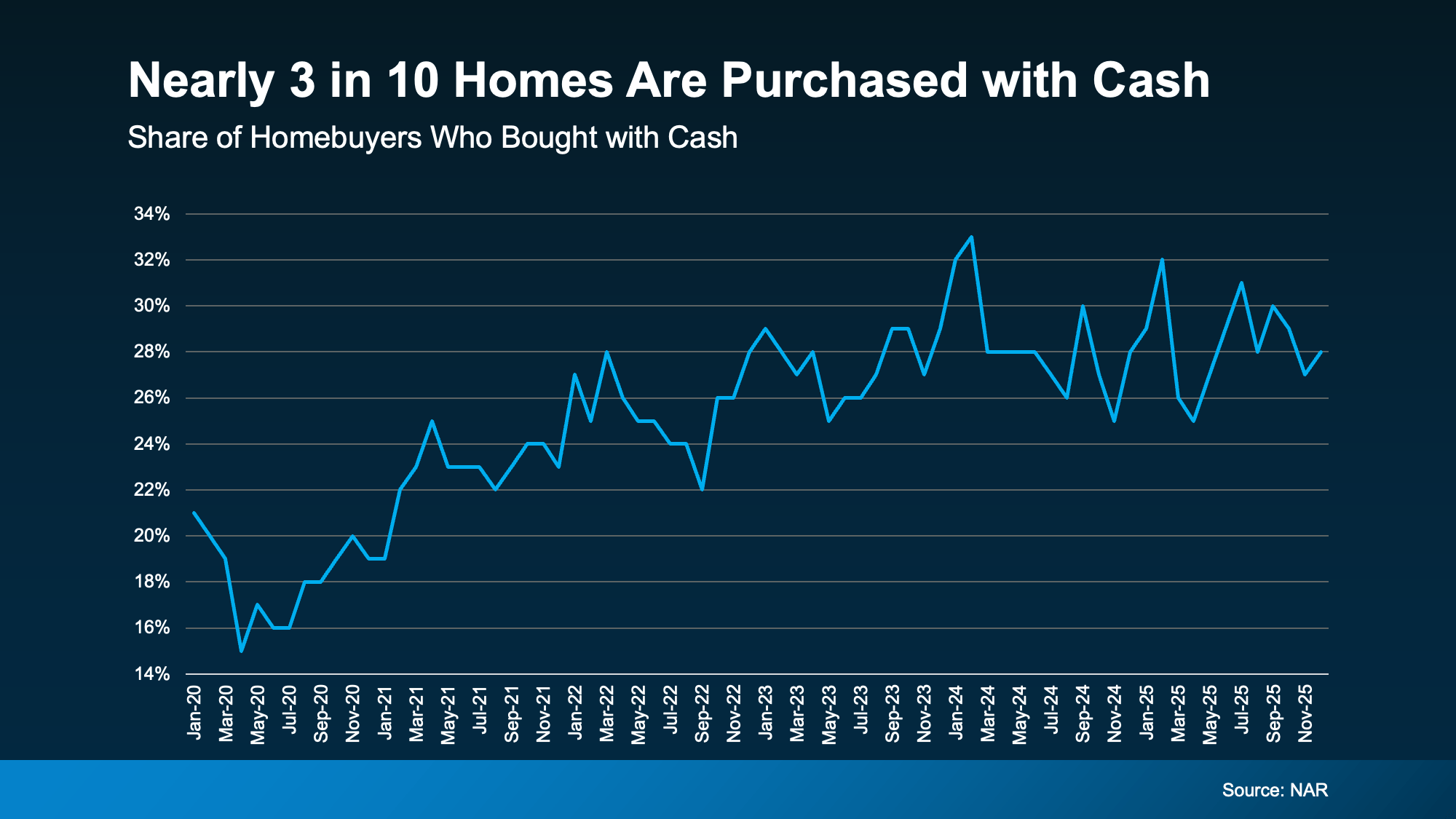

Nearly 3 in 10 homes purchased today are bought in cash, according to the National Association of Realtors (NAR). That’s far more than the pre-pandemic norm (see graph below):

So, how are so many buyers pulling that off? The answer is simple: home equity.

