Brian Bischoff

SFR, CSC, ACP

Realty Executives Midwest

5 DANGERS OF OVERPRICING

Setting the right list price is my specialty. There is more than comps involved. Contact me to learn more! Ready to sell? A sky-high list price may be appealing but there is some risk involved. Read on to learn the five dangers you face when you overprice your home.

You could encounter these issues: Fewer Showings Attract the Wrong Buyers Lose in Search Help Your Competitors Spend Too Long on the Market

1. FEWER SHOWINGS

A well-priced home is based on a lot more than comparable home prices in your area or even your neighborhood. Listing at the right price holds a lot of psychology. You need a certain equation of showings and foot traffic to create bidding wars and get the right price for your home. If you price your home too high to begin with, you’re going to miss out on a huge margin of potential buyers. A home will probably get few showings if it is more than 10% above market value. Price it right. Additionally, here are some tips that can help your home get more showings: Get listing feedback: your realtor can get this from other real estate agents and buyers. Use strategic and creative online marketing. Get professional pictures taken and a 360 video tour of your home. Stage your home to sell: take care of curb appeal and cosmetic adjustments to make your home more appealing to buyers. Appeal to emotion: as more buyers start their journey online, you need a compelling story and reasons they should come out and see the home.

2. ATTRACT THE WRONG BUYERS

Price brackets are all-important to home buyers. If bumping up your listing price puts you into another range, you’re going to get the wrong buyers. In this case, wrong buyers aren’t people who are unqualified. Instead, they’re people who are looking for a certain quality of home to match their price point. If your home is overpriced, it won’t have what they’re looking for and you’ll waste a lot of time wooing people who aren’t going to buy your home. Instead, use these tips to attract the right buyers: Update MLS listings with events and ask for an RSVP Tap niche or specialty markets Get referrals Add incentives to the home sale

3. LOSE IN SEARCH

The price bracket is also relevant for this issue. It’s dangerous to overprice your home because most buyers are finding you through online searches. If you don’t show up for the price bracket your ideal buyer is searching in, you’ll lose out. This loss of visibility could leave your home sitting on the market and eliminate any activity it could have had. There are ways to win in search. Of course, the first is pricing your home right. This way, you’ll be within the range of buyers who are looking for a home like yours. You can also: Use quality keywords and buzzwords Add a thorough, colorful description to your post Add an array of creative photos and videos Talk to your real estate agent about every platform on which your home can be featured, including websites and social media outlets

4. HELP YOUR COMPETITORS

Comparative Market Analysis (CMA) is the process real estate professionals use to analyze recently sold or for sale homes near yours. If that isn’t done, or you ignore it and price too high, you’re actually helping your competitors. Buyers have certain expectations with a price point for a home. If you’re trying to sell a beer home for a champagne price (and they don’t get champagne), they’re moving onto the next home. What’s more, buyers in a certain price range will be looking at comparable homes. If your home is priced the same but has inferior features, it will instantly look worse than the homes it’s being shown next to. In addition to helping your competitors, a home without a completed CMA could have issues during the home appraisal process.

5. SPEND TOO LONG ON THE MARKET

Overpriced homes don’t sell fast. The longer a home sits on the market, the less desirable it looks. If you have to start dropping the price, that looks even worse. Pricing your home correctly is the best way to ensure that you get early, quality traffic. Here are some more tips for selling your home fast: Make it show-worthy Neutralize your decor Time your listing Use professional media Be accommodating about scheduled showings and open houses Stand apart with unique events or showcases Get feedback 06 At the end of the day, pricing your home too high may actually get you less money. This is because the market will force you to lower your asking price, which looks bad to potential buyers. All of the hard-earned web traffic and showings could be undone if that number isn’t right. Don’t take chances with this important process! I know the comps but also the psychology and additional factors to support your home's suggested list price.

Contact me today!