So, how are so many buyers pulling that off? The answer is simple: home equity.

Back in 2020-2021, mortgage rates and the number of homes for sale were both at all-time lows. And that combination pushed home prices up, fast.

If you owned a home during that time, it likely gained significant value – maybe even enough to buy your next house in cash. NAR explains:

“. . . rising home equity has armed many existing homeowners with the financial leverage to make cash offers, allowing them to convert years of price appreciation into immediate purchasing power.”

Here’s why you may want to go that route yourself, if you have enough equity to do it.

Sellers value certainty. And an all-cash offer removes one of the biggest unknowns in a transaction: financing. As Rocket Mortgage explains:

“Cash offers are attractive to sellers. Sellers often prefer to work with cash buyers if they can because they don’t have to worry about a buyer’s financing falling through at the last minute.”

In many markets, an all-cash offer can give you a serious edge.

And since you don't have to worry about underwriting, lender approvals, and loan processing, the time it takes to close shrinks. Cotality puts it this way:

“Cash buyers have always enjoyed an edge over borrowers. They remove financing risk, reduce delays, and often close in days rather than weeks.”

If the owner of the house you're buying is already under contract on their next home or they just need to move fast (like for a new job), that speed is a real draw.

When you buy in cash, you don’t have to finance your purchase. That means you don’t have to worry about what today’s mortgage rates are and you own the house outright from the day you close. And that’s a big deal.

No mortgage.

No monthly payment.

Full ownership.

That financial freedom opens the door for other big lifestyle benefits. Zillow explains:

“Paying in cash means you own your home outright. This eliminates the need for monthly mortgage payments, freeing up your finances for other priorities like savings, travel, or home improvements.”

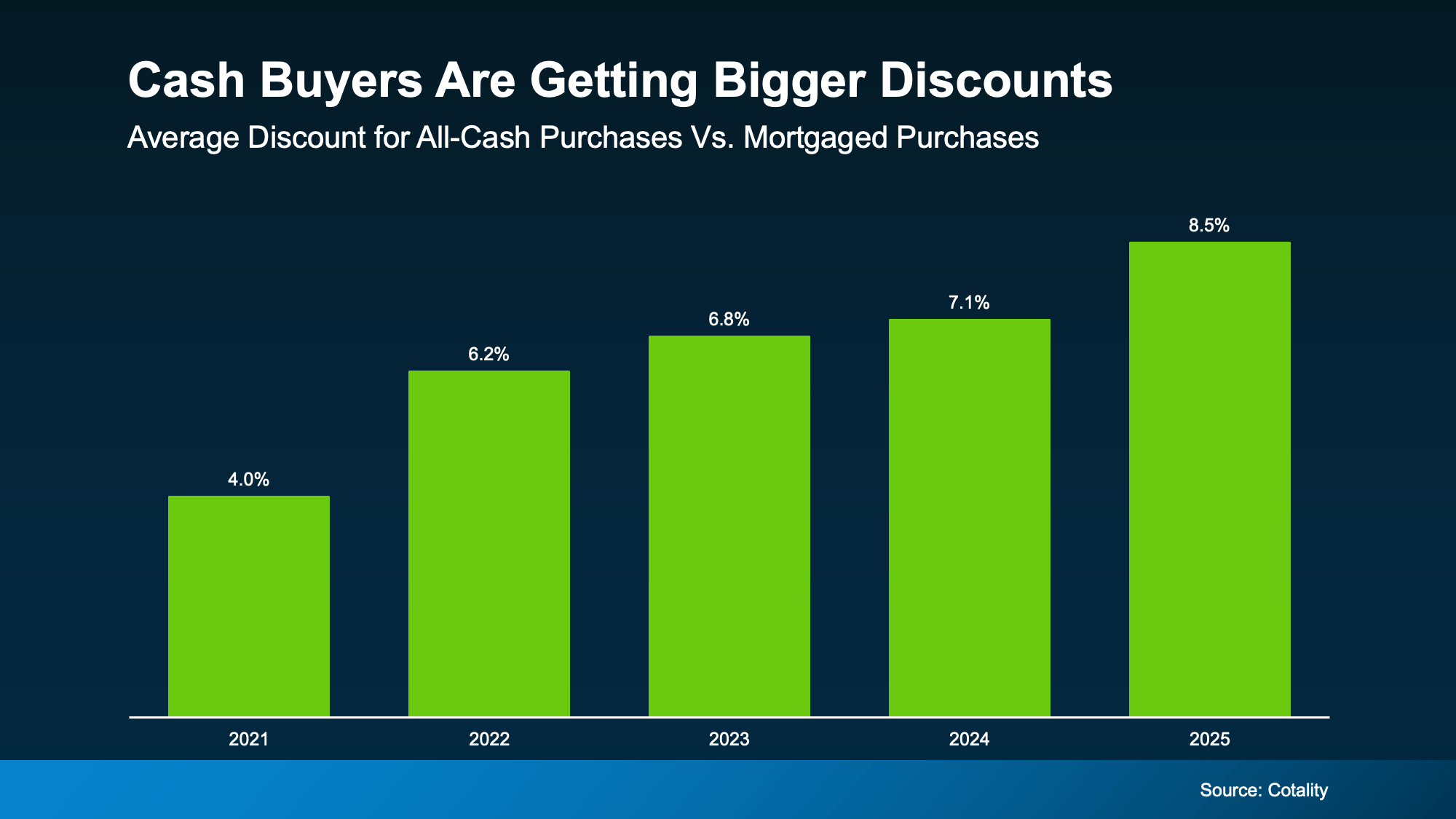

And here’s one more thing that surprises a lot of homeowners: cash buyers often pay less for the house.

According to Cotality, all-cash buyers tend to spend roughly 9% less on the house than buyers who use a mortgage. That’s because some sellers are willing to accept lower offers to get a deal done quickly, with more certainty of closing, and fewer financing hoops to jump through. As Cotality explains:

“From a seller’s point of view, a lower but reliable offer can feel preferable to a higher one that may collapse weeks later.”

And that advantage grows with each passing year (see graph below):

Is an All-Cash Move Realistic for You?

Is an All-Cash Move Realistic for You?Not every homeowner will buy their next house outright in cash. And that’s okay.

But the bigger takeaway is this: the equity you’ve built may give you more options than you think.

Whether that means downsizing and eliminating a mortgage entirely, or just relocating with stronger negotiating power, your current house may be what makes it possible.

Before assuming you’ll need another traditional mortgage, it’s worth asking one simple question: How much equity do you really have? Because the answer might change what you thought your next move could look like.

Curious what your home equity could do for you? Let’s run the numbers and see what kind of buying power you’re really sitting on.

Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment.

But then your rent goes up again. And again. And suddenly the thing that seemed flexible starts looking… expensive, especially considering you’re not building any equity. And once that happens, it’s easy to feel a little trapped in the cycle.

That’s because there’s so much chatter today about how buying a home isn’t affordable. But the truth is, the math may work out better than you'd expect based on what’s changed recently.