Brian Bischoff,

Realty Executives Midwest,

Realtor Phone: 630-866-6591

brianbischoff@realtyexecutives.com

www.vetsellinghomes.com

Realty Executives Midwest, Realtor

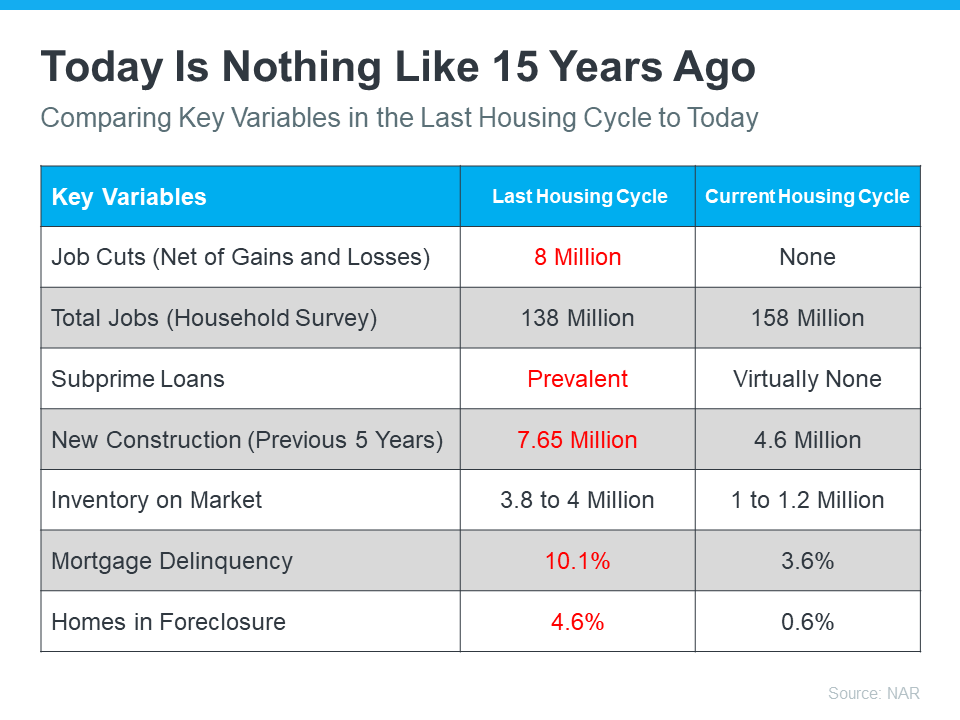

There’s no doubt today’s housing market is very different than the frenzied one from the past couple of years. In the second half of 2022, there was a dramatic shift in real estate, and it caused many people to make comparisons to the 2008 housing crisis. While there may be a few similarities, when looking at key variables now compared to the last housing cycle, there are significant differences.

In the latest Real Estate Forecast Summit, Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), drew the comparisons below between today’s housing market and the previous cycle:

Looking at the facts, it’s clear: today is very different than the housing market of 15 years ago.

And in today’s market, with inventory rising and less competition from other buyers, there’s opportunity right now. According to David Stevens, former Assistant Secretary of Housing:

“So be advised…this may be the one and only window for the next few years to get into a buyer’s market. And remember…as the Federal Reserve data shows…home prices only go up and always recover from recessions no matter how mild or severe. Long term homeowners should view this market…right now…as a unique buying opportunity.”

Today’s housing market is nothing like the real estate market 15 years ago. If you’re a buyer right now, this may be the chance you’ve been waiting for.

![Key Terms To Know When Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/11164544/Key-Terms-To-Know-When-Buying-A-Home-MEM-1046x2684.png)