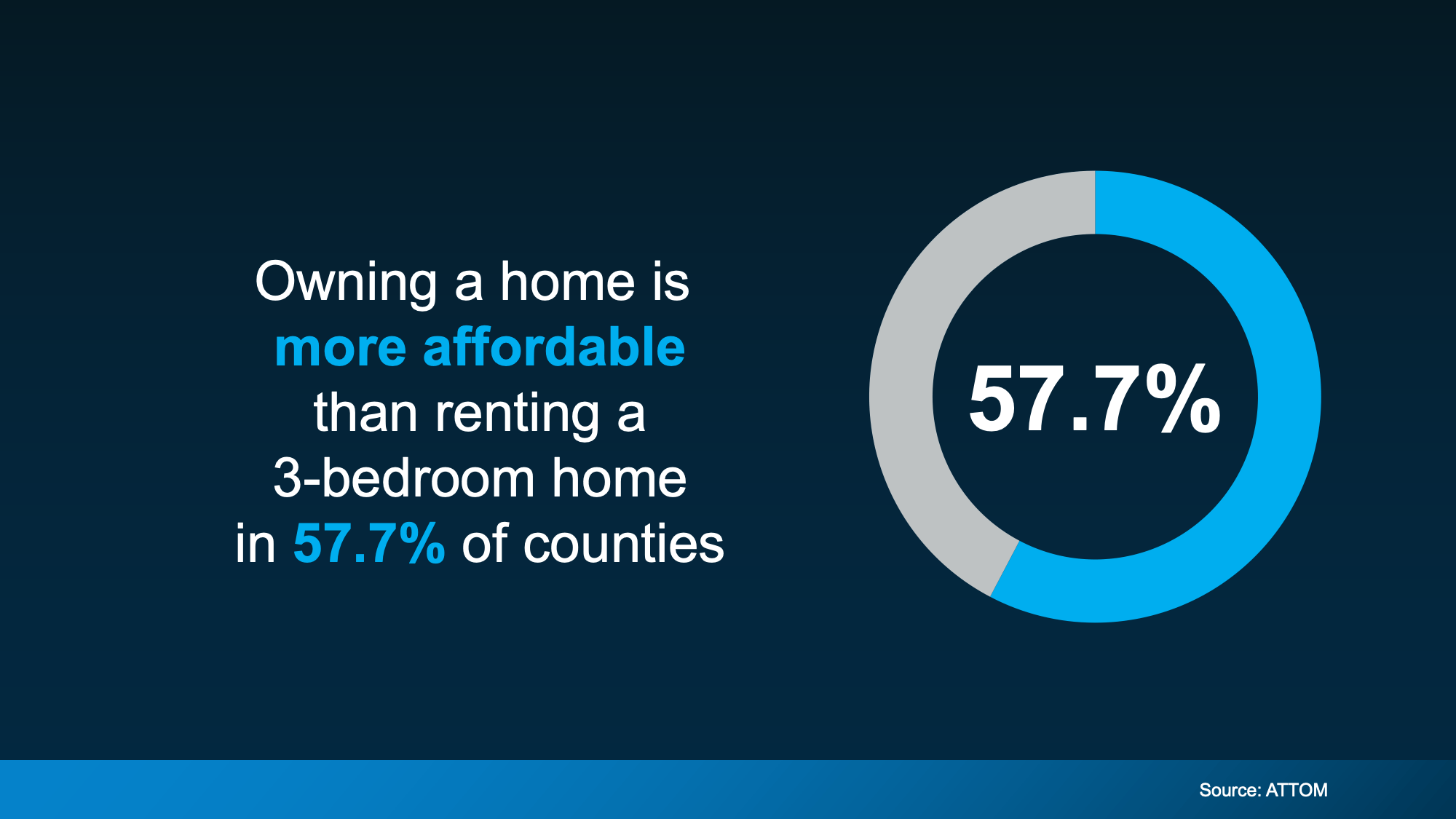

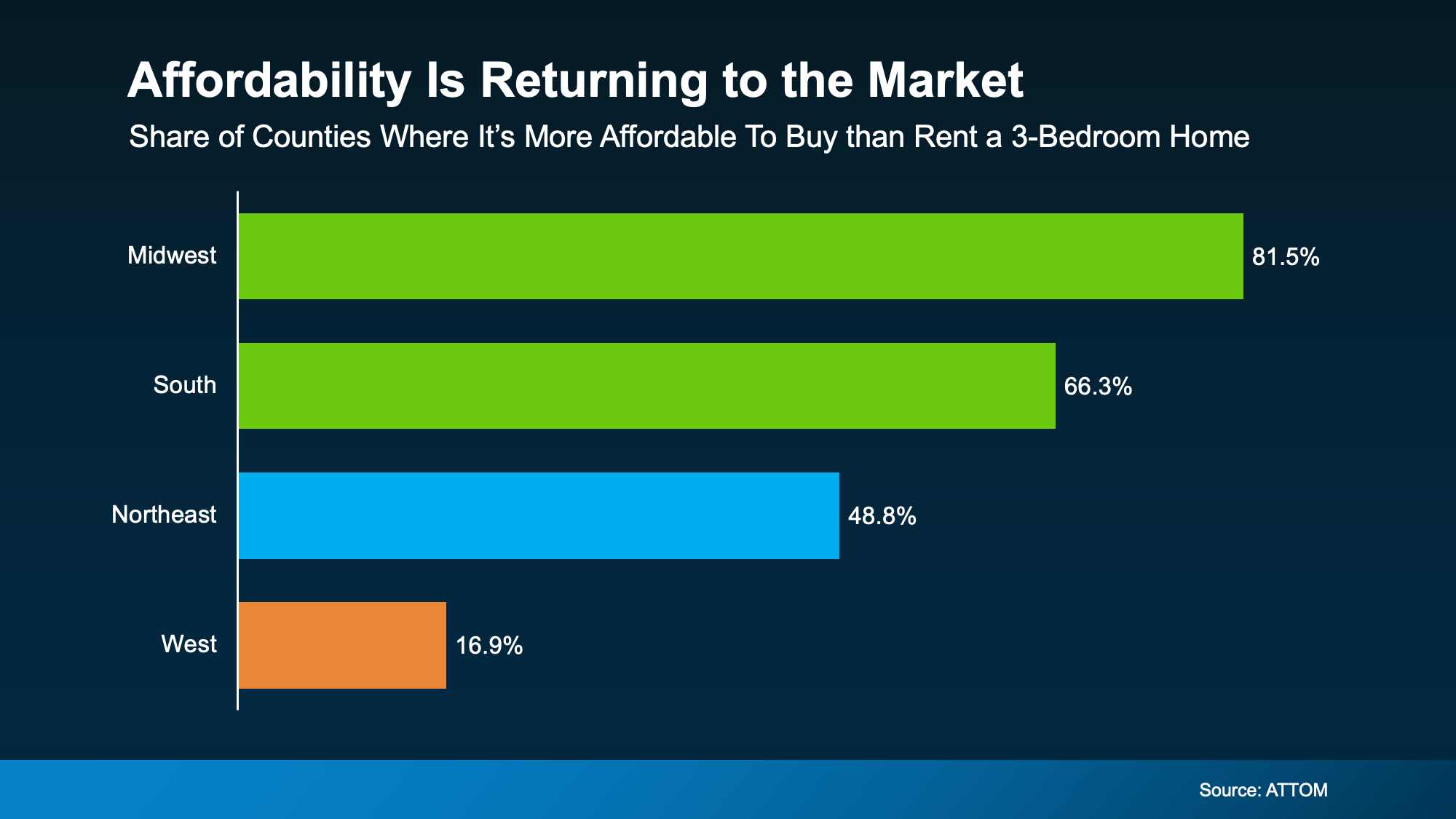

In a lot of places today, owning a home actually costs less each month than renting a 3-bedroom home. And recent data from ATTOM shows that’s true in nearly 58% of counties across the U.S. (see chart below).

And that's after you factor in things like insurance and typical maintenance costs.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

Now, even though nationally the balance has shifted, that doesn’t mean buying is more affordable in every market or for every renter.

While buying is more affordable than renting in nearly 58% of counties nationwide, that share looks different depending on your region (see graph below):

The biggest improvement is happening in the Midwest and South. But if you’re living in the West, things could still feel tight.

The takeaway? How affordable buying is really depends on where you live. And the only way to know how this plays out where you live is to look at the numbers locally.

Maybe you’re nodding along so far but thinking, “Okay, but I still can’t afford the upfront costs.” If that’s your reaction, you’re not the only one.

For many renters, the biggest hurdle isn’t the monthly payment alone. It’s the down payment, too.