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

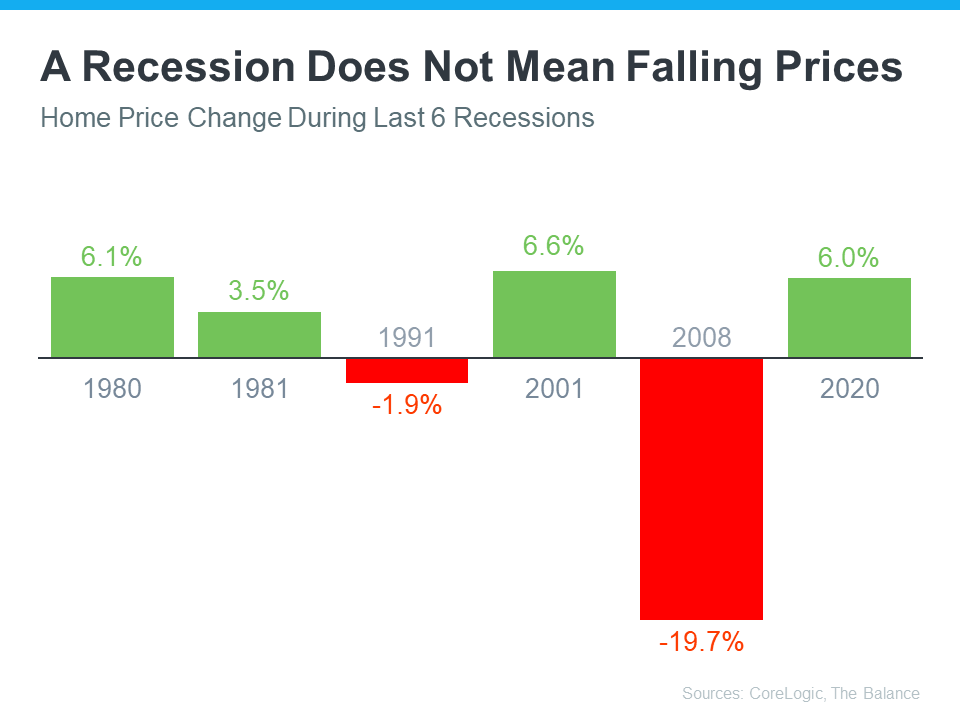

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

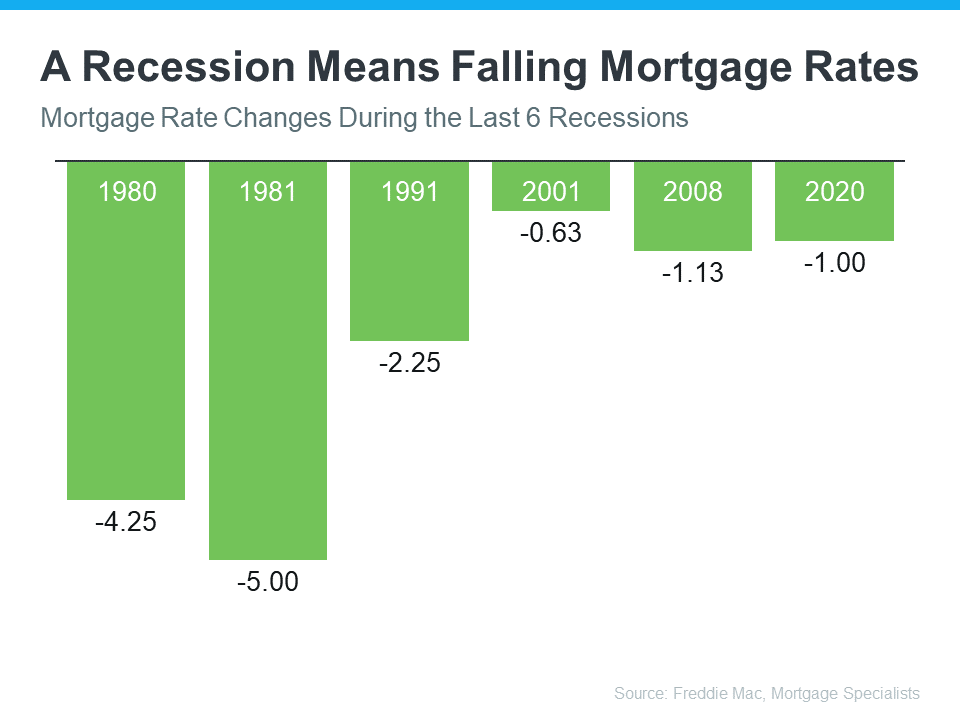

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Last year, the Federal Reserve took action to try to bring down inflation. In response to those efforts, mortgage rates jumped up rapidly from the record lows we saw in 2021, peaking at just over 7% last October. Hopeful buyers experienced a hit to their purchasing power as a result, and some decided to press pause on their plans.

Today, the rate of inflation is starting to drop. And as a result, mortgage rates have dipped below last year’s peak. Sam Khater, Chief Economist at Freddie Mac, shares:

“While mortgage market activity has significantly shrunk over the last year, inflationary pressures are easing and should lead to lower mortgage rates in 2023.”

That’s potentially great news if you’re a buyer aiming to jump back into the housing market. Any drop in mortgage rates helps boost your purchasing power by bringing down your expected monthly mortgage payment. This means the lower mortgage rates experts forecast this year could be just what you need to reignite your homebuying goals.

While this opens up a window of opportunity for you, remember: you shouldn’t expect rates to drop back down to record lows like we saw in 2021. Experts agree that’s not the range buyers should bank on. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“I think we could be surprised at how much mortgage rates pull back this year. But we’re not going back to 3 percent anytime soon, because inflation is not going back to 2 percent anytime soon.”

It’s important to have a realistic vision for what you can expect this year, and that’s where the advice of expert real estate advisors is critical. You may be surprised by the impact even a mild drop in mortgage rates has on your budget. If you’re ready to buy a home now, today’s market presents the opportunity to get a more affordable mortgage rate, find your dream home, and face less competition from other buyers.

The recent pullback in mortgage rates is great news – but if you’re ready to buy now, holding out for 3% is a mistake. Work with a local lender to learn how today’s rates impact your goals, and let’s connect to explore your options in our area.