But you’re not out of options. Here’s the part most people don’t hear enough about: there are thousands of down payment assistance programs available across the country, and many buyers qualify without realizing it.

And the average benefit? Roughly $18,000.

That kind of support can help cover part of your down payment or closing costs, which means you may not need to save nearly as much as you think to get started.

When you combine that with monthly payments that may work better than expected, especially as rates continue to ease and prices cool, buying may feel far more realistic than it looks at first glance.

The point isn’t that everyone should rush out and buy a home tomorrow.

It’s that renting isn’t always the more affordable option people assume it is – and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feeling stuck in the “someday” loop, it might be worth a simple conversation. Just a chance to see what’s possible and whether it makes sense for you.

Everyone talks about how spring is the best time to buy a home.

But there’s another window buyers often overlook that has some seriously great perks: winter.

Want to know 3 reasons buying just a few weeks earlier could save you thousands?

Drop a comment or DM me and I’ll send the details.

#BuyBeforeSpring #HomebuyingTips #KeepingCurrentMatters

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

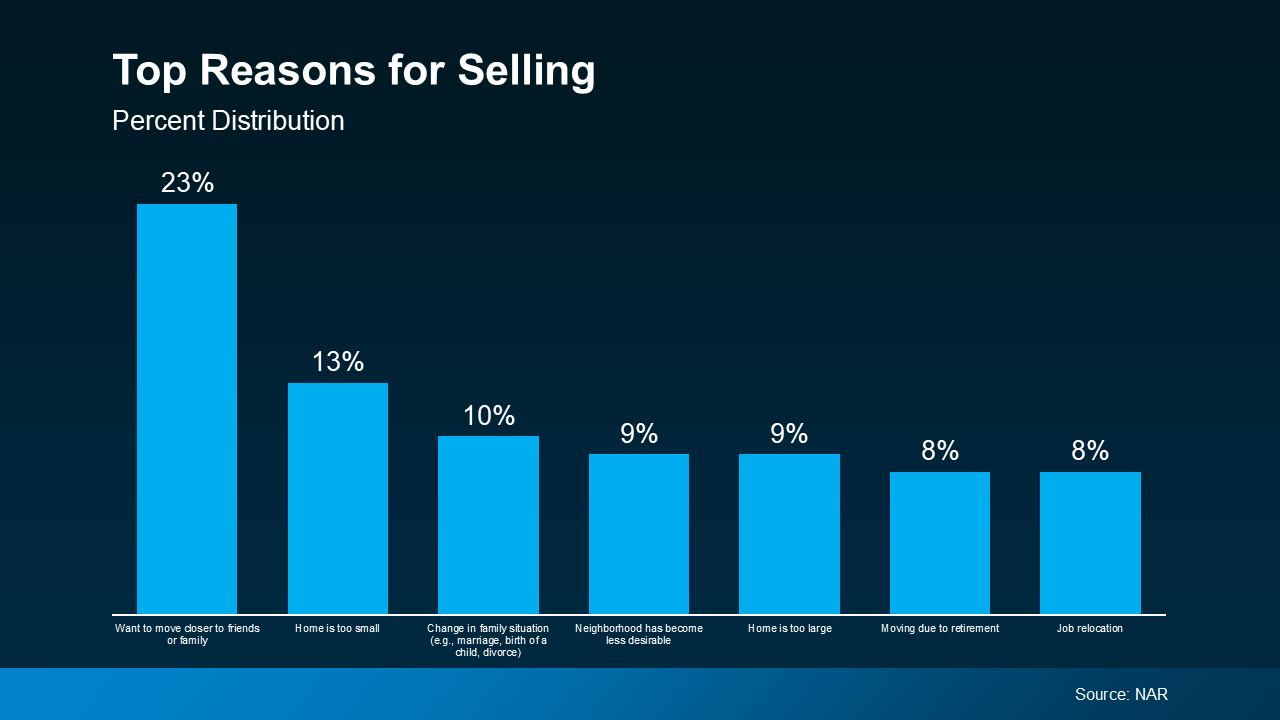

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today's homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s have a conversation.